The financial sector is experiencing a dramatic renaissance in 2025, with sector-focused exchange-traded funds reclaiming their position as top investor preferences after years of relative underperformance. Financial sector ETFs like XLF have delivered a solid 9.2% year-to-date return, positioning the sector as a compelling investment opportunity amid one of the most significant sector rotation cycles in recent memory. This resurgence stems from a perfect convergence of factors: record-breaking Q3 2025 banking earnings that exceeded expectations across all major institutions, a favorable Federal Reserve interest rate environment, and massive capital flows totaling over $50 billion rotating from growth sectors into cyclical value plays.

The transformation has been particularly pronounced in the wake of September’s Federal Reserve rate cut to 4.00-4.25%, which historically signals the beginning of outperformance cycles for financial institutions. Combined with investment banking revenues surging 40-80% year-over-year across major banks and trading revenues reaching record levels exceeding $35 billion quarterly across the sector, financial ETFs are capturing institutional attention as both a defensive play against economic uncertainty and a growth vehicle positioned to benefit from improving credit conditions and capital markets activity.

Record Q3 2025 Banking Earnings Drive Sector Momentum

Exceptional Performance Across All Major Institutions

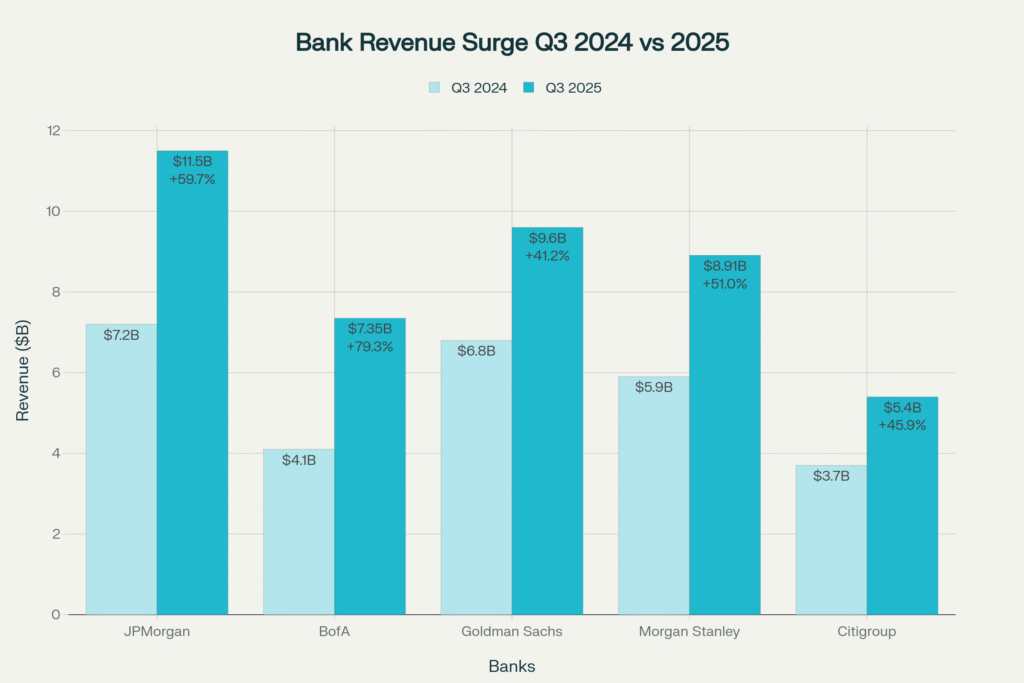

The third quarter of 2025 delivered a watershed moment for American banking, with every major financial institution significantly exceeding analyst expectations and posting results that validated the sector’s fundamental transformation. JPMorgan Chase reported record quarterly trading revenue of $8.9 billion, representing a 59.7% increase from Q3 2024 levels and demonstrating the bank’s ability to capitalize on market volatility and client activity. The bank’s earnings per share of $5.07 beat expectations by 4.75%, while comprehensive revenue reached $47.1 billion, reflecting broad-based strength across all business lines.

