The European financial services landscape is experiencing its most significant regulatory-driven transformation in over a decade, fundamentally reshaping global asset management mergers and acquisitions in ways that extend far beyond continental borders. The convergence of landmark regulatory changes—including the permanent codification of the Danish Compromise under CRR3, the implementation of AIFMD 2.0, and the ambitious Single Investment Union initiative—has unleashed a €500 billion consolidation wave that is redefining competitive dynamics across international markets.

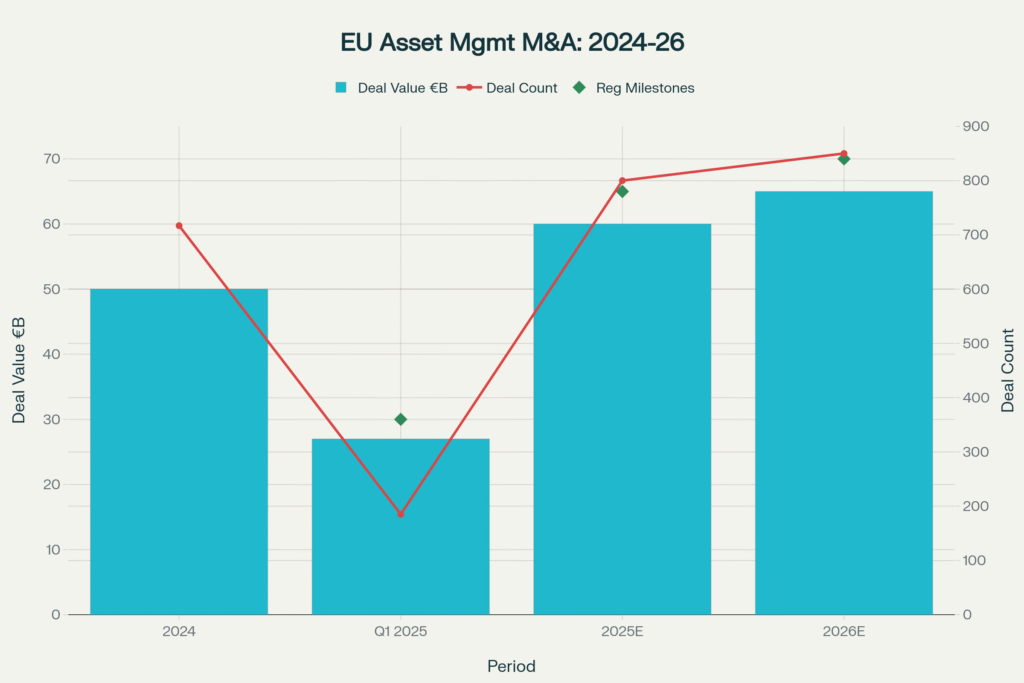

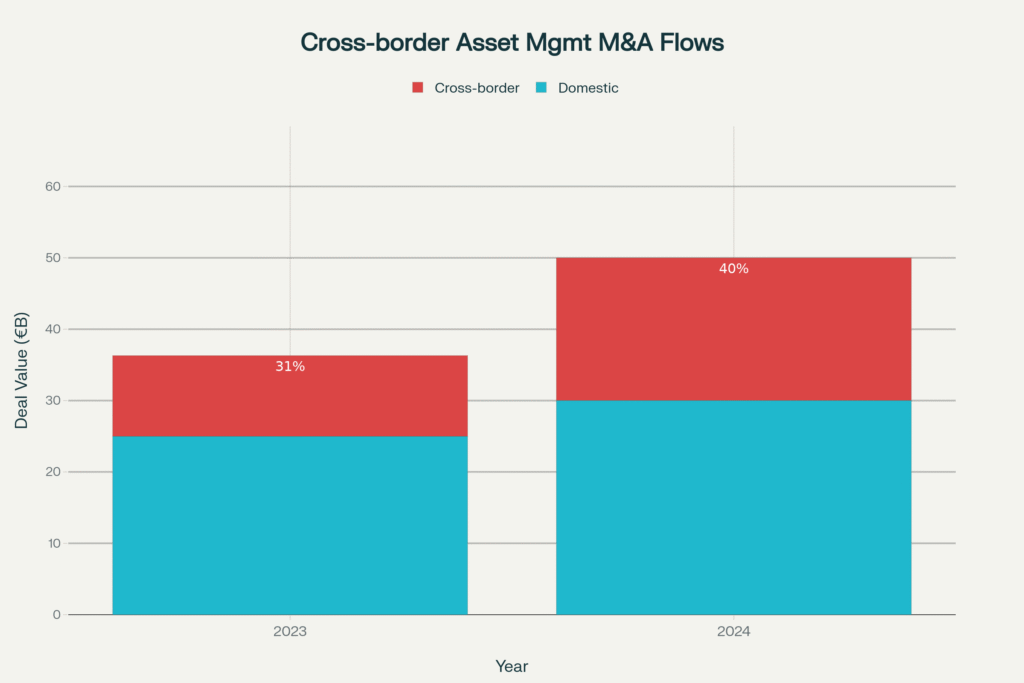

This regulatory renaissance reflects Europe’s strategic response to fragmented capital markets, intensifying global competition, and the imperative to create scale-driven efficiencies that can compete with American and Asian financial giants. European financial services M&A surged to €50 billion in 2024 with 717 transactions, nearly doubling from €36.3 billion in 2023, while cross-border deals increased by 34% as regulatory barriers diminish. The implications cascade globally as international asset managers reassess their European strategies, regulatory arbitrage opportunities emerge, and competitive pressure mounts on non-European institutions to respond with their own consolidation initiatives.

