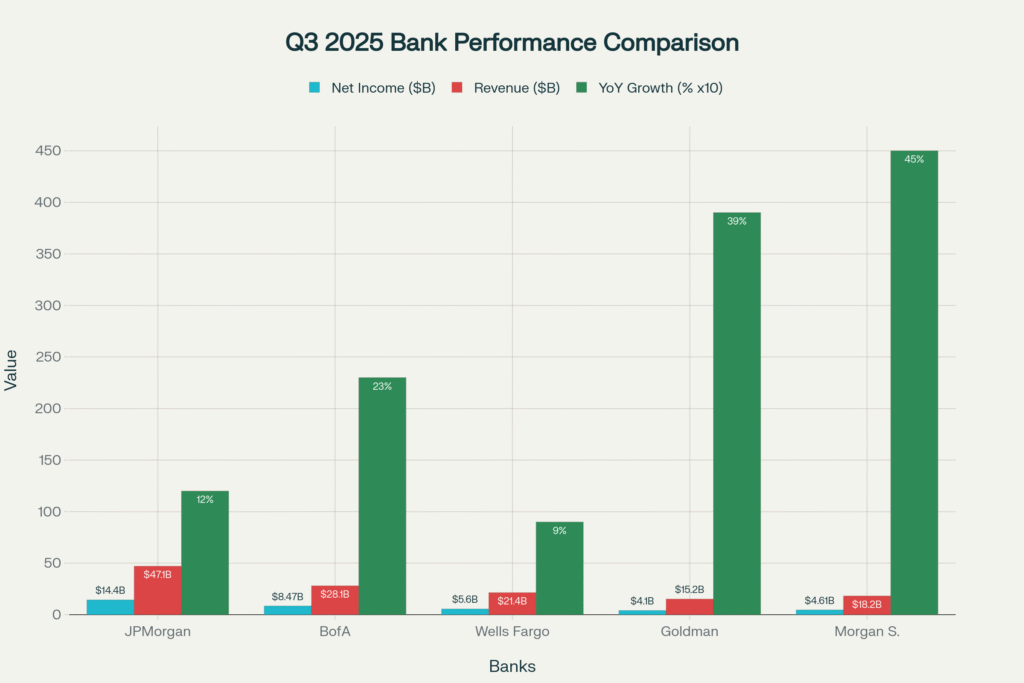

The third quarter of 2025 has delivered a banner earnings season for America’s largest banks, with JPMorgan Chase’s stellar results setting the tone for an industry that has demonstrated remarkable resilience amid a complex macroeconomic environment. JPMorgan’s earnings per share of $5.07 beat expectations by 4.75%, while net income surged 12% year-over-year to $14.4 billion. This performance, alongside equally impressive results from Goldman Sachs (39% profit surge), Morgan Stanley (45% earnings growth), and Bank of America (23% profit increase), reveals critical insights about the underlying strength of the U.S. economy and the evolving financial landscape.

The banking sector’s exceptional performance stems from a perfect storm of favorable conditions: record-breaking trading revenues exceeding $35 billion across major institutions, a resurgent investment banking environment with M&A volumes up 40% year-over-year, and continued consumer financial health despite emerging signs of economic softening. These results provide the most comprehensive real-time view of economic conditions, offering crucial signals for policymakers, investors, and market participants navigating an increasingly uncertain global environment.

