The environmental, social, and governance (ESG) investment landscape is experiencing its most profound transformation since the sustainable investing movement began, with regulatory pressure and political backlash forcing a fundamental reshaping of portfolio strategies worth over $500 billion globally. What began as a targeted political response in red states has evolved into a comprehensive recalibration of investment approaches, driving record outflows of $8.6 billion from global sustainable funds in Q1 2025 and forcing asset managers to navigate an increasingly complex regulatory environment that varies dramatically by jurisdiction.

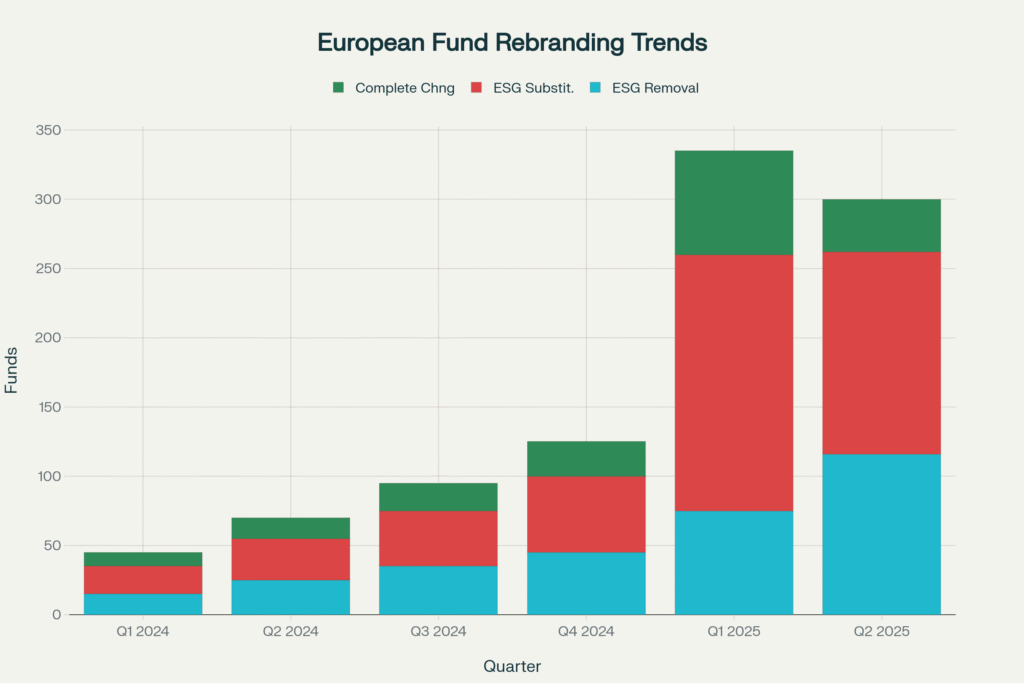

The scale of this transformation is unprecedented: 80% of corporations are reworking their ESG strategies, with 52% moving away from ESG terminology entirely. In Europe, 335 sustainable funds changed their names in Q1 2025 alone, including 116 that removed ESG terms altogether. Meanwhile, major financial institutions including BlackRock, JPMorgan, and all six largest U.S. banks have withdrawn from net-zero commitments amid mounting legal and political pressure. This comprehensive analysis examines how regulatory pressure is forcing a fundamental realignment of global investment strategies and what it means for the future of sustainable finance.

