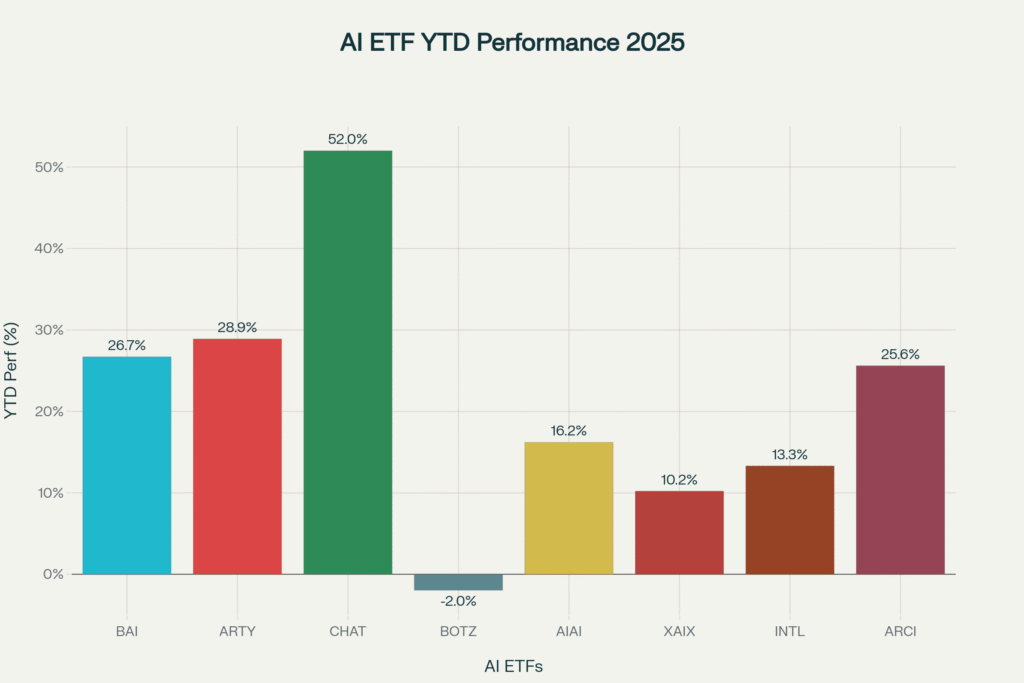

The artificial intelligence investment revolution has reached a pivotal inflection point in 2025, with specialized AI ETFs delivering exceptional returns that vastly outperform broader market indices. BlackRock’s iShares AI Innovation and Tech Active ETF (BAI) stands as the flagship example, surging 36% since its October 2024 inception and posting a robust 26.7% year-to-date return through October 2025. This remarkable performance reflects the underlying transformation of global technology infrastructure as organizations commit unprecedented capital to AI development and deployment.

