City of London’s Broker Shakeout Puts a Spotlight on Peel Hunt: The Last Stand of UK Independence

Twenty years ago, choosing a corporate broker ranked among the most crucial decisions for any company preparing to join the London Stock Exchange. The City boasted a vibrant ecosystem of independent advisory firms—names like Cazenove, Hoare Govett, Collins Stewart, Numis, and Panmure Gordon—that provided conflict-free counsel, deep UK market expertise, and bespoke attention to mid-cap and growth companies navigating public markets.

Today, that landscape has been devastated by waves of consolidation driven by brutal market conditions: an IPO drought, the hollowing out of UK public markets, regulatory cost pressures from MiFID II’s research unbundling, and the steady exodus of companies delisting or moving to overseas exchanges. Most of the capital’s storied independent brokers have been swept away by takeovers or forced mergers, leaving Peel Hunt conspicuously isolated as the last major independent name still standing.

This positioning creates a paradox for Peel Hunt: its independence represents both its greatest competitive advantage and its most significant vulnerability. As the UK takeover market surges to levels not seen since 2021—with £74 billion in bids during just the first half of 2025 and an anticipated £150 billion annual run rate—Peel Hunt finds itself advising on this M&A frenzy while potentially becoming the next target itself.

The Consolidation Wave That Reshaped the City

From Abundance to Scarcity: The Disappearing Independents

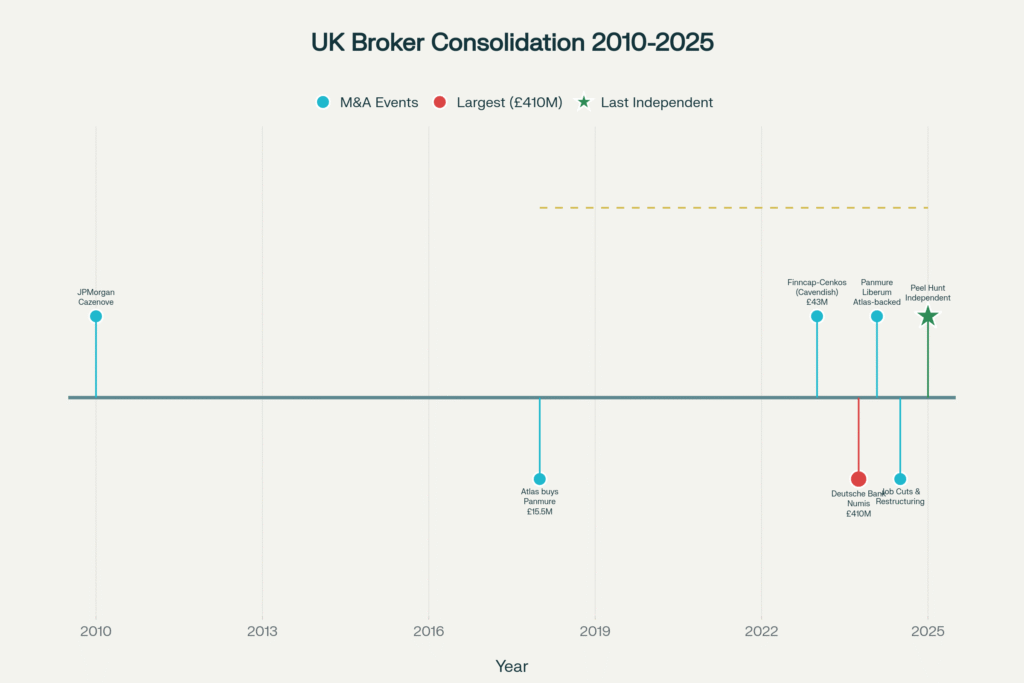

The transformation of London’s corporate broking landscape has been swift and unforgiving. The 2008 financial crisis initiated the first wave of consolidation, culminating in JPMorgan Chase’s acquisition of the 185-year-old Cazenove & Co. in 2010—a deal that symbolized the end of an era for British financial independence. What had been the preeminent City institution serving blue-chip British companies became subsumed into an American banking giant.

The pace of consolidation accelerated dramatically in recent years as structural headwinds intensified. In October 2023, Deutsche Bank completed its £410 million acquisition of Numis, the largest institutional broker consolidation deal and a transaction that shocked the market with both its price tag and strategic implications. The creation of Deutsche Numis brought 300+ corporate clients under the control of a German bank, further reducing domestic UK ownership of critical financial infrastructure.