The Great ESG Reversal: From Record Inflows to Historic Outflows

Global Flow Dynamics Reveal Systematic Retreat

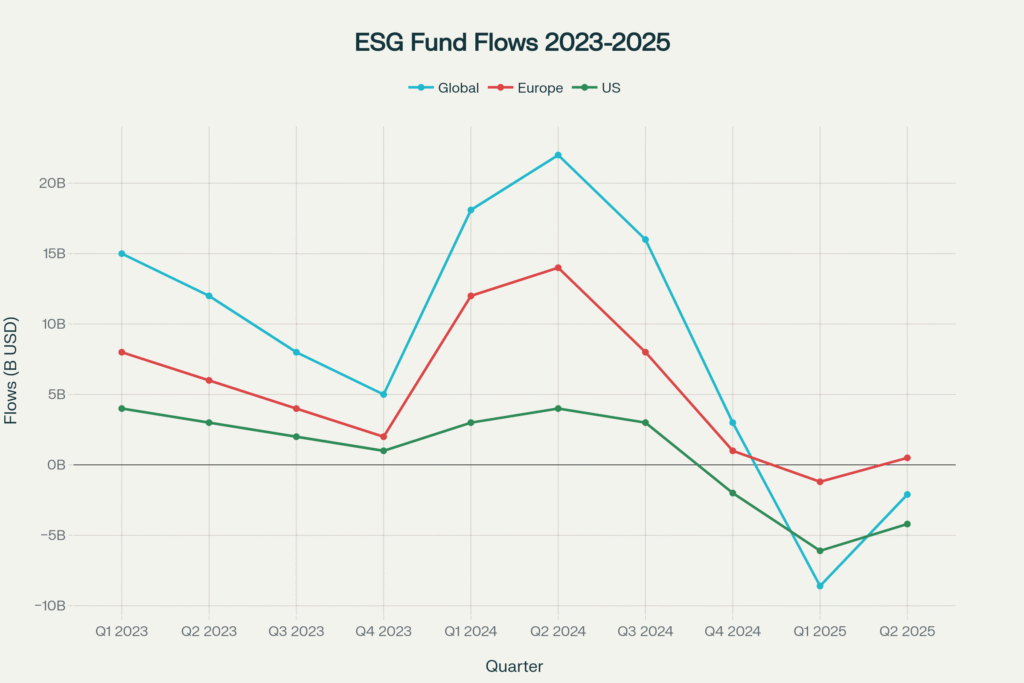

The magnitude of the ESG investment reversal becomes clear through flow data that reveals a systematic retreat from sustainable investment strategies across all major markets. Global sustainable funds recorded unprecedented outflows of $8.6 billion in Q1 2025, marking the first time since ESG’s mainstream adoption that global flows turned negative. This dramatic reversal followed $18.1 billion in inflows during Q1 2024, indicating that the shift represents more than cyclical market movements—it reflects a fundamental recalibration of investor sentiment and regulatory risk assessment.

The United States led this retreat with $6.1 billion in outflows during Q1 2025, marking the tenth consecutive quarter of declines. This sustained pattern reflects the cumulative impact of anti-ESG legislation, political pressure, and regulatory uncertainty that has made ESG investing increasingly challenging for U.S. institutions. European markets, historically the strongest supporters of sustainable investing, experienced their first quarterly outflows since 2018, with $1.2 billion in redemptions. This European reversal is particularly significant given that the region accounts for approximately 80% of global sustainable assets under management.

The breadth of outflows extended beyond traditional ESG funds to impact the strictest sustainable investment categories. Article 9 funds under Europe’s Sustainable Finance Disclosure Regulation (SFDR) suffered record outflows of €7.3 billion in Q4 2024, more than double the previous quarter’s withdrawals. These funds, which maintain the highest sustainability standards and most stringent investment criteria, have experienced five consecutive quarters of outflows, indicating that even the most committed sustainable investors are reconsidering their allocations amid regulatory uncertainty and performance pressures.

Performance and Political Factors Drive Institutional Repositioning

The ESG outflow phenomenon reflects a complex interplay of performance concerns, regulatory pressures, and political developments that have fundamentally altered the risk-return calculus for sustainable investing. Poor performance in clean energy stocks, which comprise significant portions of many ESG portfolios, has contributed to investor skepticism about the sector’s ability to deliver competitive returns. Many ESG funds concentrated in renewable energy sectors underperformed broader market indices during 2024, leading institutional investors to question whether sustainability criteria were constraining performance potential.