Record Trading Revenues: Market Volatility Creates Windfall

Unprecedented Trading Performance Across All Banks

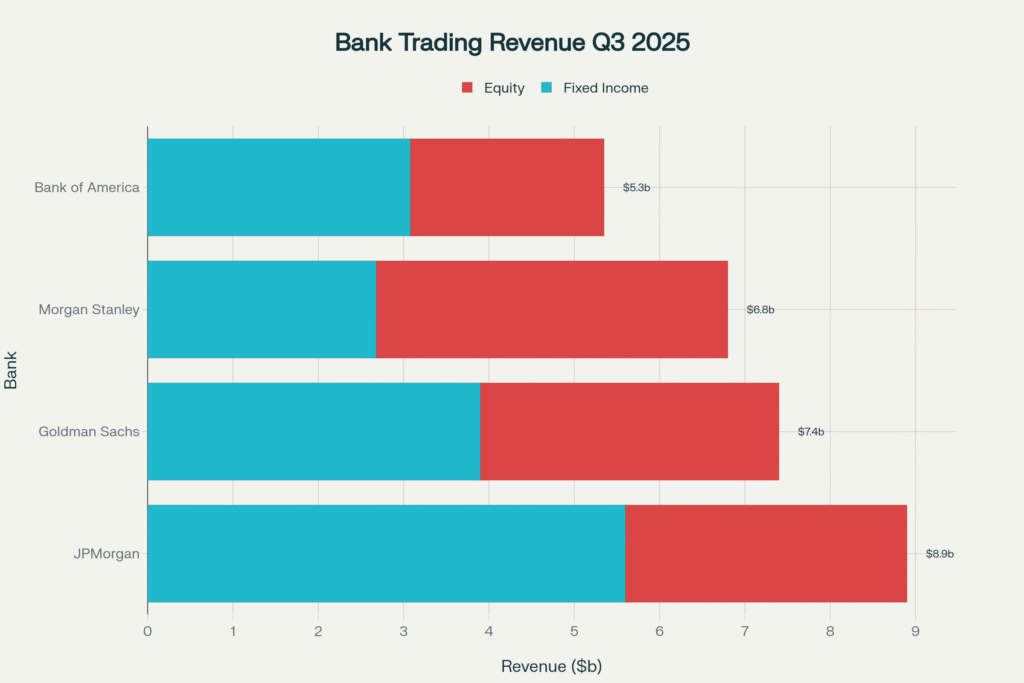

The standout feature of Q3 2025 earnings was the exceptional performance of trading divisions, which generated combined revenues exceeding $35 billion across the major Wall Street banks. JPMorgan led this surge with record quarterly trading revenue of $8.9 billion, representing a significant increase from previous quarters and substantially exceeding analyst expectations. This performance was broad-based, with fixed income trading jumping 21% to $5.6 billion and equity trading surging 33% to $3.3 billion, both metrics rising well above Street forecasts.

Goldman Sachs demonstrated even more dramatic trading strength, with the investment banking giant reporting trading revenues that contributed significantly to its 39% profit surge. The firm’s trading operations capitalized on increased market volatility throughout the quarter, particularly benefiting from client portfolio adjustments as equity markets reached unprecedented levels. Morgan Stanley’s equity trading revenues reached $4.12 billion, nearly 21% higher than expected, while the firm achieved record performance in prime brokerage services catering to hedge funds.

Bank of America’s trading division generated $5.35 billion in revenue, exceeding estimates of $5.01 billion, with particularly strong performance in equity trading at $2.27 billion versus $2.08 billion expected. This broad-based strength across all major trading franchises indicates that the revenue surge was driven by fundamental market conditions rather than institution-specific factors, suggesting sustained client activity and market-making opportunities.

Market Dynamics Driving Trading Success

The exceptional trading performance reflects several converging market dynamics that created optimal conditions for Wall Street’s trading desks. President Trump’s tariff policies and ongoing geopolitical tensions generated significant market volatility, prompting institutional investors to actively reposition portfolios and hedge exposures. This increased client activity translated directly into higher trading volumes and improved bid-ask spreads, particularly benefiting banks with strong market-making capabilities.

The Federal Reserve’s monetary policy stance created additional trading opportunities, as clients navigated changing interest rate expectations and sector rotation strategies. With the Fed funds rate currently at 4.25% and expectations for further cuts to 3.75% by year-end, fixed income markets experienced significant volatility that skilled traders were able to monetize effectively. The uncertainty surrounding future policy direction created ongoing opportunities for relative value trades and client hedging activity.