Bank of America delivered perhaps the most impressive performance, with investment banking revenue surging 43% year-over-year and net interest income reaching a record $15.4 billion. The bank’s strategic focus on wealth management and consumer banking proved prescient, generating $8.47 billion in quarterly net income that represented a 23% increase from the previous year. Morgan Stanley continued its strong performance trajectory, with equity trading revenue climbing 35% and total quarterly earnings growing 45% year-over-year to $4.61 billion.

The breadth of outperformance across the sector was remarkable, with Citigroup reporting adjusted earnings per share of $2.24 and 9% year-over-year revenue growth despite ongoing restructuring efforts. Even regional banks participated in the rally, with U.S. Bancorp beating expectations with EPS of $1.22 versus forecasts of $1.12, representing an 8.93% earnings surprise and 18.4% year-over-year growth. Overall, analysts expect third-quarter S&P 500 financials sector earnings to climb a healthy 11.5%, according to FactSet, significantly outpacing the broader market’s growth rate.

Investment Banking and Trading Revenue Renaissance

The dramatic surge in investment banking and trading revenues represents the most significant driver of financial sector outperformance, reflecting a fundamental shift in capital markets dynamics. Global M&A activity reached $1.26 trillion in Q3 2025, representing a 40% year-over-year increase and the second-best third quarter on record by value. This revival in dealmaking translated directly into fee income for major banks, with Goldman Sachs reporting a 42% surge in investment banking revenue and Morgan Stanley’s advisory fees reaching $684 million.

Trading desk performance reached historic levels as banks successfully navigated elevated market volatility and benefited from increased client activity. JPMorgan’s $8.9 billion in trading revenue included $5.6 billion from fixed income trading (up 21%) and $3.3 billion from equity trading (up 33%). The combined trading revenues across the four largest U.S. banks exceeded $35 billion for the quarter, representing the highest level since the financial crisis and demonstrating the sector’s evolution into sophisticated market-making operations.

The resurgence in IPO and capital markets activity has been particularly beneficial for investment banking divisions that had struggled during the 2022-2023 downturn. Banks are reporting robust pipelines extending into 2026, with private equity sponsors increasingly finding favorable exit environments and corporations pursuing strategic transactions that had been delayed during periods of uncertainty. This capital markets recovery is creating sustainable revenue streams that support higher valuations for financial sector ETFs and justify increased institutional allocation.

