The U.S. stock market has entered what can only be described as the final, most perilous phase of a historic asset bubble, with multiple valuation metrics simultaneously flashing red warnings not seen since the dot-com mania of 2000. The S&P 500’s Shiller CAPE ratio has soared to 39.5, approaching the second-highest level in 144 years of market history, while Warren Buffett’s preferred market indicator has exploded to 217%—a level the Oracle of Omaha once warned represents “playing with fire”. Combined with unprecedented market concentration where just 10 companies now control 40% of the entire S&P 500, these metrics paint a picture of a market that has become dangerously divorced from economic reality.

What makes the current situation particularly alarming is not just the absolute level of overvaluation, but the convergence of multiple independent warning signals occurring simultaneously. Historical precedent suggests that when the Shiller CAPE exceeds 35, every subsequent one-year period has delivered negative returns, according to economist David Rosenberg. The last three times valuation reached these extremes—in 1929, 2000, and 2021—were followed by devastating crashes of 83%, 49%, and 25% respectively. With artificial intelligence euphoria driving a parabolic melt-up phase reminiscent of the railway mania of the 1840s and the internet bubble of 1999, investors face a critical decision: whether to chase the final stages of what appears to be the most dangerous market bubble in modern history.

The Shiller CAPE Ratio: Approaching Historic Danger Zone

Current Levels Match Only the Greatest Bubbles in History

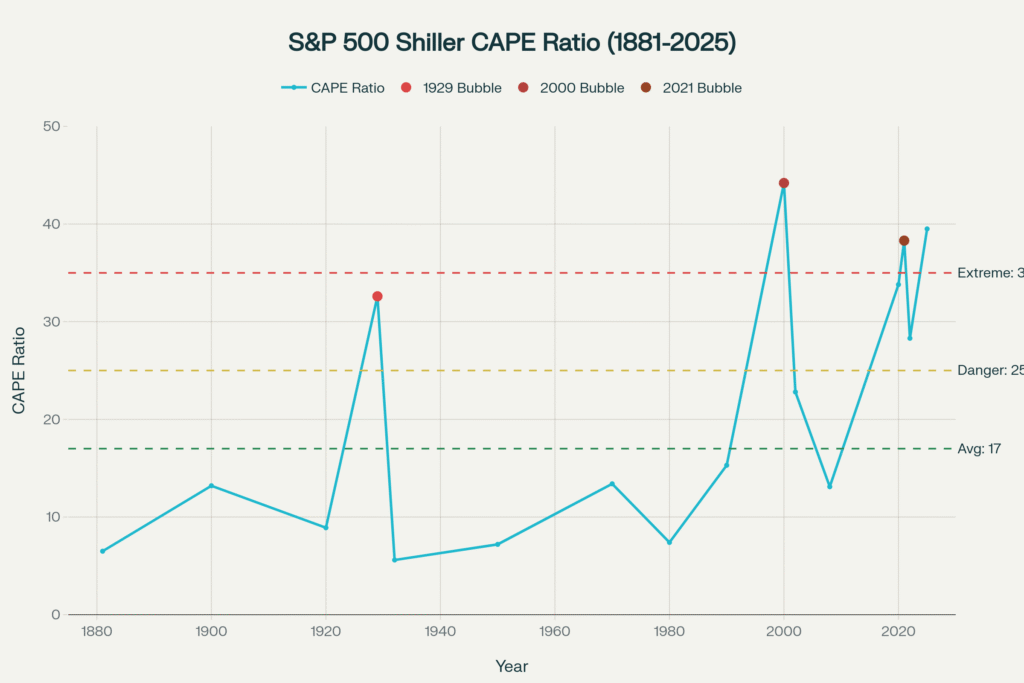

The Shiller Cyclically Adjusted Price-Earnings (CAPE) ratio, developed by Nobel laureate Robert Shiller, currently stands at 39.5 as of October 2025, representing the third-highest reading in 144 years of U.S. stock market history. This valuation metric, which compares current prices to inflation-adjusted earnings averaged over the previous decade, has exceeded 32 only three times since 1881: during the pre-1929 crash peak of 32.6, the 2000 dot-com bubble peak of 44.2, and the current period.