The Danish Compromise Revolution: Capital Efficiency Drives Bancassurance M&A

Permanent Regulatory Framework Creates Strategic Certainty

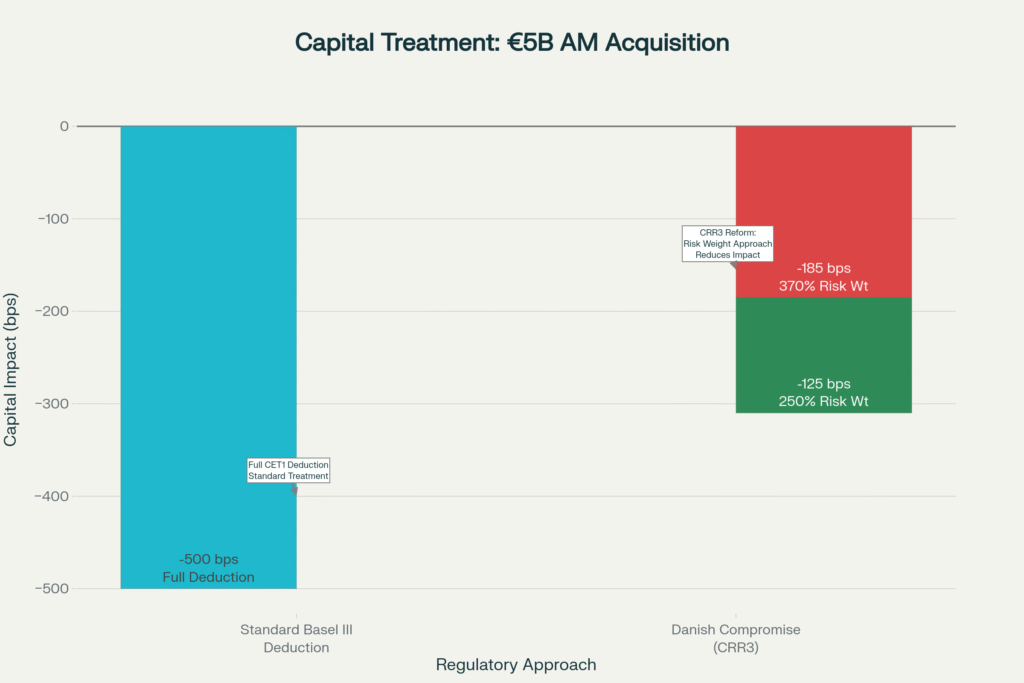

The transformation of the Danish Compromise from a supposedly temporary measure into a permanent fixture of European banking regulation represents one of the most significant developments in cross-sector M&A facilitation. Under the revised Capital Requirements Regulation 3 (CRR3), effective January 2025, financial conglomerates can now risk-weight their insurance and asset management holdings at 250%, down from the previous 370%, rather than applying full capital deductions that previously made such acquisitions prohibitively expensive.

This regulatory evolution has profound implications for bancassurance strategies and asset management consolidation. For a typical €5 billion asset management acquisition, the Danish Compromise reduces the capital impact from 500 basis points under standard Basel III treatment to just 125 basis points under the new CRR3 framework. This dramatic improvement in capital efficiency has already catalyzed major transactions, with BNP Paribas completing its €5.1 billion acquisition of AXA Investment Managers to create a €1.5 trillion asset management platform, despite regulatory complications that limited the full benefits of the Danish Compromise.

The “Danish Compromise Squared” (DC2) provision adds another layer of strategic advantage by allowing goodwill from asset management acquisitions made through insurance subsidiaries to be risk-weighted rather than deducted from capital. This treatment proves particularly valuable for asset management acquisitions, where client relationships and intangible assets typically command significant premiums. EY estimates that this enhanced treatment could improve acquisition economics by 50-75 basis points compared to direct bank acquisitions, creating clear incentives for structuring deals through insurance platforms.

ECB Interpretation Limits but Doesn’t Eliminate Benefits

The European Central Bank’s increasingly restrictive interpretation of Danish Compromise eligibility has introduced complexity but not eliminated the fundamental regulatory advantage driving bancassurance M&A. ECB Banking Supervision clarified in May 2025 that the Danish Compromise applies specifically to insurance undertakings rather than standalone asset management firms, effectively blocking BNP Paribas from achieving the full capital benefits initially anticipated for its AXA Investment Managers acquisition.