Record levels in equity markets, combined with increased M&A activity, generated substantial equity trading volumes as institutional investors adjusted positions around corporate actions and market events. The S&P 500’s continued strength to near-record levels provided a supportive backdrop for equity derivatives and options trading, while sector rotation themes around AI, energy transition, and trade policy created additional volatility that trading desks successfully captured.

Investment Banking Renaissance: Deal Activity Surges

M&A Market Experiences Dramatic Revival

The investment banking sector experienced a remarkable renaissance in Q3 2025, with global M&A volumes reaching $1.26 trillion, up 40% year-over-year and representing the second-best third quarter on record by value. This surge translated directly into exceptional fee performance across major banks, with JPMorgan’s investment banking fees climbing 16% to $2.6 billion and Bank of America reporting a dramatic 43% increase to $2.0 billion.

Goldman Sachs demonstrated the most impressive investment banking performance, with fees surging 42% as the firm capitalized on its leading market position in advisory services and underwriting. The firm’s strength was particularly evident in advisory services, reflecting a significant increase in completed mergers and acquisitions volumes and successful execution of complex transactions. Morgan Stanley’s investment banking revenues increased to $2.11 billion, with advisory fees reaching $684 million as the firm benefited from the corporate activity rebound.

The revival in deal activity stems from several factors converging to create a favorable environment for corporate transactions. Regulatory changes under the Trump administration have created a more permissive M&A landscape, while companies are hunting for scale with a record number of mega-deals (over $10 billion) announced this year. Elevated equity valuations and accessible debt markets have provided corporations with multiple avenues to finance strategic transactions, while CEO confidence in the economic outlook has encouraged long-delayed strategic initiatives.

IPO Market Shows Signs of Life

The initial public offering market, which had been largely dormant for much of 2024, began showing meaningful signs of recovery in Q3 2025. Goldman Sachs reported higher net revenues in equity underwriting, primarily driven by initial public offerings, indicating renewed investor appetite for new issues. This revival reflects improving market conditions and investor confidence, particularly in high-growth sectors where valuations have stabilized after previous volatility.

The IPO recovery is being driven by several factors, including more stable market conditions, clearer regulatory frameworks, and pent-up demand from both issuers and investors. Companies that delayed going public during periods of market uncertainty are now finding windows of opportunity, while institutional investors are seeking new growth opportunities as traditional investments face valuation challenges. Private equity sponsors are also finding more favorable exit environments, contributing to the pipeline of potential public offerings.

However, the IPO market recovery remains selective and concentrated in specific sectors where investor demand is strongest. Technology companies with clear AI applications, healthcare innovators, and companies benefiting from infrastructure investment themes are finding the most receptive audiences. The success of recent IPOs is likely to encourage additional companies to test public markets, potentially creating a positive feedback loop that could sustain investment banking fee growth into 2026.