Just months later in January 2024, Panmure Gordon—backed by former Barclays executives Bob Diamond and Rich Ricci through Atlas Merchant Capital—merged with Liberum in an all-share transaction designed to create what the firms proclaimed would be “the UK’s largest independent investment bank.” The combined Panmure Liberum entity brought together 250+ corporate clients and claimed market-making capabilities across 750+ stocks.

Yet this “independence” came with caveats: Atlas Merchant Capital’s majority ownership and the appointment of Barclays veterans to leadership roles raised questions about how genuinely independent the entity remained. Moreover, Panmure Liberum has struggled financially, with the pre-merger Panmure Gordon posting a £7.2 million loss in 2023 and subsequently implementing job cuts affecting approximately 20 positions in mid-2024 as integration challenges mounted.

The Structural Forces Driving Consolidation

The broker consolidation wave reflects deep structural challenges afflicting UK equity capital markets that extend far beyond cyclical market downturns. The number of companies listed on the London Stock Exchange has declined precipitously, with more firms leaving through takeovers, delistings, or migrations to U.S. exchanges than arriving through new IPOs.

Initial public offering activity collapsed to historically low levels throughout 2023-2024, depriving brokers of their most lucrative revenue source. Peel Hunt itself acknowledged that “historically low levels of equity capital markets activity” created “subdued conditions” that resulted in a £3.5 million pre-tax loss for the year ending March 2025, despite revenues increasing 6% to £91.3 million.

The MiFID II unbundling requirements, which forced asset managers to separate payments for research from execution commissions, devastated broker economics by making previously bundled research services explicit line items subject to cost scrutiny. This regulatory shift disproportionately impacted mid-sized brokers whose business models depended on cross-subsidizing research through trading revenues.

Adding to these pressures, many UK-listed companies—disappointed with persistently depressed valuations and thin trading liquidity—have explored or executed strategic alternatives including going private or pursuing listings in deeper, more liquid markets like New York. This exodus further reduced the addressable market for UK-focused brokers, creating a vicious cycle of declining revenues, cost-cutting, and ultimately consolidation.

Peel Hunt: The Last Major Independent Standing

Financial Performance Amid Adversity

Despite the challenging environment, Peel Hunt has demonstrated remarkable resilience while maintaining its independence—a feat that distinguishes it from virtually every comparable broker. The firm’s financial trajectory tells a story of strategic adaptation during one of the most difficult periods in UK capital markets history.

For the financial year ending March 2025, Peel Hunt reported revenues of £91.3 million, representing a 6% year-over-year increase despite market headwinds. However, the firm remained in the red with a pre-tax loss of £3.5 million, marginally wider than the £3.3 million loss reported the previous year. These results reflected conscious strategic investments in junior talent and capability building even as market conditions deteriorated.

The narrative shifted dramatically in September 2025 when Peel Hunt announced it was “on track to beat its financial targets for the year after a strong start to trading.” The firm’s shares surged 6.9% to reach 108.5p—their highest level of the year—as management revealed “emerging activity” in equity capital markets and successful involvement in several significant M&A transactions.

Perhaps most significantly, Peel Hunt disclosed it was now collaborating with 58 clients from the FTSE 350 index, up from 55 in the previous quarter, demonstrating franchise expansion during a period when competitors were retrenching. Analyst Edward Frith at KBW noted that despite “challenging” conditions for UK equity capital markets over three years, Peel Hunt had achieved “two years of growth in both revenue and franchise,” with 2026 appearing on track to continue this trend and deliver “a return to profitability”.

Strategic Positioning and Competitive Differentiation

Peel Hunt’s independence provides tangible competitive advantages that have proven increasingly valuable as consolidation has reduced client choice. As an independent broker without proprietary trading operations or investment banking conflicts of interest, Peel Hunt can offer genuinely conflict-free advice—a proposition that resonates strongly with boards and management teams navigating complex strategic decisions.

The firm’s specialization in mid-cap and growth companies positions it squarely in the segment experiencing the most intense M&A activity. With 76% of all UK takeover offers in H1 2025 valued under £500 million, Peel Hunt’s sweet spot aligns precisely with where deal flow has concentrated. This positioning proved valuable in high-profile transactions including advising on Canal+’s London IPO in December 2024—hailed as the most successful European listing of the year—and completing what Peel Hunt described as its “largest M&A transaction to date”.

