The Reserve Bank of India (RBI) made a decisive statement in October 2025 by maintaining its repo rate at 5.5% for the second consecutive meeting, signaling a strategic pause after delivering 100 basis points of aggressive rate cuts earlier this year. This decision, announced by Governor Sanjay Malhotra following the Monetary Policy Committee’s three-day deliberation, carries profound implications for millions of Indian borrowers whose loan EMIs remain directly linked to the central bank’s policy rates.

The decision to hold rates steady comes against a backdrop of remarkable economic stability, with inflation projections revised sharply downward to 2.6% for FY26—well below the RBI’s comfort zone—while GDP growth forecasts have been upgraded to a robust 6.8%. For borrowers across home loans, personal loans, and vehicle financing, this translates to continued stability in EMI outflows, though the broader narrative suggests potential opportunities ahead as the central bank maintains its accommodative stance while keeping “powder dry” for future economic support.

The implications extend far beyond static EMI calculations. With inflation now tracking at a 99-month low and the RBI hinting at future policy space, borrowers find themselves at a unique juncture where current stability meets future opportunity in India’s evolving interest rate landscape.

Decoding the RBI’s Strategic Pause

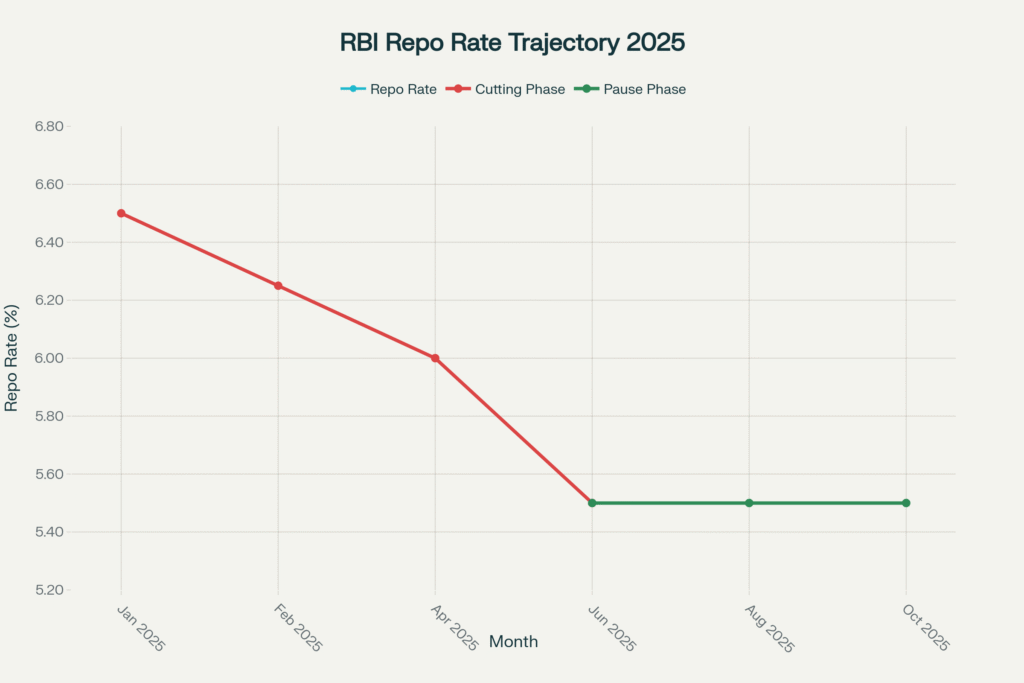

The Journey from 6.5% to 5.5%: A Year of Decisive Action

The October decision represents the culmination of an extraordinary year of monetary policy activism by the RBI. Starting from 6.5% in January 2025, the central bank embarked on an aggressive easing cycle that delivered 100 basis points of cuts across three tranches: 25 basis points each in February and April, followed by a surprising 50 basis point jumbo cut in June that caught markets off-guard.

This monetary accommodation was driven by rapidly cooling inflation pressures, with Consumer Price Index (CPI) inflation declining from elevated levels to reach an eight-year low of 1.54% in September 2025. The sustained disinflationary trend, supported by favorable monsoons, declining food prices, and GST rationalization measures, provided the RBI with unprecedented policy space to support economic growth.