Political developments, particularly the return of the Trump administration, have created a hostile environment for ESG investing that extends beyond U.S. borders. The administration’s rollback of climate and diversity-related initiatives has emboldened critics of ESG investing globally, creating uncertainty about the future regulatory environment and potential legal challenges facing sustainable investment strategies. 78% of executives identify U.S. federal policymakers and regulators as the most significant drivers of ESG backlash, representing a shift from previous years when activist groups and advocacy organizations were considered primary sources of opposition.

Regulatory complexity and compliance costs have emerged as significant barriers to ESG adoption, particularly affecting smaller asset managers and institutional investors with limited resources. The proliferation of ESG regulations across different jurisdictions—often with conflicting requirements and definitions—has created a compliance burden that many firms find increasingly difficult to justify given uncertain commercial benefits. Regulatory fragmentation has become the top challenge for corporate sustainability efforts, with firms struggling to navigate divergent requirements across markets while maintaining coherent investment strategies.

Regulatory Pressure: A Multi-Jurisdictional Challenge

U.S. Anti-ESG Legislation Creates Systemic Barriers

The United States has witnessed an unprecedented wave of anti-ESG legislation that has fundamentally altered the investment landscape for sustainable strategies. More than 20 states have passed laws or taken administrative action targeting ESG considerations in asset management, with measures ranging from divestment requirements to restrictions on state pension fund investments. These legislative initiatives have created a complex patchwork of regulations that force institutional investors to choose between compliance with state mandates and adherence to fiduciary duties.

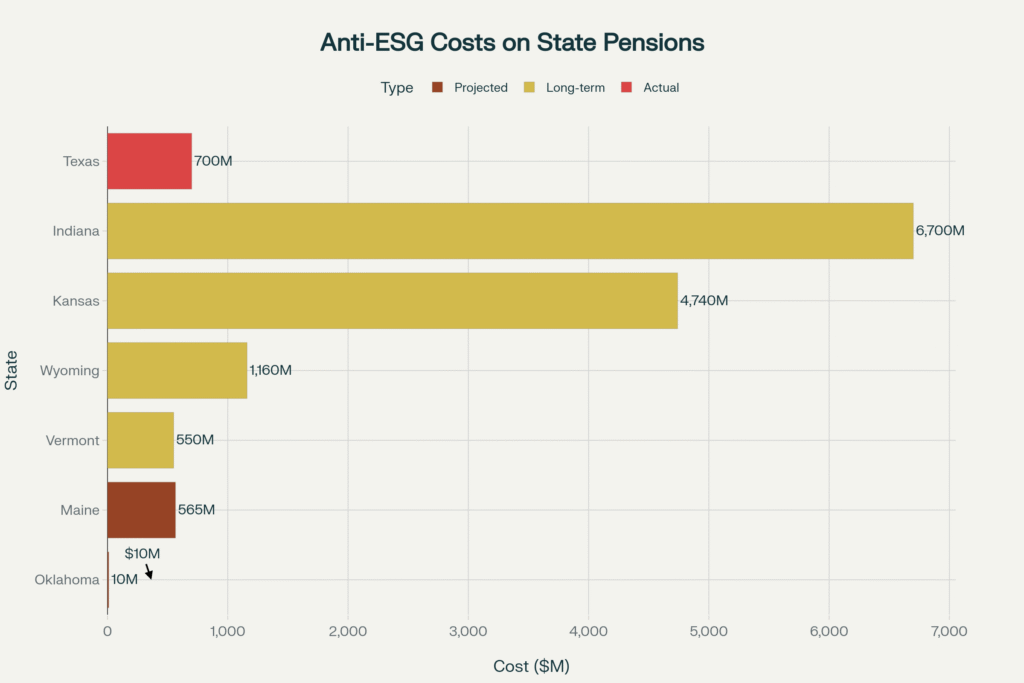

The financial impact of anti-ESG legislation has been substantial and well-documented. Texas’s anti-ESG laws cost the state more than $700 million in 2022-2023, according to the Texas Association of Business. Similar financial consequences have emerged across multiple states: Kansas estimated potential losses of $1.14 billion from immediate divestments and $3.6 billion in reduced earnings over the next decade from proposed ESG restrictions. Indiana’s original anti-ESG proposal could have led to $6.7 billion in reduced investment earnings over the next decade, forcing lawmakers to significantly amend the legislation.