The firm’s research capabilities provide another differentiation point. With independent research perspectives increasingly valued by institutional investors seeking alternatives to bulge bracket consensus views, Peel Hunt’s analytical franchise serves both as a revenue generator and a relationship anchor with the buy-side community.

Moreover, Peel Hunt benefits from what might be termed “last mover advantage” in the consolidation cycle. As one of the few remaining independent options, the firm can attract clients and talent dissatisfied with integration disruptions, culture changes, or service quality deterioration at recently consolidated competitors.

The UK Takeover Surge: Barbarians at the Gate

Record Activity Levels and Market Dynamics

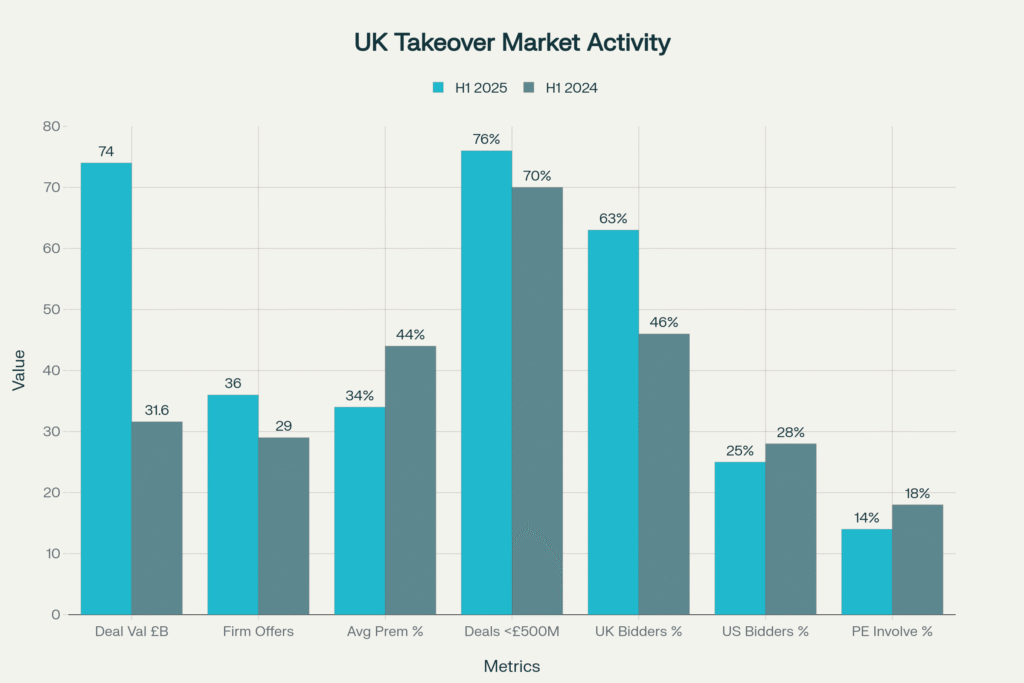

The irony of Peel Hunt’s situation is that the firm finds itself advising on a historic surge in UK takeover activity while its own independence potentially makes it an attractive target. The first half of 2025 witnessed £74 billion in announced bids for British companies—the highest level since 2021 and positioning 2025 to potentially become “the most intense period of UK takeovers in recent years”.

Peel Hunt’s own M&A analysis, published in reports titled “Barbarians At The Gate” and highlighting “UK Takeover Trends,” reveals alarming statistics for the health of UK public markets. During H1 2025, 36 firm offers were announced, up from 29 in H1 2024, with activity accelerating to roughly two new bid situations per week.

The composition of bidders reveals important trends. UK-listed consolidators represented 63% of bidders during H1 2025—well above the 46% five-year average—reflecting what Peel Hunt’s Michael Nicholson called “the return of the UK-listed consolidator” who has proven capable of competing with foreign acquirers. Meanwhile, U.S. firms accounted for over 25% of bidders, with private equity involvement remaining robust at 14% of all bid situations.

Critically, average bid premiums have compressed to 34% in 2025 from 44% in 2024 and 56% in 2023, suggesting that valuation gaps between public market prices and private transaction values are narrowing—though still substantial enough to motivate deal activity. This premium compression indicates either that UK valuations are recovering or that acquirers are becoming more disciplined in their pricing, potentially both.