The pause since June reflects the central bank’s measured approach to policy transmission. With commercial banks having absorbed approximately 70-80% of the cumulative rate cuts, the RBI has chosen to allow full transmission of previous measures while assessing their economic impact before charting the next course of action.

Inflation Outlook: The Benign Trajectory

The RBI’s confidence in maintaining policy rates stems from a fundamentally transformed inflation landscape. The central bank has revised its average inflation projection for FY26 to 2.6%, down dramatically from the 3.1% forecast in August and the 3.7% projection in June. This downward trajectory reflects both favorable base effects and structural improvements in supply chain dynamics.

Food inflation, which comprises nearly 46% of the CPI basket, has experienced an unprecedented 11-month consecutive decline through September 2025—the longest such streak in the current CPI series. Vegetable prices have declined 21.38% year-on-year, while broader food categories have shown sustained moderation, creating a disinflationary impulse that has surprised even seasoned analysts.

The GST rationalization implemented in September 2025 has provided additional disinflationary support, directly impacting 11.4% of the CPI basket and helping to lower consumer prices across essential goods and services. This policy initiative, combined with improved agricultural supply conditions, has created a benign inflation environment that provides substantial room for accommodative monetary policy.

Impact on Your Loan EMIs: Current Status and Future Prospects

Home Loans: Stability with Underlying Opportunity

For the millions of Indians with home loans linked to external benchmarks—primarily the repo rate—the October decision means immediate EMI stability. Since October 2019, floating-rate retail loans have been mandatorily linked to external benchmarks, ensuring direct transmission of policy rate changes to borrower interest costs.

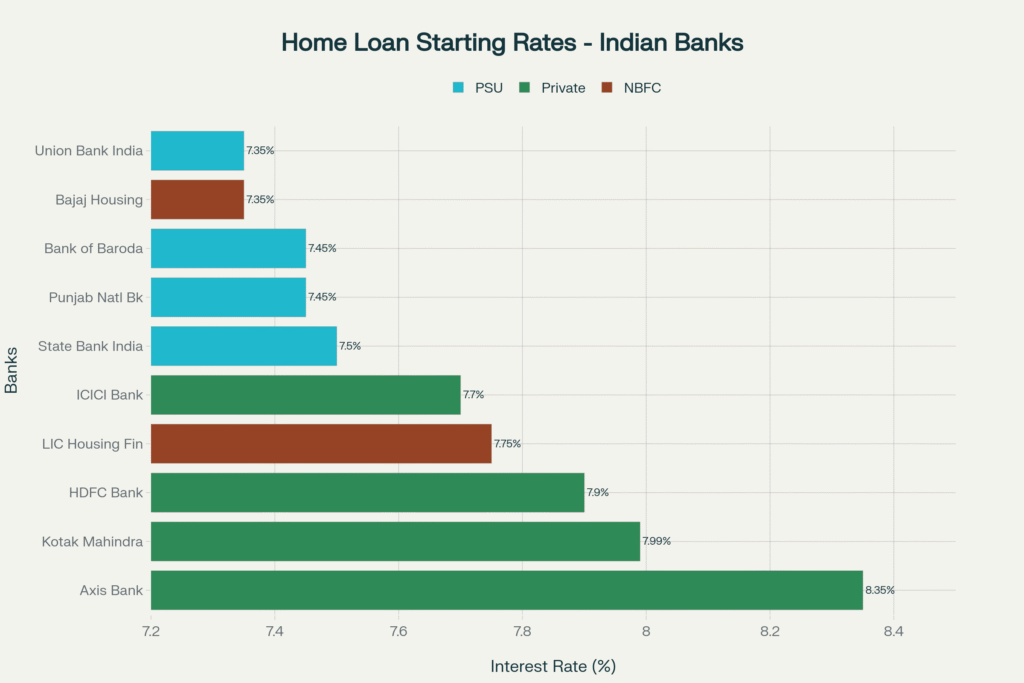

Current home loan rates across the banking system reflect the beneficial impact of the year’s rate cuts, with offerings ranging from 7.35% at select public sector banks like Union Bank of India to 8.35% at private sector institutions. The differential reflects varying risk assessments, customer profiles, and institutional funding costs, but represents a significant improvement from the 8.50-9.00% rates prevalent at the start of 2024.