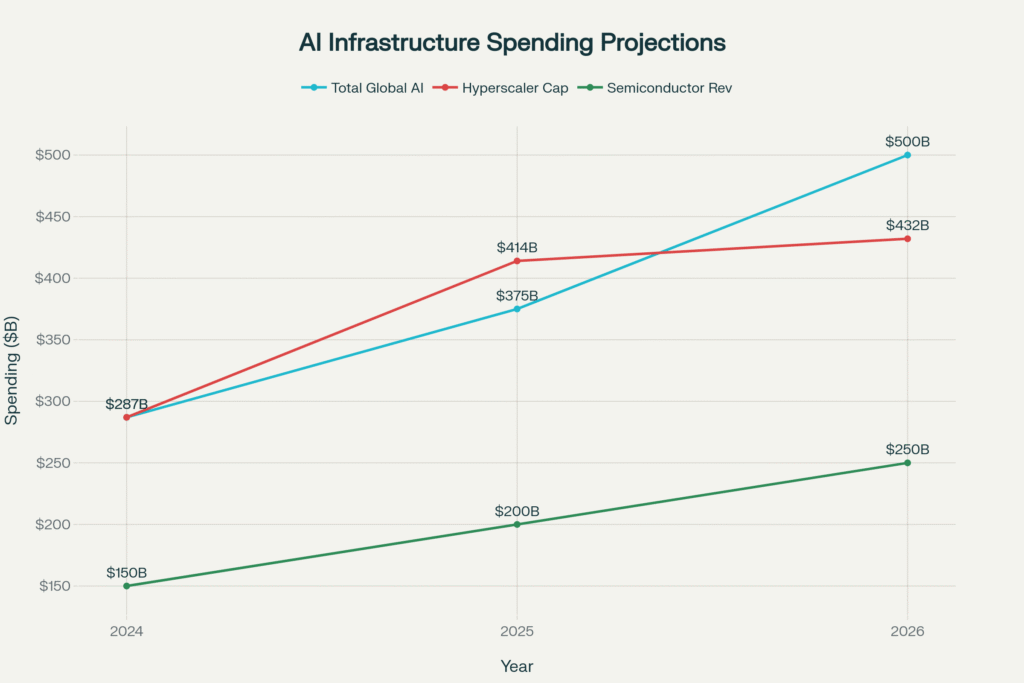

The AI ETF sector’s strength stems from a perfect convergence of factors: global AI spending projected to reach $375 billion in 2025 and $500 billion by 2026, hyperscaler capital expenditures exceeding $414 billion annually, and semiconductor companies reporting record-breaking AI-related revenues approaching $200 billion. This comprehensive analysis examines the fundamental drivers behind AI ETF outperformance, the strategic positioning that differentiates leading funds, and the investment implications of the ongoing AI infrastructure buildout.

The AI Infrastructure Investment Revolution

Unprecedented Capital Deployment Scale

The magnitude of capital flowing into AI infrastructure in 2025 represents one of the largest technology investment cycles in modern history. Bank of America projects total AI capital expenditures of $414 billion in 2025, representing a 44% increase from 2024 levels, with expectations for continued growth to $432 billion in 2026. This spending surge encompasses the full AI technology stack, from advanced semiconductors and high-performance computing systems to data center infrastructure and specialized software platforms.

The “Big Four” hyperscalers—Amazon Web Services, Google, Microsoft, and Meta—are driving the majority of this investment, with combined guidance approaching $417 billion in cloud infrastructure spending for 2025. Meta has raised its capital expenditure guidance from $60-65 billion to $64-72 billion, while Microsoft reaffirmed plans for approximately $80 billion in AI-focused investments. Amazon maintains its $105 billion capital expenditure outlook, with the majority allocated to AI and cloud infrastructure expansion.

NVIDIA CEO Jensen Huang’s assertion that the top four hyperscalers will spend approximately $600 billion annually reflects the exponential trajectory of AI infrastructure investment, even if current guidance suggests a more conservative $400-450 billion range. This discrepancy likely reflects the dynamic nature of AI investment planning, where spending often accelerates beyond initial projections as competitive pressures and technological opportunities expand.

Sector-Specific Investment Patterns

The AI infrastructure boom exhibits distinct investment patterns across different technology segments, creating differentiated opportunities for specialized ETFs. Semiconductor companies report the most dramatic growth trajectories, with AI chip sales projected to generate over $150 billion in revenue during 2025 and potentially reaching $200 billion by year-end. This growth is concentrated in advanced manufacturing nodes, with companies like TSMC expecting AI accelerator revenue to grow at a mid-40% compound annual growth rate through 2029.

Data center infrastructure represents the second-largest investment category, encompassing power systems, cooling technologies, networking equipment, and specialized facilities designed for AI workloads. Global data center power demand is projected to double by 2030, with AI applications requiring unprecedented power densities exceeding 100-250 kilowatts per rack compared to traditional deployments of 10-15 kW. This infrastructure challenge is creating massive opportunities for companies specializing in power management, cooling systems, and facility design.

Software and platform investments constitute the third major category, with organizations allocating significant capital to AI development tools, machine learning platforms, and enterprise AI applications. Adobe, SAP, ServiceNow, Salesforce, and Intuit maintain stable revenue growth momentum as enterprises integrate AI capabilities across their operations. This software layer provides recurring revenue streams that complement the more volatile hardware investment cycles.