The legal and compliance challenges extend beyond direct financial costs to encompass operational complexities and fiduciary conflicts. Pension fund trustees find themselves caught between conflicting obligations: their fiduciary duty to maximize returns for beneficiaries and state legislative mandates that may require them to forgo potentially profitable investments. Oklahoma’s Public Employees’ Retirement System conducted exhaustive research finding that divesting from BlackRock and State Street would cost approximately $10 million, leading the board to vote 9-1 for an exemption despite state treasurer opposition.

European Regulatory Uncertainty and Reform Initiatives

European markets, despite their historical leadership in sustainable finance, are experiencing significant regulatory uncertainty as policymakers grapple with the practical implementation of ambitious ESG frameworks. The European Commission’s February 2025 “Omnibus Proposal” aims to simplify sustainability regulations but has effectively reduced reporting requirements for an estimated 80% of companies. This dramatic scaling back of disclosure obligations reflects growing concerns about regulatory burden and competitiveness impacts that mirror criticisms emerging from the business community.

The Sustainable Finance Disclosure Regulation (SFDR) review, scheduled for Q4 2025, represents a critical inflection point for European sustainable finance policy. The regulation, which created the de facto labeling system for sustainable funds through Articles 6, 8, and 9 classifications, has faced criticism for complexity and unclear implementation guidance. Article 8 funds attracted €52 billion in Q1 2025, their highest inflows since late 2021, while Article 9 funds continued experiencing outflows for the sixth consecutive quarter. This divergence suggests investors are gravitating toward less stringent sustainability requirements amid regulatory uncertainty.

Corporate reporting requirements under the Corporate Sustainability Reporting Directive (CSRD) face increasing opposition from business leaders and national governments. France and Germany have publicly criticized the directive, with France describing the rules as “hell” for businesses under excessive administrative burdens. German Chancellor and French President formally urged the EU to abandon the Corporate Sustainability Due Diligence Directive, citing competitiveness risks and echoing calls to simplify or pause ESG regulations. This high-level political opposition reflects broader concerns about the cumulative impact of ESG regulations on European business competitiveness.

Global Regulatory Fragmentation and Compliance Challenges

The proliferation of ESG regulations across jurisdictions has created a complex web of compliance requirements that challenge even the largest global asset managers. Different regulatory frameworks often contain conflicting definitions, reporting standards, and investment criteria, forcing firms to maintain separate compliance infrastructures for different markets. The UK’s Sustainability Disclosure Requirements (SDR), the EU’s SFDR, and various U.S. state-level requirements each impose distinct obligations that can conflict with one another.

Regulatory enforcement has become increasingly aggressive across multiple jurisdictions, with authorities moving from guidance to active prosecution of greenwashing and ESG-related violations. Deutsche Bank’s asset management arm, DWS, was fined €25 million by German prosecutors for misleading investors about ESG credentials. The UK’s Competition and Markets Authority announced it will begin large-scale public enforcement of its Green Claims Code starting in autumn 2025, signaling a shift toward active regulatory prosecution of ESG-related violations.

International coordination efforts have largely failed to address regulatory fragmentation, with different jurisdictions pursuing distinct approaches that reflect domestic political priorities rather than global standards. The absence of harmonized international standards means that asset managers must navigate a complex maze of potentially conflicting requirements, creating operational challenges and compliance costs that disproportionately affect smaller firms and emerging market participants.