The significance of these levels cannot be overstated. When Shiller himself expressed alarm in 2014 at a CAPE ratio of 25, he noted that this threshold had been surpassed during only three previous periods, each followed by devastating market crashes. The current reading of 39.5 places the market in territory that historically precedes negative returns over virtually all subsequent time horizons. Analysis by economist David Rosenberg demonstrates that when the CAPE ratio exceeds 35, every single one-year forward period in history has produced negative returns.

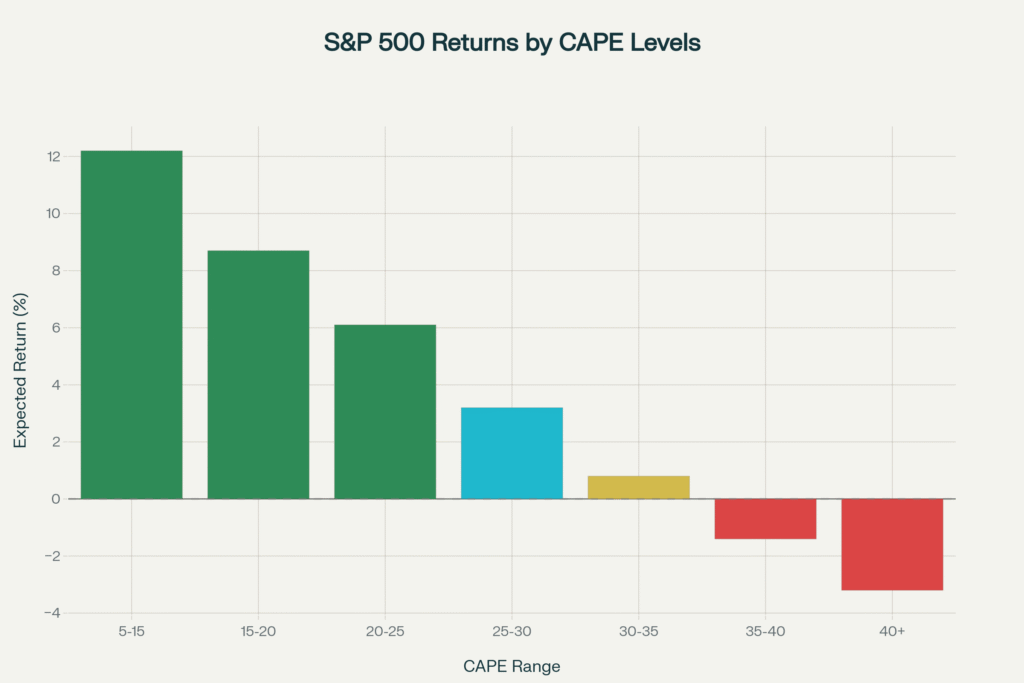

The mathematical implications are sobering for long-term investors. Historical data analysis reveals that at current CAPE levels between 35-40, investors should expect annualized returns of approximately -1.4% over the next decade, assuming normal mean reversion patterns. This stands in stark contrast to the long-term average stock market return of approximately 10% annually, suggesting that an entire generation of investors may face a “lost decade” similar to Japan’s experience in the 1990s or the U.S. market’s performance from 2000-2010.

AI Narrative Driving Unprecedented Speculation

The current bubble differs from previous episodes in its concentration around artificial intelligence themes, creating what market analysts describe as a “story stock” phenomenon reminiscent of the internet revolution narrative that drove the dot-com boom. Unlike the 1990s, when hundreds of companies with questionable business models attracted speculative investment, today’s AI bubble is concentrated among a handful of mega-cap technology companies with genuine earnings and cash flows. However, this fundamental strength may actually make the current bubble more dangerous, as it provides intellectual justification for increasingly extreme valuations.

The AI narrative has created what behavioral economists term “this time is different” syndrome, where investors rationalize unprecedented valuations based on transformative technology promises. Companies like NVIDIA, with a forward P/E ratio representing the highest for any leading S&P 500 component since at least 1981, trade at multiples that embed expectations of sustained hypergrowth that may prove mathematically impossible to achieve. NVIDIA alone now represents 8.1% of the entire S&P 500, larger than entire sectors and creating systemic risk if the AI investment thesis fails to materialize.