The AIM Vulnerability and Small-Cap Crisis

Peel Hunt’s analysis identified particularly acute risks for companies listed on the Alternative Investment Market (AIM), London’s junior exchange. The broker warned that approximately one-third of AIM-listed companies with market capitalizations between £50 million and £250 million are “potentially vulnerable to acquisition” in 2025.

This vulnerability stems from severe price dislocations: 32% of AIM companies in this size range experienced share price declines exceeding 30% over the twelve months ending mid-2025, making them mathematically attractive for opportunistic buyers who can offer meaningful premiums while still achieving compelling returns.

Michael Nicholson, Peel Hunt’s head of advisory and M&A, warned bluntly: “We observe a wave of demand approaching the shores of the UK—with strategic and private equity buyers simultaneously active—and our coastal defences feel weaker than ever.” He added that “one in 20 of all UK-listed companies” received public takeover offers in 2024, “the highest level we have observed in recent years”.

The combination of depressed valuations, limited access to capital for growth financing, thin trading liquidity, and ongoing investor disinterest in UK small-caps has created what Peel Hunt describes as a perfect storm making British companies significantly more attractive to acquirers than to public market investors. As the broker noted in its analysis: “Companies in the UK seem to be far more attractive to acquirers than investors”.

The Independence Premium and Takeover Speculation

Why Peel Hunt Matters to UK Markets

Peel Hunt’s continued independence carries significance beyond the firm’s own interests. For UK small and mid-cap companies, the availability of a genuinely independent advisor provides crucial optionality when navigating strategic alternatives, defensive situations, or capital raising requirements.

The concentration of UK corporate broking into either foreign-owned banks (Deutsche Numis, JPMorgan Cazenove) or recently consolidated entities backed by private equity (Panmure Liberum, Cavendish) creates potential conflicts and service quality concerns. Deutsche Bank’s ownership of Numis means corporate clients must consider whether German parent priorities might influence advice, while Atlas Merchant Capital’s control of Panmure Liberum introduces private equity ownership dynamics that may prioritize exit timing over long-term client relationships.

For institutional investors, Peel Hunt’s independent research provides perspectives unencumbered by investment banking relationships or proprietary trading positions. As MiFID II pressures continue squeezing research budgets across the buy-side, the value of differentiated, conflict-free insights has increased rather than diminished.

From a UK financial services policy perspective, Peel Hunt represents one of the last vestiges of domestically-owned financial infrastructure serving the mid-cap economy. The progressive foreign acquisition of British brokers, while individually defensible on commercial grounds, collectively raises questions about whether the UK retains adequate domestic capacity to serve its own capital markets.

Takeover Vulnerability and Potential Suitors

Peel Hunt’s positioning as the last major independent makes it an inherently attractive strategic asset for multiple categories of potential acquirers, though the firm has given no indication it seeks a transaction.

Foreign banks seeking to establish or expand UK mid-cap capabilities could view Peel Hunt as a turnkey solution. With approximately 250 corporate clients and 58 FTSE 350 relationships, an acquirer would immediately gain material market share and client relationships that typically require years to develop organically. U.S. bulge brackets like Jefferies, European banks like BNP Paribas, or even Canadian institutions could find strategic logic in acquiring UK capabilities through Peel Hunt.

Private equity buyers, following the playbook established by Atlas Merchant Capital with Panmure Gordon, might see Peel Hunt as an operational turnaround opportunity. With the firm approaching profitability after several restructuring years and positioned to benefit from any UK ECM recovery, a PE buyer could potentially acquire at a reasonable multiple, support growth investments, and exit at higher valuations if market conditions normalize.

Strategic consolidators among existing brokers could view Peel Hunt as an opportunity to achieve scale benefits. While Panmure Liberum recently consolidated, further industry consolidation remains possible if a buyer believed combining client relationships, reducing overhead through integration, and eliminating competitive overlap could justify acquisition premiums.

The challenge for any potential acquirer lies in Peel Hunt’s culture and client relationships, which derive significant value from the firm’s independence. As with many professional services acquisitions, integration risks include key employee departures, client defections, and culture clashes that can rapidly destroy the value being acquired.

Market Structure Implications and Future Outlook

The Hollowing of UK Financial Services

The progressive consolidation of City brokers forms part of a broader pattern of foreign acquisition and domestic hollowing affecting UK financial services. Beyond corporate broking, similar dynamics have played out in asset management, insurance, and other segments where British institutions have been acquired by larger international competitors.