BlackRock’s BAI: Strategic Positioning and Active Management Advantage

Portfolio Construction and Holdings Analysis

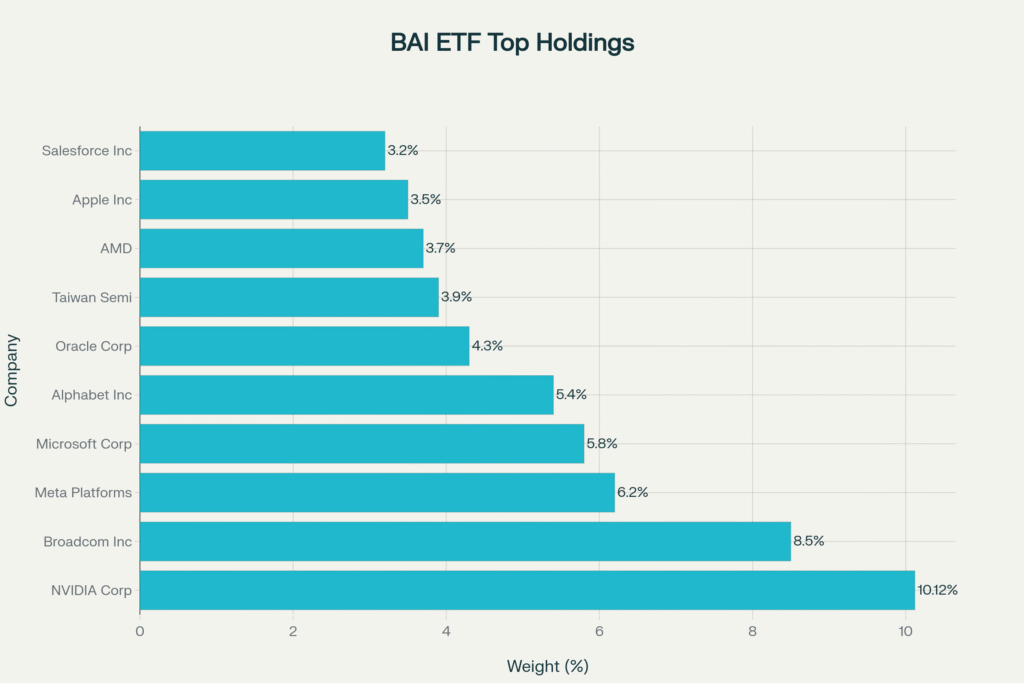

BAI’s exceptional performance stems from its actively managed approach to AI investment, enabling dynamic allocation adjustments based on evolving market conditions and technological developments. The fund maintains a concentrated portfolio of approximately 50-60 holdings, with the top 10 positions representing over 50% of total assets. This concentration strategy allows the fund to capture maximum upside from the highest-conviction AI infrastructure plays while maintaining sufficient diversification to manage risk.

NVIDIA Corporation commands the largest position at 10.12% of portfolio assets, reflecting the company’s dominant position in AI training and inference chip markets. This allocation has proven prescient, with NVIDIA’s data center revenue exceeding $30 billion quarterly and the company maintaining over 70% market share in AI accelerator chips. The fund’s substantial NVIDIA exposure directly benefits from the company’s pricing power and the technical moats surrounding its CUDA software ecosystem.

Broadcom emerges as the second-largest holding at approximately 8.5%, positioned to capitalize on custom AI chip demand and networking infrastructure requirements. The company reported record Q3 2025 revenue of $16.0 billion with AI revenue accelerating 63% year-over-year to $5.2 billion. Broadcom’s expertise in application-specific integrated circuits (ASICs) positions it to benefit from hyperscaler efforts to develop proprietary AI chips optimized for specific workloads.

The fund’s technology platform holdings—including Meta Platforms (6.2%), Microsoft (5.8%), and Alphabet (5.4%)—provide exposure to AI application development and monetization. These companies represent the demand side of the AI infrastructure equation, with their massive capital expenditure commitments driving revenue growth for semiconductor and infrastructure suppliers. Their inclusion ensures BAI captures value creation across the entire AI ecosystem rather than just the supply side.

Active Management Value Creation

BAI’s active management approach distinguishes it from passive AI ETFs that rely on index methodologies, enabling more responsive positioning as AI market dynamics evolve. The fund’s expense ratio of 0.55% (after fee waivers) reflects BlackRock’s commitment to maintaining competitive costs while providing active management capabilities. This cost structure compares favorably to the 0.75% expense ratios typical of other actively managed AI funds while significantly exceeding the value creation potential of passive alternatives.