The concentration of speculative enthusiasm around AI mirrors historical patterns observed during previous technological revolutions. The railway mania of the 1840s, the radio bubble of the 1920s, and the internet craze of the 1990s all featured revolutionary technologies that ultimately transformed society—but not before destroying enormous amounts of investor capital during speculative excess phases. While AI will undoubtedly prove transformative over decades, current market pricing appears to discount decades of perfect execution and exponential growth that historical precedent suggests is unlikely to materialize.

Warren Buffett Indicator: Playing with Fire at 217%

Unprecedented Divergence from Economic Reality

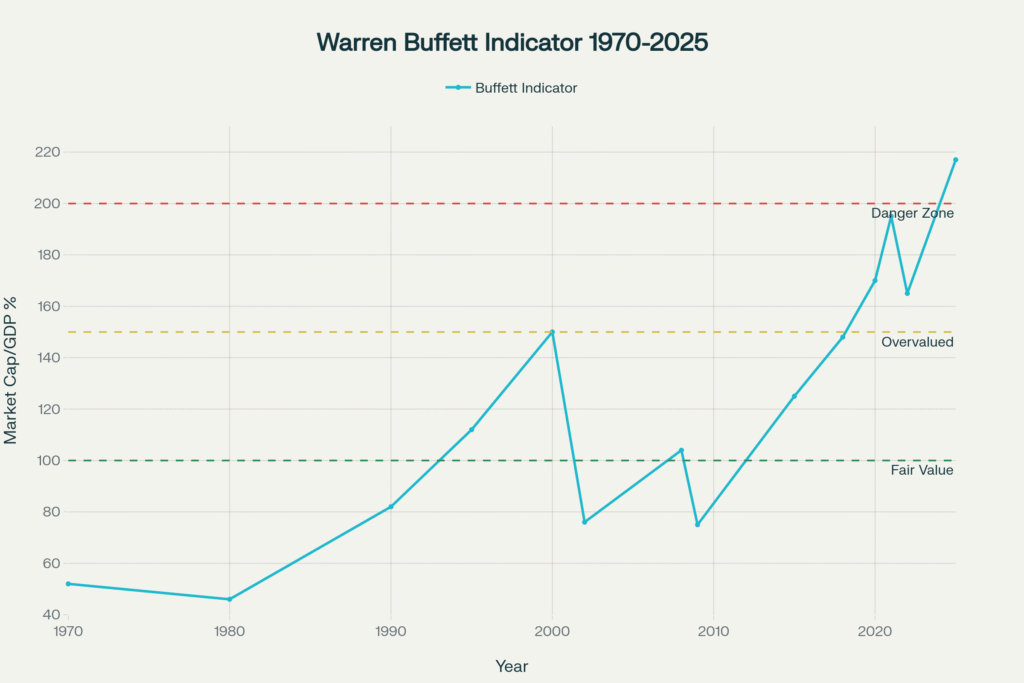

Warren Buffett’s preferred market valuation indicator—the ratio of total stock market capitalization to Gross Domestic Product—has reached an all-time high of 217%, far exceeding the previous peak of 195% in 2021. This metric, which Buffett described as “probably the best single measure of where valuations stand at any given moment,” provides a stark illustration of how dramatically stock prices have outpaced underlying economic growth. The current reading represents more than double what Buffett considers fair value (around 100%) and significantly exceeds his “playing with fire” threshold of 200%.

The historic context of this reading is particularly alarming. During the dot-com bubble peak in 2000, the indicator reached 150% before the NASDAQ crashed 80% over the subsequent two years. The 2008 financial crisis began with the indicator at 104%, while the Great Depression started with readings well below current levels. The fact that today’s reading of 217% exceeds all previous bubble peaks suggests that the magnitude of potential correction could surpass historical precedents.