This regulatory pushback reflects ECB concerns about potential gaming of capital requirements and the need to maintain level playing fields across different acquisition structures. ECB Chief Supervisor Claudia Buch emphasized that “our understanding of the Danish Compromise is that it covers the insurance sector, not asset management firms”. This interpretation forced BNP Paribas to absorb a 35 basis point CET1 impact instead of the initially projected 25 basis points, demonstrating how regulatory uncertainty can affect deal economics even under supposedly favorable frameworks.

Despite these limitations, the underlying incentive structure remains compelling for appropriately structured transactions. Banks can still achieve significant capital efficiencies by acquiring asset managers through existing insurance subsidiaries or by structuring deals to include meaningful insurance operations. The regulatory framework continues to favor integrated financial services groups over pure-play banking institutions, encouraging the bancassurance model that European regulators have long supported as a source of financial stability and customer value.

Single Investment Union: Dismantling Cross-Border Barriers

Legislative Framework Eliminates Market Fragmentation

The European Commission’s Single Investment Union strategy represents the most ambitious attempt to create a truly integrated European asset management market since the original Capital Markets Union initiative. Scheduled legislative proposals in Q4 2025 will address fundamental barriers to cross-border trading, post-trading infrastructure, investment fund distribution, and asset manager operations. These measures target the structural fragmentation that has limited European asset managers’ ability to achieve scale comparable to their American counterparts.

The SIU framework encompasses three critical dimensions of market integration: removal of legal and regulatory barriers, harmonization of supervisory practices, and creation of common market infrastructure. Studies commissioned by the European Commission have identified over 200 specific barriers to cross-border asset management operations, ranging from divergent licensing requirements to incompatible IT systems and discriminatory tax treatments. The SIU proposals aim to eliminate these barriers through targeted legislative action rather than comprehensive regulatory overhaul.