Consumer Financial Health: Resilience with Emerging Stress

Credit Quality Indicators Signal Continued Strength

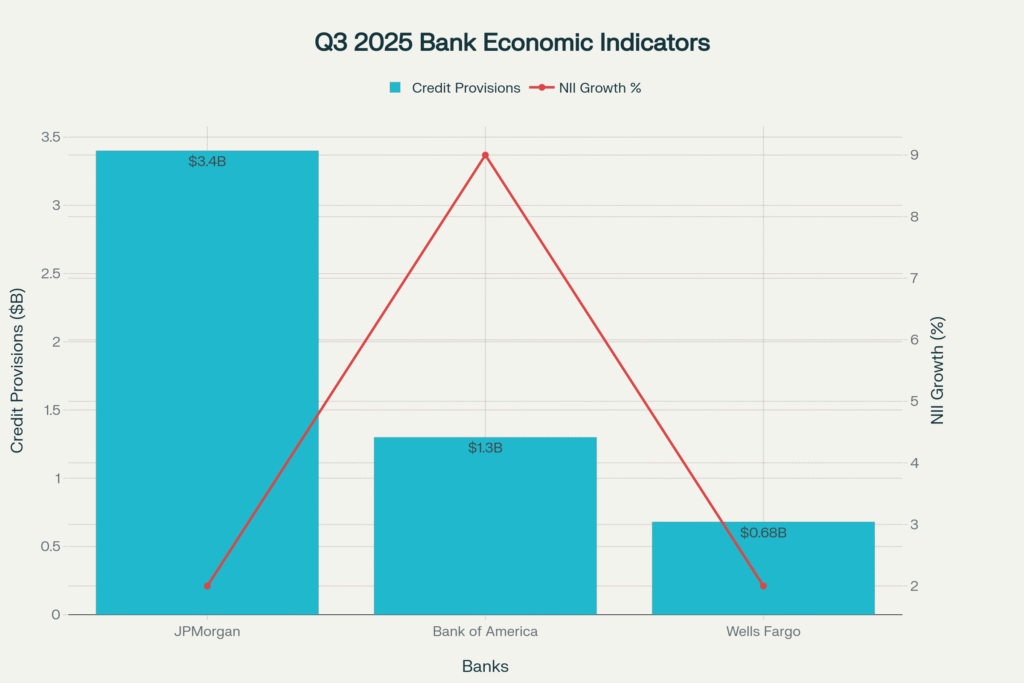

Despite concerns about economic softening, credit quality metrics across major banks remained remarkably strong in Q3 2025, providing crucial insights into consumer and commercial borrower financial health. Wells Fargo reported provisions for credit losses of just $681 million, significantly below the anticipated $1.17 billion, indicating that credit concerns that worried analysts earlier in the year have not materialized. Bank of America’s provision for credit losses decreased by approximately 13% to $1.3 billion, demonstrating improving risk profiles across its loan portfolio.

JPMorgan’s credit costs of $3.4 billion included $2.6 billion in net charge-offs and an $810 million net reserve build, reflecting a more cautious approach to credit reserves while actual losses remained manageable. The bank’s Card Services net charge-off rate of 3.15% remained within normal historical ranges, suggesting that consumer credit stress, while present, has not reached concerning levels. The firm’s provision approach reflects proactive risk management rather than reactive responses to deteriorating conditions.

Net charge-off rates across the major banks remained within historical norms, with most institutions reporting stable or improving trends in consumer credit metrics. Commercial credit quality showed particular strength, with most banks reporting minimal charge-offs in commercial and industrial lending portfolios. This performance reflects the continued resilience of business cash flows and the effectiveness of enhanced underwriting standards implemented following previous credit cycles.

Early Warning Signs of Economic Softening

While overall credit metrics remain strong, bank executives are identifying early warning signs of economic softening that warrant monitoring. JPMorgan CEO Jamie Dimon noted “some signs of softening, particularly in job growth” while emphasizing that “the U.S. economy generally remained resilient”. This nuanced assessment reflects banks’ unique vantage point on economic conditions through their customer payment patterns and borrowing behaviors.

Consumer spending patterns observed through bank transaction data show continued resilience but with emerging areas of concern. Higher-end consumers continue to drive spending growth, benefiting from elevated asset values and continued employment strength in professional services sectors. However, lower-income segments are showing increased sensitivity to inflation and borrowing costs, with some banks noting longer payment times and increased use of credit facilities among certain demographic groups.

Commercial borrowers are displaying increased caution in capital expenditure decisions, with loan demand remaining moderate despite generally favorable lending conditions. This hesitation reflects uncertainty about trade policies, regulatory changes, and the broader economic trajectory rather than immediate financial stress. Banks are interpreting this cautious approach as prudent business management rather than evidence of deteriorating business conditions.