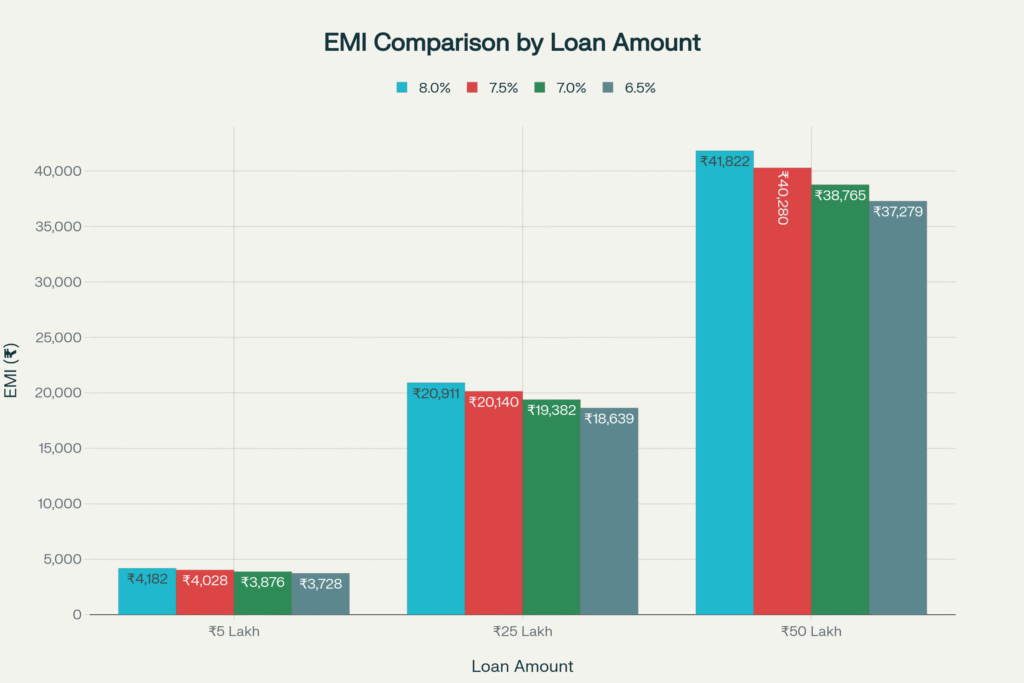

For a typical ₹25 lakh home loan over 20 years, the difference between current rates and potential future cuts is substantial. At today’s average rate of 8.0%, the EMI stands at ₹20,911. Should rates decline to 7.5% following future RBI action, the EMI would reduce to ₹20,140, creating monthly savings of ₹771 and total interest savings exceeding ₹1.85 lakh over the loan tenure.

Personal Loans and Vehicle Financing: Mixed Transmission Patterns

Personal loan rates show more complex transmission patterns, with institutions offering rates ranging from 9.99% for prime borrowers to 18-22% for standard profiles. The variability reflects the unsecured nature of personal loans and the diverse risk profiles of borrowers, though the underlying cost of funds reduction has provided some relief across the spectrum.

Vehicle financing has benefited more directly from the repo rate cuts, with new car loan rates starting from 7.80% at select banks and reaching up to 9.45% depending on the vehicle segment and borrower profile. Used car financing remains more expensive, typically ranging from 11.25% to 14.75%, reflecting higher risk premiums and shorter asset lifecycles.

The transmission lag in personal and vehicle loans reflects the MCLR (Marginal Cost of funds based Lending Rate) linkage for many existing contracts, which resets at longer intervals compared to repo-linked products. Borrowers with older loans may benefit from switching to newer repo-linked products to capture immediate rate advantages.

Business and Commercial Lending: Gradual Benefits

Business loan rates demonstrate the most complex transmission dynamics, with institutional lenders offering rates from 11.50% to 26.00% depending on business size, sector, and credit profile. Small and Medium Enterprise (SME) lending has seen some moderation, though the high-risk perception of this segment limits the pass-through of policy rate benefits.

Commercial real estate and infrastructure financing have benefited more substantially, with institutional rates declining in line with broader funding cost improvements. However, the lending criteria remain stringent, requiring strong cash flows and robust collateral to access the most favorable rates.