Cross-border M&A activity has already responded to anticipated regulatory changes, with transnational deals increasing 34% in volume and 20% in value during 2024. This surge reflects deal makers’ confidence that regulatory barriers will continue diminishing, making cross-border combinations more operationally and economically attractive. The 91 cross-border transactions announced in 2024 represent the highest level in five years, indicating that European asset managers are positioning themselves for a more integrated market environment.

ESMA Supervision and Regulatory Convergence

The gradual transfer of supervisory responsibilities from national competent authorities to the European Securities and Markets Authority represents a fundamental shift toward regulatory centralization that facilitates cross-border consolidation. Proposed measures would grant ESMA direct supervisory authority over large cross-border asset managers, reducing the compliance complexity that currently discourages European integration. While implementation remains subject to member state negotiations, the direction toward centralized supervision is clear and irreversible.

Current supervisory fragmentation imposes significant costs on cross-border operations, with asset managers required to navigate different licensing procedures, reporting requirements, and interpretation of ostensibly harmonized EU regulations. The Investment Company Institute estimates that regulatory fragmentation adds 15-25% to operational costs for managers operating across multiple EU jurisdictions. ESMA centralization would eliminate much of this complexity while creating economies of scale that favor larger, integrated European asset managers over smaller national players.

The proposed supervisory framework includes structured coordination mechanisms and peer review processes designed to ensure consistent application of EU regulations across member states. These measures acknowledge that complete centralization may not be politically feasible while still achieving meaningful harmonization. Enhanced NCA cooperation facilitated by ESMA could deliver 60-70% of the benefits of full centralization while preserving national supervisory traditions and expertise.

AIFMD 2.0: Liquidity Management Requirements Drive Consolidation

Mandatory Liquidity Management Tools Increase Compliance Burden

The Alternative Investment Fund Managers Directive 2.0, effective April 2026, introduces comprehensive liquidity management requirements that significantly increase operational complexity and compliance costs for European asset managers. All open-ended alternative investment funds must implement at least two liquidity management tools from a prescribed list including redemption gates, swing pricing, and side pockets. These requirements reflect lessons learned from liquidity stress during market turbulence and aim to protect investors while maintaining financial stability.

The compliance burden falls disproportionately on smaller asset managers who lack the operational infrastructure and technological capabilities to implement sophisticated liquidity management systems. Industry estimates suggest that AIFMD 2.0 compliance will require €5-15 million in initial system investments plus ongoing operational costs of €1-3 million annually. These fixed costs create significant economies of scale that favor larger managers and encourage consolidation among smaller players seeking to share compliance infrastructure.

ESMA Guidelines published in April 2025 provide detailed implementation guidance but also reveal the complexity of the new requirements. Fund managers must develop comprehensive policies and procedures for tool selection, calibration, activation, and deactivation while ensuring appropriate investor disclosure and regulatory reporting. The 12-month implementation window for existing funds creates additional pressure for managers to complete any contemplated mergers before compliance costs become fully apparent.

Loan Origination and Leverage Restrictions Reshape Fund Structures

AIFMD 2.0’s restrictions on loan origination by alternative investment funds represent a fundamental shift in European private credit markets that is driving strategic repositioning and consolidation. Open-ended funds face a 175% leverage limit while closed-ended funds are capped at 300%, with additional requirements for credit policies, risk retention, and concentration limits. These constraints particularly affect the rapidly growing private credit sector, where many funds will need to restructure or seek exemptions.

The “originate to distribute” prohibition prevents funds from originating loans solely for transfer to third parties, fundamentally altering business models that have driven growth in European private credit markets. Many fund managers will need to develop permanent loan portfolios or partner with institutions capable of long-term credit holding. This regulatory shift favors established financial institutions with balance sheet capacity over pure-play fund managers, creating additional incentives for bank acquisitions of asset management firms.