Federal Reserve Policy Creates Favorable Operating Environment

Historical Patterns Support Financial Sector Outperformance

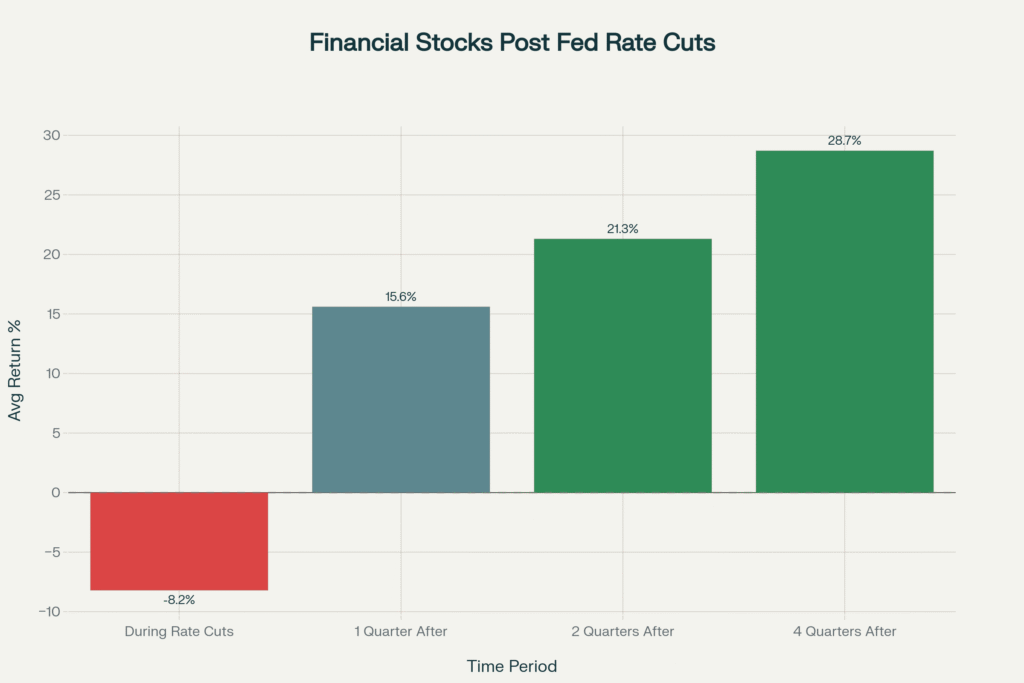

The Federal Reserve’s September 2025 rate cut to 4.00-4.25% represents the beginning of what market participants expect to be a measured easing cycle that historically benefits financial sector performance. Fed projections indicate additional cuts to 3.4% by end-2026 and 3.1% by end-2027, creating a predictable policy trajectory that enables strategic positioning by institutional investors. Historical analysis reveals that financial stocks typically underperform during the initial rate cutting phase but deliver exceptional returns in subsequent quarters.

During previous rate cutting cycles, financial sector stocks averaged -8.2% returns during the cutting phase but generated +15.6% returns one quarter after cuts began, +21.3% returns two quarters later, and +28.7% returns four quarters later. This pattern reflects the sector’s initial sensitivity to net interest margin compression followed by substantial benefits from improved loan demand, reduced credit costs, and enhanced economic activity. The current environment appears particularly favorable as banks enter the rate cutting cycle with strong capital positions, conservative credit standards, and diversified revenue streams that provide multiple avenues for growth.

The steeper yield curve environment created by Fed policy is already benefiting bank margins, with several institutions reporting improved net interest income guidance for upcoming quarters. Wells Fargo raised its full-year net interest income targets, while Bank of America increased its Q4 NII forecast to $15.6-15.7 billion, indicating confidence in the sustainability of current performance levels. This margin improvement, combined with expectations for increased loan demand as rates decline, creates a compelling fundamental backdrop for continued financial sector outperformance.

Credit Quality and Economic Resilience

Despite economic uncertainties, credit quality metrics across the banking sector remain remarkably strong, providing confidence in the sustainability of current earnings levels and the sector’s ability to navigate potential economic headwinds. Wells Fargo reported provisions for credit losses of just $681 million, significantly below the anticipated $1.17 billion, while Bank of America’s provision decreased by 13% to $1.3 billion. Net charge-off rates remain within historical norms, with JPMorgan’s Card Services net charge-off rate of 3.15% indicating manageable consumer credit stress.

The resilience of commercial credit quality has been particularly impressive, with most banks reporting minimal charge-offs in commercial and industrial lending portfolios. This performance reflects continued business cash flow strength and validates the enhanced underwriting standards implemented following previous credit cycles. Bank executives report early warning signs of economic softening but emphasize that the U.S. economy generally remains resilient, providing confidence that current credit quality trends will persist through the near-term economic transition.

Banks’ strong capital positions provide substantial buffers against potential economic disruptions, with all major institutions maintaining capital ratios well above regulatory requirements. This financial strength enables continued dividend payments and share repurchase programs that support total return performance for financial sector ETF investors. The combination of strong earnings growth and robust capital returns creates multiple sources of value creation that distinguish financial sector investments from other cyclical alternatives.