Bank-Wise Rate Comparison: Finding the Best Deal

Public Sector Leadership in Competitive Pricing

Public sector banks continue to lead the competitive landscape in home loan pricing, with Union Bank of India and Bajaj Housing Finance offering starting rates of 7.35%, followed closely by Bank of Baroda and Punjab National Bank at 7.45%. State Bank of India, the country’s largest lender, provides rates starting at 7.50%, representing excellent value for most borrowers.

The pricing advantage of public sector institutions reflects their lower funding costs, government support, and strategic mandate to support homeownership. However, borrowers must balance rate advantages against processing speed and service quality, where private sector banks often excel.

Private sector banks, while typically pricing higher, offer competitive rates for high-value customers and provide superior digital experiences. HDFC Bank starts at 7.90%, ICICI Bank at 7.70%, and Kotak Mahindra Bank at 7.99%, with the final rate depending significantly on customer relationship depth and credit profile.

Processing Fees and Hidden Costs

Beyond interest rates, borrowers must evaluate total cost structures including processing fees, which vary significantly across institutions. Several public sector banks, including Punjab National Bank and Union Bank of India, offer zero processing fees, while private banks typically charge 0.25-0.50% of the loan amount subject to minimum and maximum limits.

HDFC Bank charges 0.50% with limits of ₹3,000 to ₹11,000, while ICICI Bank imposes similar charges with a ₹2,500 to ₹10,000 range. For large loan amounts, these fees can represent substantial upfront costs that should be factored into total borrowing expenses.

Credit life insurance, loan protection, and other ancillary products often add to the effective borrowing cost. Borrowers should carefully evaluate the necessity and value of these offerings, as they can increase the total cost of borrowing by 0.25-0.50% annually.

Future Rate Outlook: Reading the RBI’s Signals

The Case for Further Cuts

Despite the October pause, the RBI has left the door open for future accommodation. The minutes of the Monetary Policy Committee meeting revealed that members see “room for rate cuts” as the inflation outlook continues to soften. With headline CPI now tracking at 1.54%—well below the 2-6% target range—the central bank has unprecedented policy space.

State Bank of India’s chief economist has argued for more aggressive action, projecting average CPI inflation for FY26 at just 2.2%, even lower than the RBI’s 2.6% forecast. This analysis suggests the central bank “runs the risk of missing the bull’s eye if it remains fixated on market cacophony” rather than acting decisively on the clear disinflationary trend.

The potential for 25-50 basis points of additional cuts in Q4 FY26 or Q1 FY27 remains substantial, particularly if global economic conditions remain supportive and domestic inflation continues its benign trajectory. Such cuts would translate to further EMI reductions for floating-rate borrowers and improved affordability for new loan seekers.

Global and Domestic Factors

The timing and magnitude of future cuts will depend on several key variables. Global economic conditions, particularly U.S. monetary policy and trade tensions, could influence the RBI’s calculus. Recent tariff announcements and trade disruptions create uncertainty that may counsel caution in policy implementation.

Domestically, the sustainability of low food inflation and the impact of ongoing GST reforms will be critical determinants. The RBI has noted that while current inflation trends are favorable, geopolitical tensions and potential supply disruptions could alter the trajectory, suggesting a data-dependent approach to future policy decisions.

Monsoon patterns and agricultural output will remain key variables, given food’s dominant role in the inflation basket. A normal monsoon and stable agricultural production would support the case for continued accommodation, while adverse weather could limit policy space.

Strategic Implications for Borrowers

Timing Considerations for New Loans

Current market conditions present a favorable environment for prospective borrowers, particularly during the ongoing festival season when many banks offer promotional rates and waived processing fees. The combination of stable rates and competitive market dynamics creates opportunities for securing advantageous loan terms.

For home purchases, the current rate environment offers excellent value, though borrowers with flexibility might benefit from waiting if they can defer purchases to capture potential future cuts. The risk-reward calculation depends on individual circumstances, housing market dynamics, and the urgency of the purchase decision.

Commercial borrowers should consider longer-term fixed-rate options if available, as the current environment may represent a cyclical low in interest rates. However, floating-rate products remain attractive given the potential for further accommodation and the historically favorable rate environment.

Refinancing and Loan Switching Opportunities

Existing borrowers with older loans linked to Base Rate or MCLR systems should evaluate switching to repo-linked products to capture immediate rate benefits. The switching process typically involves minimal documentation and can result in immediate EMI reductions for qualifying borrowers.