Fund manager Reid Menge’s technology sector expertise enables sophisticated security selection based on fundamental analysis rather than mechanical index inclusion criteria. This approach proves particularly valuable in the rapidly evolving AI landscape, where technological shifts can quickly alter competitive dynamics and investment attractiveness. The fund’s ability to adjust position sizes, add new holdings, and exit deteriorating positions provides significant advantages over rigid index tracking.

The fund’s concentrated approach amplifies the impact of successful stock selection, with top holdings generating disproportionate contributions to overall performance. BAI’s 26.7% year-to-date return through October 2025 significantly outperforms the broader technology sector and validates the active management premium. This outperformance occurs despite the fund’s higher expense ratio, demonstrating the value creation potential of skilled active management in emerging technology sectors.

Semiconductor Demand Surge: The Foundation of AI Infrastructure

Advanced Chip Manufacturing Bottlenecks

The semiconductor industry faces unprecedented demand for advanced AI chips, creating supply constraints that are reshaping global manufacturing capacity and investment priorities. The current shortage is highly concentrated in cutting-edge nodes below 7 nanometers, particularly the 3nm and emerging 2nm processes essential for next-generation AI accelerators. Unlike previous semiconductor shortages that affected broad chip categories, the 2025 constraints specifically impact the most advanced manufacturing capabilities required for AI applications.

Taiwan Semiconductor Manufacturing Company (TSMC) controls over 90% of advanced node capacity, making it the critical bottleneck for AI chip production. The company’s third-quarter 2025 profits surged 28% to record levels driven by insatiable AI infrastructure demand, while capacity utilization approaches maximum levels. TSMC’s advanced packaging capacity, particularly Chip-on-Wafer-on-Substrate (CoWoS) technology, has become the ultimate constraint, with NVIDIA reportedly securing over 70% of available capacity for its Blackwell architecture GPUs.

The substrate shortage, specifically Ajinomoto Build-up Film (ABF), represents a hidden constraint deeper in the supply chain that limits advanced packaging capabilities. This technical bottleneck affects all major AI chip manufacturers and has extended lead times for advanced processors from months to over a year in some cases. TSMC’s aggressive expansion targeting 70,000 CoWoS wafers per month by year-end 2025 and over 90,000 by 2026 still falls short of projected demand, creating sustained pricing power for advanced semiconductor manufacturers.

Memory and Storage Infrastructure Requirements

AI applications generate unprecedented demands for high-bandwidth memory and advanced storage systems, creating explosive growth opportunities for specialized semiconductor companies. High-Bandwidth Memory (HBM) demand has increased exponentially, with AI training applications requiring memory bandwidth exceeding 3 terabytes per second compared to traditional applications measuring in gigabytes. This demand surge has created severe supply constraints for HBM manufacturers, with lead times extending beyond 12 months for advanced memory configurations.

Samsung, SK Hynix, and Micron Technology dominate HBM production, with all three companies reporting record order backlogs and capacity utilization approaching 100%. Micron Technology’s revenue growth acceleration reflects this dynamic, with the company’s HBM revenue growing over 400% year-over-year in recent quarters. The technical complexity of HBM manufacturing, requiring advanced 3D stacking and through-silicon-via technology, creates significant barriers to entry and sustainable competitive advantages for existing producers.

Storage infrastructure for AI applications requires specialized solid-state drives (SSDs) optimized for mixed read-write workloads with extremely low latency requirements. Traditional enterprise storage systems prove inadequate for AI training and inference applications, necessitating new storage architectures that combine high-performance SSDs with intelligent caching and data management. Companies like Western Digital and Seagate report strong demand for AI-optimized storage solutions, with premium pricing reflecting the specialized performance requirements.

Hyperscaler Capital Expenditure Boom: Demand Drivers Analysis

Data Center Infrastructure Expansion

The global hyperscaler community is undertaking the largest data center infrastructure expansion in history, driven by AI workload requirements that far exceed traditional cloud computing demands. Microsoft’s $80 billion capital expenditure commitment for 2025 represents a 67% increase from previous years, with the majority allocated to AI-specific infrastructure including advanced GPUs, high-bandwidth networking, and specialized cooling systems. This investment scale dwarfs previous technology infrastructure cycles and reflects the winner-take-all dynamics emerging in AI platform competition.