Sector Rotation Dynamics Favor Financial Exposure

Massive Capital Migration from Growth to Value

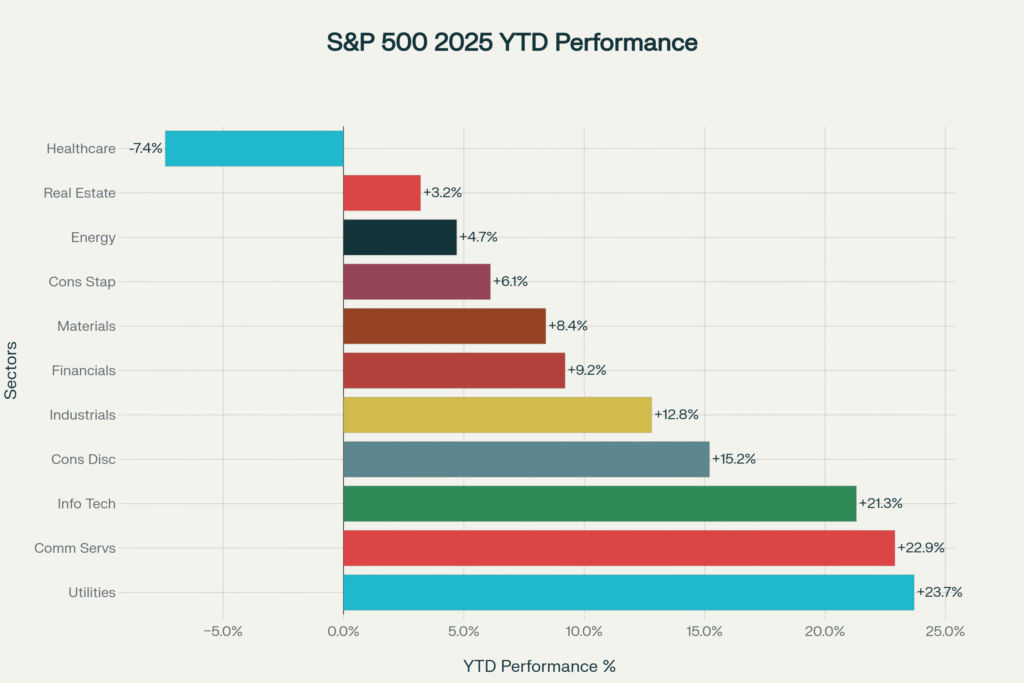

The 2025 investment landscape has been defined by one of the most significant sector rotation cycles in recent memory, with institutional capital systematically migrating from expensive growth sectors toward undervalued cyclical opportunities. Year-to-date, the Nasdaq (growth/Big Tech) is down more than 6%, while value stocks (Russell 1000 Value) are up 1.89% and financial sector ETFs have participated meaningfully in this rotation. The shift reflects institutional recognition that growth sector valuations had become unsustainable while traditional value sectors offered compelling risk-adjusted return opportunities.

Financial sector benefited disproportionately from this rotation, with $50+ billion in institutional capital flowing toward banks, insurance companies, and diversified financial services companies throughout 2025. European financial ETFs like EUFN have delivered exceptional 21% year-to-date returns, demonstrating that the rotation toward financials is a global phenomenon rather than a U.S.-specific trend. Sectors such as financial services, energy, and industrials have outperformed high-growth technology names, marking a dramatic change from the 2023-2024 environment where tech stocks dominated market leadership.

The breadth of this rotation has been remarkable, with 11 of 11 S&P 500 sectors ending 2024 in positive territory but only four beating the overall index. Communication Services surged +34.7% and Financials gained +30.6% in 2024, while even defensive Utilities enjoyed a +23.3% rebound. This broad-based performance created momentum that has continued into 2025, with financial sector ETFs positioned to benefit from continued institutional rebalancing as portfolio managers seek to reduce concentration risk in expensive growth sectors.

International and Emerging Market Dynamics

The sector rotation phenomenon extends beyond domestic U.S. markets, with international stocks (MSCI EAFE) up 11.21% year-to-date compared to significant underperformance by growth-oriented indices. This global rotation reflects common themes including currency adjustments, relative valuation considerations, and institutional recognition that economic growth is becoming more broad-based rather than concentrated in a handful of technology leaders.

Emerging market financial institutions have participated in this rotation, though with more mixed results due to tariff pressures and weak domestic demand in some regions. Eurozone banks have benefited from robust corporate earnings, while Asian financial institutions have shown resilience despite geopolitical tensions. The global nature of financial sector strength supports the investment thesis for broadly diversified financial sector ETFs that provide exposure to international banking systems and currency diversification benefits.

The rotation away from U.S. dollar strength has particularly benefited international financial sector exposure, with weaker dollar conditions improving competitiveness for foreign banks and reducing funding pressures for emerging market institutions. This international dimension adds depth to the financial sector investment thesis, suggesting that geographic diversification within financial sector ETFs could provide additional sources of alpha and risk reduction.