Liquidity management requirements for loan-originating funds mandate closed-end structures unless managers can demonstrate compatibility with redemption policies. This requirement effectively eliminates certain hybrid fund structures and forces managers to choose between liquidity provision and loan origination capabilities. The resulting business model clarity is expected to accelerate consolidation as managers focus on core competencies rather than attempting to serve multiple market segments with incompatible regulatory requirements.

Global Competitive Implications and Strategic Responses

American and Asian Asset Managers Reassess European Strategies

The regulatory transformation of European asset management markets is forcing global competitors to fundamentally reassess their continental strategies as competitive dynamics shift dramatically. American asset managers face the prospect of competing against newly consolidated European giants with €1+ trillion in assets under management and integrated distribution capabilities across 27 countries. The BNP Paribas-AXA Investment Managers combination exemplifies this trend, creating a platform comparable in scale to major American competitors while benefiting from regulatory advantages unavailable to foreign entrants.

Asian asset managers, particularly those from Japan and Singapore, are accelerating their European expansion plans to establish positions before consolidation eliminates attractive acquisition targets. Chinese asset managers face additional regulatory scrutiny under foreign investment screening regimes, but are exploring partnership structures and minority stake acquisitions to access European distribution capabilities. The window for non-European entry is narrowing as regulatory preferences increasingly favor European integration over global diversification.

Technology-driven asset managers and fintech platforms face particularly complex strategic choices as traditional regulatory categories become more important than technological innovation. AIFMD 2.0’s liquidity management requirements effectively eliminate many digital-first fund structures that cannot accommodate mandatory redemption gates and swing pricing mechanisms. European regulators’ preference for operational substance over technological efficiency creates barriers for asset managers built around algorithmic trading and automated portfolio management.

Regulatory Arbitrage Opportunities and Limitations

The evolving European regulatory landscape creates both opportunities and constraints for regulatory arbitrage strategies that have historically driven cross-border asset management structures. The Danish Compromise’s permanent establishment under CRR3 creates clear advantages for European financial conglomerates over international competitors who cannot access similar capital treatment for insurance and asset management combinations. This regulatory asymmetry is likely to accelerate the repatriation of European asset management activities from international financial centers.

Brexit has eliminated the UK’s role as a regulatory arbitrage center for European asset management, forcing international managers to establish substantial European operations or accept limitations on their EU market access. The UK’s proposed mutual recognition arrangements with Switzerland represent an attempt to create an alternative regulatory framework but cannot replicate the integrated European market access that drove London’s historical dominance. Luxembourg and Ireland continue to benefit from favorable tax and regulatory treatments but face increasing pressure from the European Commission to eliminate competitive distortions.

ESMA’s enhanced supervisory role creates both opportunities and risks for regulatory arbitrage strategies. Centralized supervision could eliminate the “forum shopping” among national regulators that has historically enabled regulatory arbitrage, but might also create more consistent and predictable regulatory outcomes. International asset managers are increasingly focused on regulatory compliance costs rather than arbitrage opportunities, reflecting the maturation of European regulatory frameworks and the increasing penalties for non-compliance.

Transaction Execution and Strategic Considerations

Deal Structure Innovation Responds to Regulatory Constraints

The complexity of European regulatory frameworks is driving sophisticated deal structure innovation as acquirers seek to optimize regulatory treatment while achieving strategic objectives. The BNP Paribas-AXA Investment Managers transaction demonstrates both the potential and limitations of regulatory optimization, with the bank initially structuring the deal through its insurance subsidiary to access Danish Compromise benefits but ultimately facing ECB restrictions that increased capital costs.