Google (Alphabet) has raised its 2025 capital expenditure guidance to $85 billion, representing a substantial increase from previous projections and emphasizing AI infrastructure development. The company’s investments focus on custom AI chips (Tensor Processing Units), global data center expansion, and networking infrastructure capable of supporting massive AI training workloads. Google’s emphasis on custom silicon development creates additional demand for advanced semiconductor design and manufacturing services, benefiting companies across the AI chip ecosystem.

Amazon Web Services reported quarterly capital expenditures running at $31.4 billion, annualizing above $118 billion with the majority directed toward AI and cloud infrastructure. The company’s investment strategy emphasizes geographic expansion of AI-capable data centers, development of custom Graviton processors, and advanced networking technologies. AWS’s infrastructure investments directly benefit semiconductor suppliers, data center equipment manufacturers, and specialized component producers represented in leading AI ETFs.

Power and Energy Infrastructure Challenges

The exponential growth in AI data center deployments has created unprecedented challenges for power generation and distribution infrastructure, requiring massive investments in electrical systems and energy management technologies. Global electricity demand from data centers is projected to double by 2030 under base case scenarios and triple in upside cases, with AI applications consuming significantly more power per computation than traditional workloads. This power demand growth far exceeds available grid capacity in many regions, forcing hyperscalers to invest in distributed generation and energy storage technologies.

Individual AI training facilities now require over 1 gigawatt of power—equivalent to supplying nearly 1 million homes—creating entirely new categories of infrastructure demand. OpenAI’s GPT-4 training consumed approximately 30 megawatts of continuous power, while next-generation models anticipate multi-gigawatt requirements that exceed the capacity of traditional power plants. These power densities are driving investments in advanced cooling systems, power distribution technologies, and renewable energy generation specifically designed for AI workloads.

The power infrastructure challenge creates investment opportunities across multiple sectors, including utility-scale battery storage, advanced power management systems, and efficient cooling technologies. Companies specializing in data center power infrastructure report order backlogs extending multiple quarters, with premium pricing reflecting the urgent need for solutions that can support AI power densities. Bloom Energy’s recent $5 billion partnership with Brookfield Asset Management exemplifies the scale of investment required to address AI power infrastructure challenges.

Performance Drivers and Market Dynamics

Earnings Growth Acceleration

The AI infrastructure investment boom has translated into exceptional earnings growth for companies across the technology supply chain, validating the performance of AI-focused ETFs like BAI. NVIDIA’s data center revenue has grown from approximately $1 billion quarterly to over $30 billion, representing one of the fastest revenue acceleration cycles in corporate history. This growth stems from the company’s dominant position in AI training chips, where technical superiority and software ecosystem advantages create substantial competitive moats.

Broadcom’s AI-related revenue reached $5.2 billion in Q3 2025, accelerating 63% year-over-year as hyperscalers increasingly invest in custom AI chip solutions. The company’s expertise in high-performance networking, storage controllers, and custom silicon design positions it to benefit from multiple AI infrastructure trends simultaneously. Broadcom’s record $16.0 billion quarterly revenue and 30% adjusted EBITDA growth demonstrate the exceptional profitability available to companies with differentiated AI infrastructure capabilities.

Taiwan Semiconductor Manufacturing Company’s record quarterly profits reflect the premium pricing available for advanced AI chip manufacturing, with the company’s leading-edge processes commanding 50-100% higher margins than traditional semiconductor production. TSMC’s capital expenditure investments exceeding $25 billion annually ensure continued technology leadership while creating substantial barriers to entry for potential competitors. The company’s dominant market position in advanced nodes provides sustained pricing power as AI chip demand continues expanding.

Technology Innovation Cycles

The rapid pace of AI technology development creates continuous opportunities for innovation and investment across hardware, software, and infrastructure categories. NVIDIA’s Blackwell architecture represents a generational leap in AI processing capability, offering 2.5x performance improvements over previous generations while maintaining software compatibility. This innovation cycle drives continuous upgrade demand from hyperscalers seeking competitive advantages in AI model training and inference capabilities.