This trend carries economic and strategic implications. Financial and professional services generate UK exports exceeding double those of any other sector, support 2.5 million jobs (mostly outside London), and contribute nearly £110 billion in annual tax revenue. The industry’s health matters not just to the City but to the entire UK economy.

The loss of independent UK brokers specifically impacts the small and mid-cap economy that forms “the lifeblood of the UK economy,” as Bob Diamond noted when justifying the Panmure-Liberum merger. If these companies lack access to high-quality, conflict-free advice from institutions that understand UK market dynamics, their ability to access capital, execute strategic transactions, or defend against opportunistic takeovers may be compromised.

Regulatory and Policy Responses

UK regulators and policymakers have begun recognizing these structural challenges, though effective policy responses remain elusive. The Competition and Markets Authority (CMA) has signaled a more growth-oriented approach under new leadership, with the government issuing a “strategic steer” emphasizing that CMA actions should “reflect the need to enhance the attractiveness of the UK as a destination for international investment”.

The Financial Conduct Authority (FCA) implemented radical changes to listing rules in July 2024, creating a simpler, more flexible framework designed to make UK listings more attractive. These reforms removed requirements for shareholder approval of significant transactions and introduced private sale processes to give target companies more control over takeover situations.

However, these regulatory adjustments have yet to reverse the fundamental outflow of capital from UK markets or restore IPO activity to healthy levels. As Peel Hunt itself noted, addressing the core problem requires ensuring that “UK capital backs UK companies”—a cultural and economic challenge that transcends regulatory fixes.

The Path Forward for Peel Hunt

Peel Hunt’s strategy centers on maintaining independence while building the scale and capabilities needed to remain competitive as markets evolve. The firm’s September 2025 trading update emphasized diversification beyond pure ECM activities into M&A advisory, where deal flow has proven more resilient.

Expanding the FTSE 350 client roster from 55 to 58 during challenging market conditions demonstrates the firm’s ability to win mandates even against larger competitors. If Peel Hunt can sustain this franchise expansion while controlling costs and returning to sustainable profitability in FY2026, it strengthens the case for continued independence.

The firm benefits from operating in a segment—UK small and mid-caps—where demand for advisory services remains robust even as public market activity has slowed. With 33% of AIM companies potentially vulnerable to takeover, Peel Hunt’s defensive advisory capabilities should generate consistent mandates.

However, the firm faces genuine challenges to its independence thesis. If UK public markets continue deteriorating—through further delistings, takeover activity, or migration of companies to foreign exchanges—Peel Hunt’s addressable market shrinks accordingly. The broker’s business model depends on a vibrant UK mid-cap public market that, at present, appears structurally challenged.

Conclusion: The Last Independent’s Dilemma

Peel Hunt’s position as the City of London’s last major independent corporate broker represents both the culmination of a brutal consolidation wave and a potential last stand for UK-owned financial infrastructure serving the mid-cap economy. The firm has survived where storied competitors fell, maintained franchise growth during market downturns, and positioned itself to benefit from any recovery in UK equity capital markets.

Yet this very survival makes Peel Hunt increasingly conspicuous as a potential takeover target. Its independence—the source of competitive advantage with clients seeking conflict-free advice—simultaneously makes it an attractive strategic asset for acquirers seeking instant UK market share and capabilities. The delicate balance between maintaining independence and potentially succumbing to the same consolidation forces that eliminated competitors defines Peel Hunt’s strategic challenge.

For UK capital markets more broadly, Peel Hunt’s fate carries symbolic weight beyond the firm’s individual circumstances. If the last major independent broker ultimately succumbs to foreign acquisition or forced consolidation, it would mark another step in the progressive hollowing of domestically-owned financial infrastructure serving British businesses. The questions this raises about the UK’s ability to maintain vibrant, competitive capital markets that serve the real economy extend well beyond corporate broking to the heart of Britain’s post-Brexit economic model.

The coming months will reveal whether Peel Hunt can sustain its independence, potentially becoming a case study in resilience, or whether the structural forces reshaping City financial services ultimately prove too powerful even for the sector’s last major independent to withstand. For now, Peel Hunt stands alone—both vulnerable and valuable—as the final significant holdout in a landscape transformed by consolidation.

Ready to Explore Your Next Deal?

Our team specializes in M&A advisory, deal sourcing, capital introductions, and strategic positioning in private markets. Whether you’re raising capital, seeking acquisition opportunities, or planning an exit, we provide the expertise and network to execute successfully.

Book a Strategy Call

Leave a Reply