Insurance subsidiary structures are becoming increasingly common for asset management acquisitions, even when direct bank acquisitions might offer superior operational integration. The 125-basis-point capital advantage from risk-weighting versus deduction creates compelling economics for appropriately structured transactions. However, regulatory uncertainty about ECB interpretation requires careful legal structuring and regulatory pre-clearance to avoid the execution risks experienced by BNP Paribas.

Cross-border transaction structures must navigate increasingly complex regulatory approval processes as member states assert greater scrutiny over strategic asset acquisitions. The EU Foreign Subsidies Regulation adds additional complexity for transactions involving non-EU acquirers or targets with foreign government connections. Transaction timing has become increasingly important as regulatory windows of opportunity may close rapidly due to changing political priorities or supervisory interpretations.

Valuation Implications of Regulatory Change

The regulatory transformation of European asset management is fundamentally altering valuation methodologies and creating new sources of both value creation and destruction. Asset managers with strong European distribution capabilities and regulatory compliance infrastructure command premium valuations as acquirers recognize the increasing barriers to market entry and expansion. Scale advantages in regulatory compliance are becoming more important than traditional metrics like assets under management or fee rates.

The Danish Compromise creates clear valuation differences between insurance-affiliated and standalone asset managers, with affiliated firms benefiting from lower acquisition capital costs for potential acquirers. Industry analysis suggests that regulatory optimization can add 10-15% to asset management valuations for appropriately structured transactions, creating incentives for financial engineering that may not align with operational efficiency. Valuation premiums for European asset managers have increased 25-30% since 2024 as regulatory advantages become more apparent and scarce.

AIFMD 2.0 compliance costs are creating valuation pressure for smaller managers who cannot achieve economies of scale in regulatory infrastructure. Firms with less than €5 billion in assets under management face disproportionate compliance burdens that may render them financially unviable as independent entities. Distressed asset management acquisitions are expected to increase significantly in 2026-2027 as compliance costs fully materialize and smaller managers seek exits rather than expensive system upgrades.

Future Implications and Strategic Outlook

Emerging Competitive Landscape and Market Structure

The convergence of European regulatory changes is creating a fundamentally different competitive landscape that will define asset management industry structure for the next decade. The emergence of €1+ trillion European asset management platforms represents a qualitative shift toward scale-based competition that mirrors developments in American markets while maintaining distinctly European characteristics around bancassurance integration and cross-border distribution.

Traditional boundaries between banking, insurance, and asset management are dissolving as regulatory incentives favor integrated financial services groups. The Danish Compromise’s permanent establishment encourages banks to view asset management as a natural extension of their insurance operations rather than a separate business line, creating opportunities for operational synergies and capital efficiency that standalone managers cannot replicate. This structural shift disadvantages pure-play asset managers regardless of their operational efficiency or investment performance.

Technology adoption in European asset management will be shaped increasingly by regulatory requirements rather than market demand or operational efficiency. AIFMD 2.0’s liquidity management tools mandate specific technological capabilities that favor established financial technology providers over innovative startups. The compliance-driven technology adoption cycle is likely to favor large systems integrators over specialized fintech solutions, potentially slowing innovation in favor of regulatory predictability.

Regulatory Evolution and Policy Implications

The success of European regulatory integration in driving asset management consolidation is likely to influence policy development in other major financial centers as competitive pressures mount. The European model of using regulatory incentives to encourage domestic consolidation while maintaining international market access offers lessons for other jurisdictions seeking to strengthen their financial services sectors. American regulators face increasing pressure to respond to European integration with their own initiatives to support domestic asset management competitiveness.

The permanent establishment of the Danish Compromise represents a broader shift toward regulatory pragmatism over ideological purity in European financial regulation. Regulators are increasingly willing to accept regulatory complexity in exchange for strategic advantages for European institutions, marking a departure from previous emphasis on level playing fields and competitive neutrality. This trend toward regulatory nationalism is likely to accelerate as geopolitical tensions increase and financial services become viewed as strategic assets.