This divergence reflects fundamental structural changes in the economy that may not justify current market premiums. While proponents argue that modern technology companies generate higher returns on invested capital and operate with less physical infrastructure than traditional industrial companies, the aggregate economy still depends on physical goods, services, and human labor that constrain growth regardless of technological advancement. The idea that financial assets can permanently trade at more than double the size of the productive economy represents a form of collective delusion that inevitably requires correction.

Global Context and International Comparisons

The U.S. market’s extreme overvaluation becomes even more apparent when compared to international markets, where similar technology trends exist but valuations remain far more reasonable. European markets trade at CAPE ratios in the low-to-mid 20s, while emerging markets remain below 15, suggesting that U.S.-specific factors rather than global technological transformation drive current extremes. This disparity indicates that American investors may be paying a significant “AI premium” that may not be justified by superior growth prospects.

The concentration of global investment flows into U.S. technology stocks has created what economists term a “reflexive bubble,” where rising prices attract additional capital, which drives prices higher, creating a self-reinforcing cycle that becomes increasingly unstable. Foreign investment in U.S. equities has reached record levels, with international investors chasing AI-related returns despite already-extreme valuations. This dynamic creates vulnerability to sudden capital flight if sentiment shifts or if alternative investment destinations become more attractive.

Currency implications add another layer of risk for international investors in U.S. markets. The dollar’s strength, partly driven by foreign capital inflows seeking AI exposure, makes U.S. assets more expensive for international buyers while potentially creating conditions for eventual dollar weakness if investment flows reverse. A reversal in international capital flows could create a double-negative impact for foreign investors through both equity price declines and currency losses, potentially accelerating any correction in U.S. markets.

Market Concentration: Systemic Risk from Mega-Cap Dominance

Unprecedented Concentration Creates Systemic Vulnerability

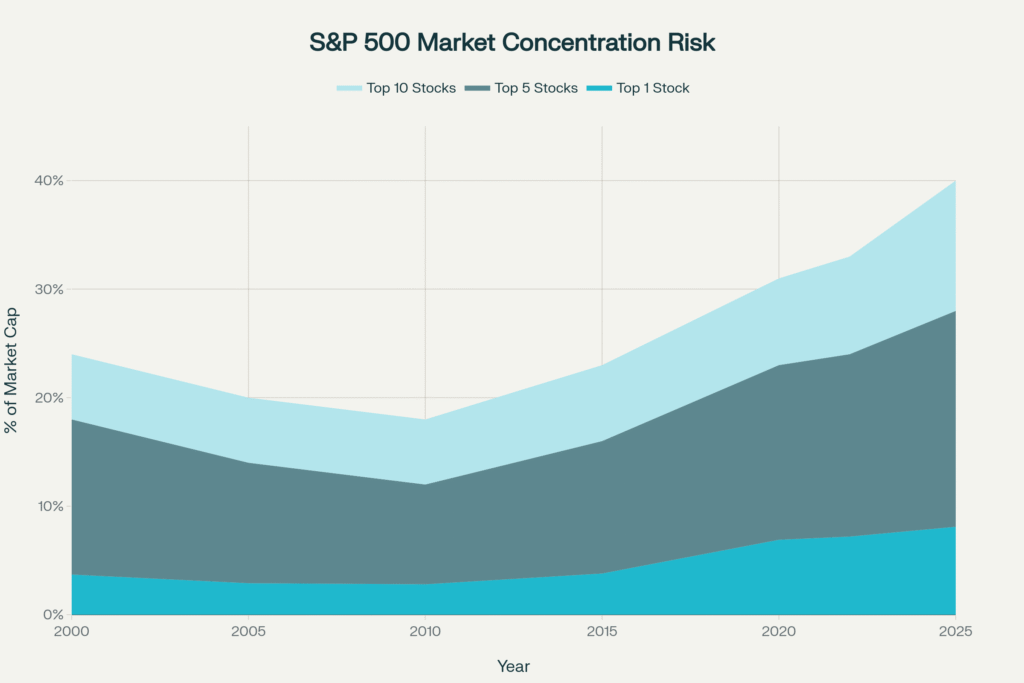

The current market structure exhibits the highest concentration of market capitalization in a handful of companies since reliable records began, with the top 10 stocks representing approximately 40% of the entire S&P 500 market value. This concentration exceeds even the dot-com bubble peak, when the largest companies commanded smaller percentages of total market cap despite similarly extreme individual valuations. NVIDIA’s 8.1% weighting alone exceeds the entire healthcare sector, while the top six companies control one-third of the index.