Portfolio Strategy Transformation: Asset Manager Responses

Massive Fund Rebranding and Strategic Repositioning

Asset managers have responded to regulatory pressure and political backlash through unprecedented rebranding efforts designed to reduce exposure to ESG-related controversy while maintaining access to sustainability-focused capital. European fund rebranding activity accelerated dramatically in Q1 2025, with 335 Article 8 and Article 9 funds with ESG-related terms undergoing name changes. This surge in rebranding activity reflects strategic positioning ahead of ESMA’s anti-greenwashing rule implementation, which required compliance by May 21, 2025.

The scope of rebranding extends beyond superficial name changes to encompass fundamental strategy modifications. 185 funds swapped ESG-related terms for alternative language like “sustainable,” “responsible,” or “impact,” while 75 funds removed ESG terminology altogether. This linguistic shift represents more than marketing adjustment—it reflects strategic positioning to avoid regulatory scrutiny while maintaining appeal to sustainability-conscious investors who may be less sensitive to specific terminology than to underlying investment approaches.

Fund liquidations and mergers have accelerated as asset managers rationalize their sustainable investment offerings. 94 sustainable funds were either merged or liquidated during Q1 2025, representing a significant consolidation of the European ESG fund landscape. This consolidation reflects both regulatory pressure and commercial reality, as asset managers focus resources on higher-performing vehicles while eliminating funds that no longer attract sufficient investor interest or generate adequate revenue to justify compliance costs.

Institutional Investor Strategy Recalibration

Institutional investors are implementing sophisticated strategies to maintain exposure to sustainability themes while reducing regulatory and reputational risks associated with explicit ESG commitments. Major pension funds are adopting what industry experts term “green-hushing” strategies, maintaining climate-conscious investment approaches while avoiding public sustainability commitments that might attract political attention. This approach allows institutions to fulfill fiduciary duties while avoiding the regulatory and political complications associated with explicit ESG branding.

Asset allocation strategies are shifting toward sector-specific approaches rather than broad ESG mandates. Rather than implementing comprehensive ESG screens across entire portfolios, institutional investors are focusing on specific sectors where sustainability factors have clear financial materiality—such as renewable energy infrastructure, water resources, and technology companies with strong governance practices. This targeted approach provides exposure to sustainability themes while avoiding the political complications associated with broad-based ESG strategies.

International diversification has become a key strategy for U.S. institutional investors seeking to maintain sustainable investment exposure while complying with domestic anti-ESG regulations. By allocating capital to international funds and strategies domiciled outside anti-ESG jurisdictions, these investors can maintain sustainability-focused allocations while technically complying with state-level restrictions. However, this approach requires careful legal structuring and may face challenges as anti-ESG advocates become more sophisticated in their regulatory approaches.

Corporate Strategy and Governance Adaptations

Corporate issuers are fundamentally restructuring their sustainability communications and governance practices in response to the changing regulatory and political environment. 52% of surveyed executives report reworking sustainability messaging, including moving away from the term “ESG”. This shift reflects strategic positioning to maintain sustainability initiatives while reducing exposure to political and regulatory backlash that has targeted companies with prominent ESG commitments.

Corporate sustainability strategies increasingly emphasize financial materiality over stakeholder capitalism themes, focusing on sustainability factors that have clear connections to operational efficiency, risk management, and long-term value creation. This approach allows companies to maintain sustainability initiatives while framing them in terms of traditional business objectives rather than social or environmental impact. 66% of executives say tariffs will hinder progress on sustainability goals, forcing companies to balance sustainability commitments against cost pressures and supply chain considerations.

Board composition and committee structures are adapting to de-emphasize explicit ESG oversight while maintaining substantive attention to sustainability issues. Many companies are integrating sustainability oversight into existing risk management and audit committees rather than maintaining separate ESG or sustainability committees that might attract regulatory attention. This structural approach maintains corporate governance attention to sustainability issues while reducing the visibility that has made ESG initiatives targets for political opposition.