ETF Flow Dynamics and Institutional Positioning

Record ETF Inflows Signal Sustained Institutional Interest

The 2025 ETF market has experienced unprecedented growth, with U.S. ETF inflows crossing $1 trillion at record pace and total assets reaching $12.7 trillion by September. Q3 2025 marked the strongest quarter yet with $377 billion in inflows, representing 43% more than Q2 and double the quarterly average since 2020. Financial sector ETFs have been significant beneficiaries of these flows as institutional investors seek exposure to the sector’s improving fundamentals and attractive valuations.

The shift toward active ETF management has particularly benefited financial sector funds, with 97% of investors planning to increase their active ETF exposures over the next 12 months. Active financial sector ETFs provide professional management that can navigate the complex dynamics of bank earnings cycles, regulatory changes, and interest rate sensitivity that characterize the sector. This trend toward active management reflects institutional recognition that financial sector investing requires specialized expertise and dynamic allocation adjustments.

Geographic diversification within ETF flows has also supported financial sector performance, with international investors beginning to rotate back to U.S. exposures. Fixed income ETFs set a new record in Q3 with active fixed income ETFs accounting for 44% of flows, indicating institutional preference for professional management during periods of monetary policy transition. This institutional migration toward professionally managed strategies creates sustained demand for well-managed financial sector ETFs with experienced investment teams.

Fundamental Factors Supporting Continued Inflows

Several fundamental factors support continued institutional flows into financial sector ETFs. The sector’s attractive dividend yields averaging 2-3% provide income generation that complements growth potential, particularly valuable in an environment where cash yields are declining due to Fed rate cuts. XLF’s dividend yield of 1.38% combined with capital appreciation potential offers compelling total return characteristics compared to fixed income alternatives.

Valuation metrics remain attractive relative to both historical levels and other sectors, with financial sector trading at reasonable forward price-to-earnings ratios despite strong recent performance. The sector’s beta of approximately 1.05 versus the S&P 500 provides modest amplification of market movements while maintaining reasonable volatility characteristics. This risk-return profile appeals to institutional investors seeking cyclical exposure without excessive volatility.

The liquidity characteristics of major financial sector ETFs continue to attract institutional attention, with XLF averaging over 35 million shares in daily volume and tight spreads of 0.01-0.02 USD. This exceptional liquidity enables large institutional transactions without market impact concerns and supports sophisticated trading strategies including options overlays and portfolio hedging applications. The combination of fundamental strength and technical liquidity creates sustainable institutional demand for financial sector ETF exposure.

Investment Implications and Strategic Positioning

Portfolio Allocation Strategies in Current Environment

Financial sector ETFs have emerged as core holdings for institutional portfolios seeking to balance growth potential with defensive characteristics in an uncertain economic environment. The sector’s performance during the initial phases of Fed rate cutting cycles provides downside protection while positioning for potential upside as economic conditions improve. Recommended allocation ranges of 5-15% of equity portfolios enable meaningful participation in sector themes while maintaining appropriate diversification across economic sectors.

Tactical allocation strategies can enhance returns by utilizing the predictable patterns of financial sector performance around earnings seasons and Fed policy announcements. The concentration of major bank earnings in the first two weeks of each quarter creates recurring opportunities for tactical over-weighting ahead of results that typically exceed expectations. Fed meeting calendars and economic data releases provide additional timing signals for adjusting financial sector exposure within broader portfolio contexts.

International diversification within financial sector allocations adds strategic value by reducing concentration risk in U.S. banking system performance while providing currency hedging benefits. European financial ETFs like EUFN offer exposure to different regulatory environments and economic cycles that may provide uncorrelated returns relative to U.S. financial performance. Emerging market financial sector exposure adds additional diversification while potentially capturing higher growth rates in developing banking systems.