Advanced packaging technologies, including chip-on-wafer-on-substrate (CoWoS) and through-silicon-via (TSV) connections, enable new chip architectures that dramatically improve AI processing efficiency. These packaging innovations require sophisticated manufacturing capabilities and create additional value-added opportunities for semiconductor companies. The technical complexity of advanced packaging creates sustainable competitive advantages for companies with the manufacturing expertise and capacity to deliver these solutions at scale.

Software ecosystem development complements hardware innovations, with companies like Microsoft, Google, and Meta investing billions in AI development platforms and tools. These software investments create recurring revenue streams while driving additional hardware demand as developers deploy increasingly sophisticated AI applications. The symbiotic relationship between hardware and software innovation ensures sustained investment across the entire AI technology stack.

Competitive Landscape Among AI ETFs

Performance Differentiation Strategies

The AI ETF landscape exhibits significant performance dispersion based on different investment strategies, geographic focus, and sector concentration approaches. The Roundhill Generative AI and Technology ETF (CHAT) leads performance with a 52% year-to-date return, reflecting its concentrated focus on pure-play AI companies and generative AI applications. This concentrated approach amplifies both upside potential and volatility, attracting investors seeking maximum exposure to AI technology trends.

BAI’s 26.7% year-to-date performance positions it among the top-performing actively managed AI strategies, demonstrating the value of professional security selection and dynamic allocation adjustments. The fund’s active management approach enables responsive positioning as AI market dynamics evolve, providing advantages over passive strategies that rely on mechanical index inclusion criteria. BAI’s outperformance relative to broader technology indices validates the premium paid for specialized AI expertise.

Traditional robotics and automation ETFs like Global X Robotics & Artificial Intelligence (BOTZ) have underperformed with negative returns, reflecting their exposure to industrial automation companies that have not benefited from the generative AI boom. This performance divergence highlights the importance of investment strategy focus, with pure-play AI infrastructure funds significantly outperforming broader technology automation strategies.

Regional and Sector Allocation Differences

AI ETF performance varies significantly based on geographic exposure and sector allocation decisions, with U.S.-focused funds generally outperforming globally diversified alternatives. L&G Artificial Intelligence ETF’s 16.2% return reflects its balanced global approach, which includes European and Asian AI companies that have participated less directly in the U.S. hyperscaler investment boom. While this geographic diversification reduces concentration risk, it also limits exposure to the strongest-performing AI infrastructure companies.

European AI ETFs face additional challenges from slower AI adoption rates and limited access to advanced semiconductor manufacturing capabilities. The concentration of cutting-edge AI chip production in Taiwan and advanced AI model development in the United States creates geographic advantages that translate into superior ETF performance. WisdomTree Artificial Intelligence ETF’s 13.3% return demonstrates the impact of global diversification on performance during periods of U.S. AI leadership.

Sector allocation decisions significantly impact AI ETF performance, with funds emphasizing semiconductor exposure generally outperforming those focused on software applications or industrial automation. The Xtrackers Artificial Intelligence & Big Data ETF’s 10.2% return reflects its broader technology focus that includes cybersecurity and big data analytics companies with lower AI exposure. Pure-play AI infrastructure funds consistently outperform diversified technology strategies during periods of concentrated AI investment growth.

Risk Factors and Investment Considerations

Valuation and Bubble Concerns

The exceptional performance of AI ETFs has generated concerns about potential overvaluation and bubble formation, particularly given the concentration of gains among a relatively small number of companies. Leading AI infrastructure companies trade at forward price-to-earnings ratios around 35x, significantly below the 60x valuations common during the dot-com bubble but elevated relative to historical technology sector norms. The current valuations reflect high growth expectations that require sustained execution from both individual companies and the broader AI ecosystem.

Market concentration poses additional risks, with the top 10 AI infrastructure companies representing over 40% of total market capitalization in leading AI ETFs. This concentration amplifies both upside and downside potential, making AI ETF performance highly dependent on the continued success of a small number of key players. Any significant disappointment in AI adoption rates, competitive dynamics, or technology development could result in substantial performance reversals.