Financial Impact and Market Consequences

Quantifying the Cost of Regulatory Pressure

The financial impact of ESG backlash extends far beyond simple fund outflows to encompass systematic costs imposed on institutional investors, corporations, and the broader financial system. Direct costs to state pension systems from anti-ESG legislation have exceeded $1 billion annually across affected states, with Texas alone incurring over $700 million in additional costs during 2022-2023. These costs reflect the economic inefficiency of politically-motivated investment restrictions that force pension systems to forgo potentially profitable investment opportunities or incur additional transaction costs from required portfolio adjustments.

Corporate compliance costs have escalated dramatically as companies navigate conflicting regulatory requirements across jurisdictions. The complexity of maintaining separate sustainability reporting and governance systems for different markets has created substantial operational expenses, particularly for multinational corporations operating in both ESG-supportive and ESG-hostile jurisdictions. Regulatory fragmentation has become the top challenge for corporate sustainability efforts, with compliance costs estimated to consume 2-5% of sustainability budgets for large multinational corporations.

Asset management industry consolidation has accelerated as smaller firms struggle to absorb regulatory compliance costs while maintaining competitive investment offerings. The fixed costs of ESG compliance—including data acquisition, reporting systems, legal consultation, and regulatory monitoring—create economies of scale that favor larger asset managers over smaller specialists. This consolidation trend reduces competition and innovation in sustainable investment strategies while concentrating industry assets among firms with sufficient resources to navigate complex regulatory environments.

Market Structure and Competitive Implications

The ESG backlash has created fundamental shifts in market structure that extend beyond sustainable investing to affect broader capital allocation patterns and competitive dynamics. The withdrawal of major U.S. financial institutions from international climate commitments has reduced the influence of American capital in global sustainability initiatives, potentially shifting leadership toward European and Asian institutions that maintain stronger commitments to sustainable finance principles.

Credit and capital markets are experiencing bifurcation between ESG-supportive and ESG-hostile jurisdictions, creating potential arbitrage opportunities for sophisticated investors while imposing additional costs on issuers seeking broad market access. Companies and financial institutions may need to maintain separate financing strategies for different markets, potentially increasing capital costs and reducing market efficiency. This fragmentation could ultimately disadvantage U.S. capital markets if international investors increasingly prefer jurisdictions with clearer sustainability frameworks.

Innovation in sustainable finance has shifted toward jurisdictions with supportive regulatory environments, potentially creating long-term competitive disadvantages for markets with restrictive ESG policies. The development of new sustainable finance instruments, including green bonds, sustainability-linked loans, and transition finance products, is increasingly concentrated in European and Asian markets rather than U.S. financial centers. This geographic shift in innovation could have lasting implications for the competitiveness of different financial systems as sustainable finance becomes more mainstream globally.

Regional Divergence: Different Approaches to Sustainable Finance

European Resilience Amid Regulatory Reform

Despite regulatory uncertainty and political pressure, European markets have demonstrated relative resilience in maintaining commitment to sustainable finance principles while adapting to practical implementation challenges. European Article 8 funds attracted €52 billion in Q1 2025, their highest inflows since late 2021, suggesting that investor demand for sustainability-focused strategies remains strong despite political and regulatory headwinds. This resilience reflects both the maturity of European sustainable finance markets and the integration of sustainability considerations into broader investment decision-making processes.

European regulatory reforms emphasize practical implementation improvements rather than fundamental philosophical shifts away from sustainable finance. The EU Commission’s taxonomy review and SFDR revision aim to simplify compliance requirements and improve regulatory clarity rather than eliminating sustainability considerations from investment decisions. The Platform on Sustainable Finance’s recommendations could reduce reporting burden on non-financial companies by over a third, addressing practical concerns while maintaining the fundamental framework for sustainable finance regulation.