Risk Management and Position Sizing Considerations

Despite strong fundamental momentum, financial sector investments require careful risk management due to the sector’s sensitivity to interest rate changes, regulatory developments, and economic cycles. Position sizing should reflect individual risk tolerance and overall portfolio construction, with larger allocations appropriate for investors with longer time horizons and higher risk tolerance. The sector’s historical volatility patterns suggest that tactical position adjustments may be more effective than static buy-and-hold approaches.

Regulatory risk remains a persistent consideration for financial sector investments, particularly given the sector’s systemic importance and ongoing regulatory evolution. Banking regulations, capital requirements, and compliance costs can materially impact sector profitability and should be monitored closely by investors. Political developments and policy changes also influence financial sector performance through their effects on regulations, tax policies, and economic growth prospects.

Interest rate sensitivity requires ongoing monitoring as Fed policy evolves and economic conditions change. While current rate cutting cycles historically benefit financial sector performance, the magnitude and timing of policy changes can create short-term volatility. Diversification across different types of financial institutions (money center banks, regional banks, insurance companies, payment processors) can reduce exposure to specific regulatory or business model risks while maintaining sector exposure.

Future Outlook and Catalysts

The financial sector outlook for the remainder of 2025 and into 2026 appears constructive based on current fundamental trends and policy trajectories. Continued Fed rate cuts should support loan demand growth while the current elevated rate levels maintain favorable net interest margins during the transition period. Investment banking pipelines remain robust with continued M&A activity and capital raising supporting fee income growth across major institutions.

Technological advancement within financial services represents an additional growth catalyst, with banks increasingly benefiting from AI applications, digital transformation, and operational efficiency improvements. These technological investments should support margin expansion and competitive positioning while creating new revenue opportunities in emerging financial services segments. Fintech partnerships and acquisitions provide additional avenues for growth and innovation within traditional banking frameworks.

Credit normalization represents both opportunity and risk as economic conditions evolve and previous monetary tightening effects work through the system. Current strong credit quality provides cushion for potential deterioration, while normalized credit costs should support more predictable earnings patterns compared to the artificially low credit costs of recent years. Geographic and sector diversification within lending portfolios should help major banks navigate changing credit conditions while supporting continued growth in loan balances.

Conclusion: Financial Sector ETFs as Core Portfolio Holdings

The financial sector’s remarkable transformation in 2025 represents far more than a cyclical rebound—it reflects fundamental improvements in business model resilience, regulatory positioning, and competitive dynamics that support sustained outperformance potential. The convergence of record Q3 earnings performance, favorable Federal Reserve policy, and massive sector rotation dynamics has created compelling investment opportunities that extend well beyond short-term tactical positioning.

Financial sector ETFs like XLF offer institutional investors professionally managed exposure to diversified banking, insurance, and financial services companies with attractive risk-adjusted return characteristics. The sector’s 9.2% year-to-date performance, strong dividend yields, and improving fundamental metrics position these funds as core holdings rather than speculative sector bets. Historical patterns following Fed rate cutting cycles suggest that current positioning may capture the early stages of multi-quarter outperformance cycles.

The breadth of financial sector strength across investment banking, trading, credit quality, and international markets indicates that current performance reflects sustainable improvements rather than temporary cyclical factors. Record ETF inflows exceeding $1 trillion annually and continued institutional adoption of active management strategies provide sustained demand dynamics that should support continued performance. For investors seeking exposure to economic growth, interest rate normalization, and sector rotation themes, financial sector ETFs represent compelling opportunities to participate in one of 2025’s most significant investment trends.

Looking ahead, the combination of supportive monetary policy, robust earnings momentum, and attractive valuations creates favorable conditions for continued financial sector leadership. While risks remain around regulatory changes, credit cycles, and economic transitions, the sector’s demonstrated resilience and diversified revenue streams provide confidence in its ability to navigate changing conditions while delivering superior risk-adjusted returns for patient investors.

Ready to capitalize on the financial sector renaissance? Our specialized M&A advisory services help institutional investors and strategic acquirers identify prime opportunities in the evolving financial services landscape. From fintech consolidation to traditional banking M&A, we provide comprehensive market intelligence and transaction execution expertise. Contact us today to explore how the financial sector transformation creates compelling investment and acquisition opportunities in both public and private markets.

Leave a Reply