Net Interest Income: Navigating the Rate Environment

Deposit and Lending Dynamics Show Resilience

Net interest income performance across major banks exceeded expectations, providing crucial insights into the effectiveness of interest rate policy transmission and banking sector health. Bank of America reported record net interest income of $15.2 billion, marking a 9% year-over-year increase and demonstrating the bank’s ability to manage asset-liability dynamics effectively in a changing rate environment. The bank raised its full-year NII forecast, now projecting Q4 NII between $15.6-15.7 billion, indicating confidence in sustained performance.

JPMorgan’s net interest income increased by 2% to $24.1 billion, reflecting the bank’s successful balance sheet optimization amid competitive deposit pressures and evolving loan demand patterns. The bank raised its 2025 NII forecast to approximately $95.5 billion from earlier estimates, while providing 2026 guidance of $95 billion excluding market impacts. This forward guidance suggests that banks are successfully adapting to the post-rate-hike environment and positioning for continued profitability.

Wells Fargo’s net interest income surpassed expectations, contributing to the bank’s ability to set higher targets for net interest margins going forward. The bank’s performance reflects improved asset yields and successful deposit repricing strategies that have enabled margin expansion despite competitive pressures. Average loan growth of 1% quarter-over-quarter across major banks indicates steady but not excessive credit demand, suggesting balanced economic conditions.

Federal Reserve Policy Implications

The banking sector’s NII performance provides important signals about Federal Reserve monetary policy effectiveness and future policy directions. The current federal funds rate of 4.25%, with market expectations for a decline to 3.75% by year-end, appears to be creating favorable conditions for bank profitability while supporting credit intermediation. Banks’ ability to maintain NII growth despite rate cut expectations suggests that the current policy stance is achieving desired economic effects without undermining financial sector stability.

Deposit competition has moderated from earlier peaks, indicating that funding pressures that concerned regulators earlier in the rate cycle have largely stabilized. Most major banks report stable deposit costs and improved deposit mix trends, with customers gravitating toward relationship-based banking rather than simply chasing the highest yields. This trend supports banking sector profitability while indicating consumer confidence in the financial system.

The banking sector’s guidance for 2026 NII performance suggests expectations for continued policy normalization without dramatic disruptions to business models. Banks’ confidence in providing forward guidance indicates their assessment that current economic conditions will prove sustainable and that potential policy changes will be implemented gradually rather than abruptly. This stability supports continued credit provision to the economy.

Capital Markets Revival and Economic Growth Signals

Corporate Confidence Drives Transaction Activity

The surge in investment banking activity reflects a fundamental shift in corporate confidence and strategic decision-making that has important implications for broader economic growth. Global deal activity exceeded $3 trillion in the first three quarters of 2025, representing the highest volume since the pandemic peak in 2021. This revival indicates that corporate leaders are increasingly confident about economic stability and growth prospects, leading to the pursuit of strategic transactions that had been delayed during periods of uncertainty.

The types of transactions driving this activity provide insights into corporate strategic priorities. Companies are pursuing scale-building acquisitions and vertical integration strategies that suggest confidence in long-term demand trends and competitive positioning. Technology sector consolidation, infrastructure investments, and supply chain reshoring transactions are prominent themes that align with broader economic policy objectives and secular growth drivers.

Private equity participation in the transaction surge indicates healthy exit markets and continued institutional capital deployment. The success of recent exits is encouraging sponsors to pursue additional portfolio company transactions, creating a positive feedback loop that supports continued deal activity. This institutional capital deployment has important multiplier effects on economic growth through corporate expansion, employment, and capital investment.

Market Structure Evolution and Innovation

The strong performance of capital markets divisions reflects ongoing evolution in market structure and financial innovation that supports economic growth. Banks’ trading performance benefits from increased electronic trading capabilities and improved risk management systems that enable more efficient capital allocation and price discovery. These technological improvements reduce transaction costs and improve market liquidity, supporting broader economic efficiency.

The growth in structured products and derivatives trading indicates increasing sophistication in risk management across the economy. Corporate and institutional clients are utilizing more complex hedging strategies that enable them to pursue longer-term strategic objectives while managing short-term volatility. This risk management infrastructure supports business investment and economic growth by reducing uncertainty and enabling better capital allocation decisions.