The ESMA supervision initiative represents the most significant transfer of financial regulatory authority from national to European level since the establishment of the European Central Bank. Success in asset management supervision could create precedents for broader financial services integration, while failure could reinforce national regulatory preferences. The outcome will significantly influence the future architecture of European financial regulation and the viability of deeper integration initiatives.

Investment Implications and Strategic Recommendations

For institutional investors, the European regulatory transformation creates both opportunities and risks that require careful strategic positioning. Direct investment in consolidating European asset managers offers exposure to regulatory tailwinds and scale advantages but requires careful selection of managers with appropriate regulatory positioning and growth capabilities. The emergence of mega-platforms creates new due diligence challenges as traditional performance metrics become less relevant than regulatory compliance and integration capabilities.

Private equity investors face particular challenges and opportunities in the evolving European landscape. Traditional asset management buyout strategies may become less viable as regulatory compliance costs increase and integration complexity grows. However, distressed situations and regulatory-driven divestitures create new investment opportunities for sophisticated investors capable of navigating complex regulatory requirements. The 12-18 month implementation window for AIFMD 2.0 creates timing opportunities for acquirers willing to bear transition risks.

Strategic corporate investors, particularly banks and insurance companies, should accelerate their evaluation of asset management acquisition opportunities as regulatory advantages become more apparent and acquisition targets become scarcer. The Danish Compromise benefits are most valuable for institutions that can structure transactions appropriately and navigate ECB interpretation challenges. Delay in pursuing strategic acquisitions may result in significantly higher prices as regulatory tailwinds drive competitive bidding for scarce targets.

Conclusion: The New European Asset Management Paradigm

The regulatory transformation of European asset management represents far more than technical rule adjustments—it constitutes a fundamental reshaping of global financial services competition through strategic regulatory policy. The combination of the Danish Compromise’s permanent establishment, AIFMD 2.0’s compliance requirements, and the Single Investment Union’s integration initiatives creates a powerful triumvirate of forces driving unprecedented consolidation across European markets.

The BNP Paribas-AXA Investment Managers transaction, despite regulatory complications, demonstrates both the potential and complexity of the new regulatory environment. Creating a €1.5 trillion platform positions European asset management to compete globally while benefiting from regulatory tailwinds unavailable to international competitors. The transaction’s execution challenges also highlight the importance of sophisticated regulatory strategy in navigating increasingly complex approval processes and supervisory interpretations.

For global asset management, the European regulatory revolution creates a new competitive reality where regulatory positioning becomes as important as investment performance or operational efficiency. International managers must choose between accepting peripheral status in European markets or making substantial investments in European operations that comply with increasingly demanding regulatory requirements. The window for strategic positioning is narrowing rapidly as consolidation eliminates attractive acquisition targets and regulatory barriers to entry continue rising.

The success of European regulatory integration in driving asset management consolidation offers important lessons for other major financial centers facing similar competitive pressures. The strategic use of regulatory policy to encourage domestic consolidation while maintaining international competitiveness represents a sophisticated approach to financial services development that other jurisdictions are likely to emulate. The global implications extend far beyond European borders as competitive dynamics shift and regulatory frameworks evolve in response to changing geopolitical realities.

Looking ahead, the European asset management industry will emerge from this regulatory transformation fundamentally changed in structure, competitive dynamics, and global positioning. The success of these initiatives in creating scale-competitive European champions while maintaining market efficiency and investor protection will influence financial services policy globally and determine whether regulatory nationalism represents the future of international financial services competition.

Ready to navigate the European regulatory transformation? Our specialized M&A advisory services help institutional investors and strategic acquirers capitalize on regulatory-driven consolidation opportunities in European asset management. From Danish Compromise structuring to AIFMD 2.0 compliance strategies, we provide comprehensive regulatory intelligence and transaction execution expertise. Contact us today to explore how European regulatory changes create compelling investment and acquisition opportunities in the evolving global asset management landscape.

Leave a Reply