This concentration creates unprecedented systemic risk, as the performance of the broader market becomes increasingly dependent on a small number of companies whose individual fortunes may diverge significantly from economic fundamentals. Traditional diversification benefits deteriorate when such a large portion of index returns depends on a handful of companies, particularly when those companies operate in related industries and face similar regulatory, competitive, and technological risks. A significant decline in any of the top-weighted stocks can trigger cascading effects throughout the broader index.

The mathematical implications of this concentration are particularly concerning during potential correction scenarios. If the top 10 holdings were to decline by 50%—not uncommon during major bear markets—the S&P 500 would fall by approximately 20% from concentration effects alone, before considering broader market psychology and forced selling dynamics. Historical precedent suggests that during major corrections, leading stocks often decline more than the broader market, potentially amplifying the concentration risk significantly.

Technology Sector Dominance and Regulatory Risks

The concentration risk is compounded by sector concentration, with technology companies representing an unprecedented portion of total market capitalization. Information technology and communication services sectors combined represent over 40% of the S&P 500, creating vulnerability to sector-specific risks including regulatory intervention, technological disruption, and cyclical downturns. This level of sector concentration has no historical precedent in U.S. markets, making it difficult to predict how such a structure might behave during stress periods.

Regulatory risks specific to mega-cap technology companies add another dimension of concentration risk. Antitrust investigations, data privacy regulations, and potential AI-specific oversight could disproportionately impact the largest market components. The Biden administration’s aggressive antitrust stance and growing bipartisan concern about technology company power create ongoing regulatory risks that could trigger significant valuation adjustments in the most heavily weighted index components.

International regulatory developments create additional concentration risks, as major technology companies generate significant revenues from global markets subject to different regulatory frameworks. European Union regulations on AI development, Chinese restrictions on technology transfers, and evolving privacy regulations worldwide create multiple potential triggers for revaluation of the largest index components. The concentration of market cap in companies with significant international exposure amplifies the impact of adverse regulatory developments in any major market.

Historical Precedent: When Valuations Reached These Levels

The 1929 Precedent: The Original Bubble Burst

The 1929 stock market crash provides the most relevant historical precedent for current market conditions, as it remains the only other period when multiple valuation metrics simultaneously reached extreme levels comparable to today. The Shiller CAPE ratio peaked at 32.6 in September 1929, followed by the infamous crash in October that began a decline ultimately reaching 83% from peak to trough. The similarities to today’s market extend beyond simple valuation metrics to include concentration in leading companies, speculative fever around transformative technologies, and widespread belief that “this time is different”.

The 1920s bubble, like today’s, was driven by legitimate technological innovation—radio, automobiles, and mass production techniques that genuinely transformed society. Companies like RCA commanded valuations based on their revolutionary potential, much as AI companies do today. However, even genuinely transformative companies saw their stock prices decline by 90% or more during the subsequent correction, demonstrating that technological merit does not protect against valuation extremes during speculative corrections.

The aftermath of the 1929 crash illustrates the potential magnitude of wealth destruction possible when valuations reach current extremes. An investor who bought the S&P 500 at its 1929 peak would have experienced negative returns for over 25 years, not recovering their initial investment until September 1954. This “lost generation” scenario represents the most severe outcome possible for today’s investors, though it demonstrates that even extreme overvaluation does not guarantee immediate correction—markets can remain expensive longer than many expect.

The 2000 Dot-Com Crash: Technology Bubble Precedent

The dot-com bubble of 1999-2000 provides an even more relevant comparison to current conditions, as it similarly centered on transformative technology with legitimate long-term potential. The Shiller CAPE peaked at 44.2 in December 1999, followed by a 49% decline in the S&P 500 from March 2000 to October 2002. The NASDAQ, more concentrated in technology companies, declined 78% from peak to trough, illustrating how sector concentration amplifies losses during corrections.