The sustainability of current AI investment spending levels remains uncertain, with some analysts questioning whether the massive capital expenditures will generate sufficient returns to justify continued growth. Deutsche Bank analysis suggests that without AI-related investments, the U.S. economy might already be experiencing recession conditions, highlighting the critical importance of AI spending to broader economic growth. A significant reduction in AI investment could have cascading effects across semiconductor, infrastructure, and technology sectors.

Technology and Competitive Risks

The rapid pace of AI technology development creates continuous risks of technological disruption and competitive displacement that could significantly impact AI ETF holdings. The emergence of more efficient AI architectures, such as those demonstrated by China’s DeepSeek model, could reduce demand for current-generation AI hardware while shifting investment toward alternative approaches. Technology transitions in AI could favor different companies and create winners and losers within current AI ETF portfolios.

Semiconductor technology risks include potential breakthroughs in quantum computing, optical processing, or neuromorphic chips that could displace current silicon-based AI accelerators. While such transitions typically occur over extended periods, the concentrated nature of AI ETF holdings amplifies exposure to technology disruption risks. Investment in emerging semiconductor technologies requires careful balance between current market leaders and potential disruptive innovators.

Geopolitical tensions create additional technology risks, particularly regarding U.S.-China competition in AI development and semiconductor manufacturing. Export controls on advanced semiconductor equipment and AI chips could disrupt global supply chains while creating both challenges and opportunities for different companies. AI ETFs with significant exposure to global supply chains face ongoing regulatory and trade policy uncertainties that could impact performance.

Regulatory and Policy Considerations

The growing importance of AI technology has attracted increased regulatory attention worldwide, creating potential policy risks that could impact AI ETF performance. European Union AI regulations, U.S. export controls, and emerging national security restrictions could affect AI technology development and deployment timelines. Regulatory compliance costs and operational restrictions may particularly impact smaller AI companies while providing advantages to larger, well-resourced organizations.

Data privacy regulations and AI governance frameworks are evolving rapidly across major markets, creating uncertainty about future operating requirements for AI companies. Companies with strong compliance capabilities and robust data governance practices may gain competitive advantages, while those struggling with regulatory requirements could face operational challenges. AI ETF managers must evaluate regulatory compliance capabilities as a key factor in security selection and portfolio construction.

Government AI policy initiatives, including research funding, infrastructure investments, and strategic partnerships, could significantly influence competitive dynamics within the AI sector. National AI strategies in the United States, China, and European Union include substantial government investments that could benefit different companies and technologies. AI ETF performance may increasingly reflect government policy decisions in addition to private market forces.

Future Outlook and Investment Implications

Long-Term Growth Projections

The AI infrastructure investment cycle appears positioned for sustained growth through the remainder of the decade, driven by continuous technology advancement and expanding enterprise adoption. Global AI spending is projected to reach $749 billion by 2028 with a five-year compound annual growth rate of 32.8%, indicating that current investment levels represent the early stages of a multi-year expansion. This growth trajectory suggests AI ETFs may continue outperforming broader market indices as AI infrastructure companies capture increasing shares of global technology spending.

The shift from AI model development to practical deployment and “Agentic AI” systems creates new investment opportunities across software platforms, edge computing, and specialized hardware categories. Microsoft’s $80 billion AI infrastructure investment and Apple’s focus on AI-enabled devices demonstrate the expansion of AI beyond data center applications into consumer and enterprise products. This broadening adoption creates more diverse investment opportunities within AI ETF portfolios while reducing concentration risks.

The emergence of edge AI and AI-enabled devices represents the next phase of AI infrastructure development, requiring different hardware architectures and software platforms than current data center-focused solutions. Companies developing specialized edge AI chips, efficient AI software frameworks, and distributed AI infrastructure may become increasingly important AI ETF holdings. The evolution from centralized to distributed AI processing creates new growth vectors for the AI ecosystem.

Investment Strategy Recommendations

Investors considering AI ETF exposure should carefully evaluate their risk tolerance, investment timeline, and portfolio diversification objectives before making allocation decisions. AI ETFs like BAI offer compelling growth potential but exhibit higher volatility than broader market indices, making them more suitable for investors with longer investment horizons and higher risk tolerance. Position sizing should reflect the concentrated and potentially volatile nature of AI technology investments.