International capital flows and cross-border transaction activity remain robust despite geopolitical tensions, indicating continued integration of global financial markets. U.S. banks’ strong international trading and investment banking results suggest that American financial markets continue to serve as global capital allocation centers, supporting domestic economic growth through capital attraction and efficient resource deployment.

Economic Outlook and Policy Implications

Banking Sector Signals for Monetary Policy

The banking sector’s Q3 2025 performance provides important signals for Federal Reserve policy makers as they navigate the balance between supporting economic growth and maintaining price stability. The combination of strong credit quality, robust NII performance, and healthy loan demand growth suggests that current monetary policy is achieving desired effects without creating financial stability risks. Banks’ ability to maintain profitability while supporting credit intermediation indicates that the transmission mechanism of monetary policy remains effective.

The moderate pace of loan growth across major banks suggests that credit demand is healthy but not excessive, indicating balanced economic conditions rather than either credit restriction or excessive risk-taking. This measured growth pace supports Federal Reserve objectives of maintaining financial stability while ensuring adequate credit availability for productive economic activities. Banks’ forward guidance confidence indicates their assessment that policy changes will be gradual and predictable.

Consumer and commercial credit quality metrics provide important real-time indicators of economic stress that complement traditional macroeconomic statistics. The continued strength in these metrics, despite some softening indicators identified by bank executives, suggests that the economy retains fundamental resilience. This assessment supports continued gradual policy normalization rather than dramatic policy shifts in either direction.

Geopolitical Risk Assessment Through Banking Lens

Bank executives’ commentary on geopolitical risks provides insights into how these factors are affecting real economic activity. JPMorgan’s Jamie Dimon emphasized “complex geopolitical conditions, tariffs and trade uncertainty” as key risk factors, reflecting the banking sector’s front-line perspective on how policy uncertainty affects business decision-making. However, the strong financial performance suggests that these risks are being managed effectively by both banks and their clients.

International trading revenues and cross-border transaction activity provide direct measures of how geopolitical tensions are affecting global economic integration. The continued strength in these areas suggests that while concerns exist, the fundamental infrastructure of global commerce and finance remains resilient. Banks’ risk management capabilities are enabling continued participation in international markets despite elevated uncertainty.

The banking sector’s capital strength and liquidity positions provide important buffers against potential economic disruptions from geopolitical developments. All major banks report strong capital ratios and substantial liquidity reserves, indicating preparedness for various economic scenarios. This financial sector resilience supports overall economic stability and provides policymakers with flexibility in responding to future challenges.

Investment Implications and Strategic Outlook

Banking Sector Investment Thesis

The Q3 2025 earnings results support a compelling investment thesis for the banking sector based on multiple converging factors. The combination of strong trading revenues, recovering investment banking fees, and resilient credit quality creates favorable conditions for sustained profitability growth. Banks’ ability to exceed earnings expectations while maintaining strong capital positions demonstrates operational excellence and strategic positioning that should support continued investor interest.

Valuation metrics remain attractive relative to both historical levels and broader market multiples, particularly given the demonstrated earnings power and balance sheet strength. The sector’s ability to generate substantial returns on equity while maintaining conservative risk profiles offers attractive risk-adjusted return potential for investors. Dividend yields and capital return programs provide additional value creation mechanisms that complement earnings growth.

The regulatory environment appears stable with potential for continued normalization of capital requirements and stress testing regimes. This regulatory stability supports business model predictability and strategic planning capabilities that enable banks to optimize capital allocation and operational efficiency. The policy environment under the current administration appears favorable for banking sector growth and profitability.

Sector Differentiation and Strategic Positioning

The Q3 2025 results highlight important strategic differentiation among major banks that creates distinct investment opportunities. JPMorgan’s comprehensive business model and market leadership positions enable it to benefit from virtually all positive market developments while maintaining defensive characteristics during challenging periods. The bank’s “fortress balance sheet” and diversified revenue streams provide stability and growth potential across economic cycles.