Corporate adaptation in European markets focuses on operational efficiency rather than strategic retreat from sustainability commitments. European companies are investing in systems and processes to manage complex regulatory requirements while maintaining substantive attention to environmental and social factors. This approach reflects confidence that sustainable finance regulation will remain a permanent feature of European markets, making compliance investment a necessary component of long-term competitive positioning.

U.S. Market Fragmentation and Adaptation

The United States has experienced the most dramatic fragmentation in sustainable finance approaches, with stark differences emerging between states, institutional investor types, and political jurisdictions. Blue states continue implementing pro-ESG policies, with California requiring climate-related disclosures and prohibiting thermal coal investments by state pension funds, while red states pursue increasingly aggressive anti-ESG measures including asset manager boycotts and investment restrictions.

Federal policy uncertainty under the current administration adds complexity to an already challenging regulatory environment. The administration’s efforts to overturn Biden-era ESG rules for retirement plans, combined with congressional investigations and Department of Justice antitrust actions, create legal and regulatory risks that extend beyond state-level measures. The DOL’s commitment to replacing ESG rules by May 2026 adds temporal uncertainty that complicates long-term strategic planning for institutional investors.

Market innovation in the U.S. has shifted toward implicit sustainability strategies that avoid explicit ESG branding while maintaining substantive attention to environmental and social factors. Asset managers are developing investment approaches that integrate sustainability considerations through traditional financial analysis rather than specialized ESG frameworks, potentially creating more resilient strategies that can withstand political criticism while delivering similar investment outcomes.

Emerging Market Responses and Opportunities

Emerging markets are positioning themselves to capitalize on sustainable finance opportunities as developed markets grapple with political and regulatory challenges. India’s comprehensive framework for social, sustainability, and sustainability-linked bonds represents a major regulatory step to boost credibility and accountability in ESG debt markets. This proactive approach contrasts with the regulatory retreat occurring in some developed markets and positions India as a potential leader in sustainable finance innovation.

Asian financial centers, particularly Singapore and Hong Kong, are attracting sustainable finance business from institutions seeking stable regulatory environments with clear sustainability frameworks. These jurisdictions benefit from political systems that can implement consistent policies without the partisan divisions affecting U.S. and, to some extent, European markets. The concentration of sustainable finance activity in these centers could create lasting competitive advantages as the global economy becomes more focused on sustainability transitions.

Regional taxonomy and regulatory development efforts are creating alternative frameworks to European and U.S. approaches, potentially offering more flexible and practical approaches to sustainable finance regulation. These regional initiatives may attract international capital seeking alternatives to the increasingly complex and politicized regulatory environments in traditional financial centers.

Strategic Implications and Future Outlook

Asset Manager Strategic Positioning

Asset managers face fundamental strategic choices about how to position their businesses in an environment where sustainable finance remains commercially important but politically controversial. Firms are adopting more sophisticated communication strategies that emphasize financial materiality and risk management rather than social impact or environmental advocacy. This approach allows managers to maintain substantive attention to sustainability factors while reducing exposure to political backlash and regulatory scrutiny.

Product development is shifting toward implicit sustainability integration rather than explicit ESG branding, with managers developing investment strategies that incorporate environmental and social factors through traditional financial analysis frameworks. This approach may prove more resilient to political criticism while delivering similar investment outcomes, potentially representing the future evolution of sustainable investing beyond the current backlash period.

Geographic diversification strategies are becoming increasingly important as firms seek to maintain global sustainable finance capabilities while complying with regional restrictions. Asset managers are establishing separate operational structures for different jurisdictions, allowing them to offer ESG-compliant products in supportive markets while maintaining compliant operations in restrictive jurisdictions.

Institutional Investor Adaptation Strategies

Institutional investors are developing sophisticated approaches to maintain sustainability-focused investment strategies while navigating complex regulatory and political environments. Pension funds are increasingly adopting materiality-focused approaches that emphasize financial relevance of environmental and social factors rather than broader stakeholder capitalism themes, providing stronger defense against political criticism while maintaining substantive attention to sustainability issues.