Active versus passive AI ETF strategies present different risk-return trade-offs, with actively managed funds like BAI potentially offering superior performance during periods of rapid technological change but at higher expense ratios. Passive AI ETFs provide broader diversification and lower costs but may not adapt as quickly to evolving market conditions. Investors should evaluate management quality, expense ratios, and investment philosophy when selecting among AI ETF alternatives.

Geographic and sector diversification within AI investments can help manage concentration risks while maintaining exposure to AI growth trends. Combining pure-play AI ETFs with broader technology sector exposure may provide optimal risk-adjusted returns for many investors. Regular rebalancing and performance monitoring are essential given the rapid pace of change in AI markets and potential for significant performance divergence among different strategies.

Emerging Investment Themes

Several emerging themes within AI investing may create new opportunities and reshape existing AI ETF portfolios over the coming years. Artificial General Intelligence (AGI) development remains highly speculative but could create extraordinary value for companies achieving breakthrough capabilities. Investment in AGI research and development requires careful evaluation of technical feasibility and commercial viability timelines.

Sustainable AI and energy-efficient computing are becoming increasingly important as power consumption concerns limit AI deployment scale. Companies developing low-power AI chips, efficient cooling systems, and renewable energy solutions for data centers may gain competitive advantages as sustainability becomes a priority. Green AI investments align with environmental, social, and governance (ESG) investment criteria while addressing practical operational challenges.

AI democratization through cloud platforms and development tools creates opportunities in software-as-a-service and platform-as-a-service categories that complement hardware infrastructure investments. Companies providing accessible AI development platforms, pre-trained models, and specialized tools may benefit from broader AI adoption across industries and organizations. The expansion of AI beyond technology leaders creates new growth opportunities throughout the economy.

Conclusion: Navigating the AI Investment Revolution

The exceptional performance of AI ETFs in 2025, exemplified by BAI’s 36% surge, reflects the unprecedented scale and scope of the artificial intelligence infrastructure revolution transforming global technology markets. With AI spending projected to reach $500 billion by 2026 and hyperscaler capital expenditures exceeding $400 billion annually, the sector appears positioned for sustained growth that validates current premium valuations and performance expectations.

BAI’s active management approach and concentrated portfolio of leading AI infrastructure companies demonstrate the potential for skilled security selection to generate alpha during periods of rapid technological change. The fund’s strategic emphasis on semiconductor leaders like NVIDIA and Broadcom, combined with exposure to hyperscaler demand drivers, positions it to benefit from multiple AI growth vectors simultaneously. The fund’s 26.7% year-to-date outperformance relative to broader technology indices validates the premium paid for specialized AI investment expertise.

However, the concentrated nature of AI investments and elevated valuations require careful risk management and appropriate position sizing within diversified portfolios. The sustainability of current AI spending levels, potential technology disruptions, and evolving regulatory landscape create ongoing risks that investors must monitor closely. The winner-take-all dynamics emerging in AI infrastructure suggest that security selection and fund management quality will become increasingly important determinants of investment success.

For investors seeking exposure to the AI infrastructure revolution, BAI and similar actively managed AI ETFs offer compelling opportunities to participate in one of the most significant technology transformations in history. The combination of massive capital deployment, continuous innovation cycles, and expanding enterprise adoption creates favorable conditions for sustained outperformance, though investors must balance return potential against concentration risks and market volatility.

Looking ahead, the AI investment landscape will likely continue evolving as new technologies emerge, competitive dynamics shift, and regulatory frameworks develop. Success in AI investing will require not just identifying the right themes and companies, but also maintaining the flexibility to adapt as this transformative sector continues its rapid evolution throughout the remainder of the decade.

Ready to capitalize on the AI infrastructure revolution? Our specialized M&A advisory services help institutional investors and strategic acquirers identify prime opportunities in the rapidly evolving artificial intelligence ecosystem. From semiconductor consolidation to AI software platform acquisitions, we provide comprehensive market intelligence and transaction execution expertise. Contact us today to explore how the AI infrastructure boom creates compelling investment and M&A opportunities across the technology value chain.

Leave a Reply