Goldman Sachs and Morgan Stanley’s strong performance in trading and investment banking reflects their strategic focus on capital markets activities and wealth management. These business models provide leveraged exposure to market recovery and increased client activity, making them attractive for investors seeking growth-oriented banking exposure. Their premium valuation reflects these superior growth characteristics.

Bank of America and Wells Fargo represent different strategic approaches to traditional commercial banking, with both institutions demonstrating strong operational execution and market positioning. Their performance reflects the continued attractiveness of core banking activities when executed with strong risk management and operational efficiency. These institutions offer more defensive investment characteristics while still participating in sector growth trends.

Future Performance Drivers and Risks

The sustainability of Q3 2025’s exceptional performance will depend on several key factors that investors should monitor closely. Continued market volatility that supports trading revenues is inherently unpredictable, suggesting that future quarters may not match Q3’s exceptional trading performance. However, the structural improvements in market-making capabilities and risk management should provide sustained competitive advantages even in more normalized market conditions.

The investment banking recovery appears sustainable given improving corporate confidence and regulatory environment, but the pace of growth may moderate from Q3’s exceptional levels. The pipeline of potential transactions remains robust, supporting continued fee growth although quarter-to-quarter variability should be expected. Private equity exit activity and IPO market development will be key drivers of sustained investment banking performance.

Credit quality trends bear careful monitoring as economic conditions evolve and the effects of previous monetary tightening work through the system. While current metrics remain strong, banks’ own guidance suggests increasing attention to early warning indicators of potential stress. Proactive risk management and conservative underwriting standards should provide protection against adverse credit developments, but investors should remain vigilant for changing trends.

Conclusion: Banking Strength Signals Economic Resilience

The third quarter of 2025 has delivered exceptional banking sector results that provide crucial insights into the underlying strength and resilience of the U.S. economy. JPMorgan’s leadership in delivering record trading revenues and strong earnings growth, alongside impressive performances from Goldman Sachs, Morgan Stanley, Bank of America, and Wells Fargo, demonstrates the financial sector’s ability to capitalize on favorable market conditions while maintaining prudent risk management.

The convergence of record trading revenues, resurgent investment banking activity, and continued consumer financial health paints a picture of an economy that remains fundamentally sound despite facing various challenges and uncertainties. Banks’ unique position as intermediaries in virtually all economic activity provides them with unparalleled visibility into real-time economic conditions, making their collective assessment particularly valuable for understanding broader economic trends.

The forward guidance and strategic confidence expressed by bank management teams suggests that the financial sector expects continued stability and growth opportunities, albeit with appropriate caution regarding geopolitical and policy uncertainties. This measured optimism, combined with strong balance sheet positions and diversified revenue streams, positions the banking sector to continue supporting economic growth while generating attractive returns for investors.

For policymakers, the banking sector’s performance validates current monetary policy approaches while providing important real-time feedback on the effectiveness of policy transmission mechanisms. For investors, the sector offers attractive opportunities to participate in economic growth while benefiting from improved operational efficiency and strategic positioning that should support sustained outperformance relative to broader market indices.

As the economy navigates an increasingly complex global environment, the banking sector’s demonstrated resilience and adaptability provide important stability and confidence for continued economic expansion. The third quarter of 2025 will likely be remembered as a period when American banks demonstrated their essential role in supporting economic growth while delivering exceptional value to all stakeholders.

Ready to capitalize on the banking sector’s transformation? Our M&A advisory services help institutional investors and strategic acquirers identify prime opportunities in the evolving financial services landscape. From fintech consolidation to traditional banking M&A, we provide comprehensive market intelligence and transaction execution expertise. Contact us today to explore how the current environment creates compelling investment opportunities across the banking and financial services ecosystem.

Leave a Reply