Borrowers with personal loans or vehicle loans at higher rates should explore refinancing options, particularly if their credit profiles have improved since the original loan. The improved rate environment and increased competition among lenders have created opportunities for rate optimization.

Home loan borrowers might consider partial prepayments using bonuses or surplus funds, as the current stable rate environment reduces the opportunity cost of deploying cash for debt reduction. However, borrowers should balance prepayment benefits against investment opportunities and maintain adequate liquidity buffers.

Credit Score Optimization Strategies

The current environment rewards borrowers with strong credit profiles, with rate differentials of 0.50-1.00% or more between prime and standard borrowers. Investing in credit score improvement can yield substantial long-term savings, particularly for large loan amounts.

Borrowers should focus on timely payments across all credit obligations, optimal credit utilization rates, and maintaining diverse credit profiles. The benefits compound over time, particularly in a competitive lending environment where institutions actively price for risk.

Credit monitoring and periodic rate negotiations with existing lenders can also yield benefits. Many institutions offer loyalty programs and relationship-based pricing that can reduce borrowing costs for long-standing customers with strong repayment histories.

Economic Context and Broader Implications

Growth-Inflation Balance

The RBI’s policy stance reflects a favorable growth-inflation trade-off, with GDP growth projections raised to 6.8% while inflation forecasts decline to 2.6%. This combination provides unusual policy flexibility and suggests continued support for economic expansion through accommodative monetary policy.

The services sector resilience, combined with improving investment activity and government capital expenditure, supports the growth outlook. Manufacturing activity has shown consistent expansion, while exports remain competitive despite global trade tensions.

Current account dynamics have improved substantially, with the deficit narrowing to just 0.2% of GDP in Q1 FY26 from 0.9% in the previous year. Strong services exports and robust remittance inflows provide external sector stability that supports domestic monetary accommodation.

Financial Sector Health

The banking sector’s strong capitalization and improved asset quality provide the foundation for continued credit expansion at favorable rates. Non-performing asset ratios have declined to multi-year lows, while bank profitability remains robust, supporting competitive pricing in loan markets.

Credit growth has remained healthy across segments, with home loans leading expansion while commercial credit shows steady improvement. The financial sector’s resilience provides confidence in the sustainability of current rate benefits and the capacity to absorb future policy changes.

Capital adequacy ratios across the banking system remain well above regulatory requirements, providing institutions with the flexibility to expand lending while maintaining competitive pricing. This structural strength supports the continuation of borrower-favorable conditions.

Conclusion: Navigating the New Normal

The RBI’s decision to hold rates at 5.5% represents a strategic pause in an extraordinary year of monetary accommodation that has delivered substantial benefits to Indian borrowers. The 100 basis point reduction from 6.5% to 5.5% has created the most favorable borrowing environment in years, with home loan EMIs reflecting the direct benefits of policy transmission.

For current borrowers, the stability means predictable EMI outflows and continued benefits from earlier rate cuts. The opportunity ahead lies in the potential for further accommodation, with the RBI maintaining flexibility to support growth as inflation remains benign. The central bank’s upgraded growth projections and dramatically lower inflation forecasts suggest a favorable policy trajectory.

The strategic message for borrowers is clear: current conditions offer excellent value for both new loans and refinancing existing obligations. While future cuts remain possible, the present environment already provides substantial benefits compared to the higher rate regime of 2024. The combination of competitive pricing, improved credit availability, and stable economic conditions creates an optimal environment for strategic financial planning.

Looking forward, borrowers should focus on optimizing their credit profiles, evaluating refinancing opportunities, and positioning themselves to benefit from potential future accommodation. The RBI’s commitment to supporting growth while maintaining price stability suggests continued borrower-friendly policies, making this an opportune time for strategic financial decisions.

The path ahead requires balancing immediate opportunities with future possibilities, recognizing that India’s monetary policy framework provides both stability and flexibility. For millions of Indian borrowers, the current environment represents the culmination of favorable policy decisions and improved economic fundamentals that support homeownership dreams and business expansion plans.

Ready to take advantage of the current favorable interest rate environment? Contact our M&A advisory team to explore strategic financing opportunities and optimize your borrowing costs in this evolving monetary landscape.

Leave a Reply