Investment committee governance structures are evolving to integrate sustainability considerations into traditional risk management and investment oversight processes rather than maintaining separate ESG committees that might attract political attention. This structural approach maintains institutional attention to sustainability factors while reducing visibility that has made ESG initiatives targets for opposition.

Legal and compliance strategies are becoming increasingly sophisticated as institutions work to maintain fiduciary compliance while navigating anti-ESG regulations. This includes developing clear documentation of financial materiality for sustainability-related investment decisions and maintaining robust legal defenses for investment approaches that might face political challenge.

Long-term Market Evolution

The current ESG backlash period may represent a necessary evolution toward more sophisticated and resilient approaches to sustainable investing rather than a fundamental rejection of sustainability considerations in investment decisions. Market forces driving attention to environmental and social factors—including climate risk, resource scarcity, and demographic transitions—remain structurally important regardless of political and regulatory developments.

The integration of sustainability factors into mainstream investment analysis may ultimately prove more durable than specialized ESG approaches that can be targeted by political opposition. As sustainability considerations become embedded in traditional financial analysis rather than separate overlay processes, they may become less visible to political criticism while maintaining substantive influence on investment decisions.

International competition for sustainable finance business may ultimately reward jurisdictions with clear, stable regulatory frameworks over those with restrictive or uncertain policies. This competitive dynamic could create pressure for policy convergence around practical sustainable finance approaches that balance commercial objectives with environmental and social considerations.

Conclusion: Navigating the Transformation of Sustainable Finance

The ESG investment backlash represents a watershed moment that is fundamentally reshaping the landscape of sustainable finance, forcing a evolution from advocacy-driven approaches toward more sophisticated integration of environmental and social factors into mainstream investment decision-making. The $8.6 billion in global outflows during Q1 2025 and the withdrawal of major financial institutions from climate commitments signal not the end of sustainable investing, but its transformation into more resilient and financially-focused approaches that can withstand political scrutiny while maintaining substantive attention to material sustainability factors.

The regulatory pressure driving this transformation has created both challenges and opportunities for institutional investors, asset managers, and corporations. While anti-ESG legislation has imposed significant costs on some institutions and forced strategic repositioning across the industry, it has also accelerated the development of more sophisticated approaches to sustainability integration that may prove more durable over time. The 335 European funds that rebranded in Q1 2025 and the systematic strategy changes being implemented globally represent adaptive responses rather than wholesale retreat from sustainability considerations.

The regional divergence in approaches to sustainable finance reflects broader geopolitical and economic competition that will likely intensify as climate change and resource constraints become more pressing global challenges. European markets’ relative resilience and continued innovation in sustainable finance regulation, combined with emerging markets’ proactive development of sustainable finance frameworks, suggest that the current U.S.-led backlash may ultimately disadvantage American financial markets in the long term.

For forward-thinking institutional investors and asset managers, the current environment presents opportunities to develop more resilient and sophisticated approaches to sustainable investing that can thrive regardless of political and regulatory volatility. The key to success lies in focusing on financial materiality, maintaining operational flexibility across jurisdictions, and developing communication strategies that emphasize risk management and value creation rather than social advocacy.

The ultimate outcome of the current transformation will likely be a more mature and financially-focused approach to sustainable investing that integrates environmental and social considerations into mainstream investment processes rather than treating them as separate overlay strategies. This evolution may prove beneficial for both investment performance and long-term sustainability outcomes, creating more robust frameworks for addressing the material environmental and social challenges that will continue to influence global economic development regardless of short-term political opposition.

Ready to navigate the evolving sustainable finance landscape? Our specialized advisory services help institutional investors and asset managers develop resilient ESG strategies that balance regulatory compliance, political risk management, and sustainable investment objectives. From regulatory intelligence to strategic repositioning, we provide comprehensive support for organizations adapting to the transformed sustainable finance environment. Contact us today to explore how the current market transformation creates both challenges and opportunities in sustainable investing.

Leave a Reply