The parallels between the internet revolution of the 1990s and today’s AI revolution are striking: both involved genuinely transformative technologies, both attracted massive speculative investment, and both created “new era” narratives that justified unprecedented valuations. Companies like Cisco Systems, trading at over 100 times earnings in 2000, were profitable enterprises with real market-leading positions—yet still declined over 80% during the subsequent correction. This precedent suggests that even the highest-quality AI companies may not escape significant valuation compression if broader market sentiment shifts.

The dot-com crash also demonstrated how quickly market psychology can reverse during valuation extremes. The transition from euphoria to panic occurred over a matter of months, not years, as investors realized that even revolutionary technologies could not justify infinite valuation multiples. Today’s AI market exhibits similar psychological extremes, with widespread belief that current leaders possess unassailable competitive advantages that may prove less durable than currently assumed.

The 2021-2022 Correction: Recent Warning Signal

The most recent precedent occurred in 2021-2022, when similar valuation extremes led to a significant but incomplete market correction. The Shiller CAPE peaked at 38.3 in late 2021, followed by a 25% decline in the S&P 500 during 2022. However, this correction proved insufficient to restore normal valuation levels, with the market recovery driving metrics to even higher extremes than the previous peak. This pattern suggests that incomplete corrections during extreme valuation periods often lead to even more dangerous subsequent bubbles.

The 2021-2022 episode demonstrates how modern monetary policy and market structure may prolong bubble conditions beyond historical norms. Federal Reserve intervention, corporate share buybacks, and passive investment flows may have prevented the type of complete valuation reset that characterized previous bubble endings. However, this intervention may have simply delayed and amplified the ultimate correction, as current valuation levels exceed even the 2021 peak across multiple metrics.

The incomplete nature of the 2021-2022 correction has created what economists term a “double bubble” scenario, where the second phase often proves more destructive than the initial peak. Historical precedent suggests that when markets fail to complete normal correction cycles, the eventual adjustment often exceeds what would have occurred during the initial downturn. Current valuation levels suggest that the market may be in the final phase of this double bubble pattern, with potential corrections exceeding the relatively modest 25% decline of 2022.

The Melt-Up Phase: Final Stage Before Reversal

Characteristics of Parabolic Market Acceleration

The current market exhibits classic characteristics of what technical analysts term a “melt-up phase”—the final, most dangerous stage of a bubble cycle characterized by parabolic price acceleration driven by fear of missing out rather than fundamental analysis. CLSA’s technical strategist Laurence Balanco describes the current environment as a “melt-up phase” with “further juice left in the trade,” reflecting the psychological dynamics that typically mark bubble peaks. This phase can extend longer and reach higher extremes than rational analysis suggests possible, making it particularly treacherous for both bulls and bears.

Melt-up phases typically feature several distinctive characteristics, all of which are evident in current markets: compressed timeframes where gains that previously took years occur in months, failure of traditional resistance levels, broad participation across previously lagging sectors, and market resilience to negative news that would have triggered corrections in normal environments. The S&P 500’s ability to shrug off major geopolitical shocks, trade tensions, and economic uncertainties demonstrates the type of market psychology that characterizes final bubble phases.

The psychological dynamics of melt-up phases create particularly dangerous conditions for investors. Fear of missing out (FOMO) drives continued buying despite recognizing overvaluation, while early bears are repeatedly forced to cover positions, adding fuel to the advance. Professional investors often capitulate during this phase, abandoning disciplined valuation approaches in favor of momentum-based strategies. This capitulation by sophisticated investors often marks the final stage before reversal, as the last sources of rational selling pressure are eliminated.

Technical Indicators Signal Extreme Conditions

Multiple technical indicators are flashing warning signals consistent with late-stage bubble conditions. Put/call ratios have fallen to extreme lows, indicating complacency among options traders, while the VIX volatility index remains suppressed despite mounting fundamental risks. These contrarian indicators suggest that investors have become dangerously complacent, pricing in continued stability that historical precedent suggests is unlikely to persist.

Market breadth indicators reveal underlying weakness despite strong index performance, with advancing stocks failing to confirm new highs in major indices. This divergence suggests that market strength is increasingly dependent on a small number of large-capitalization stocks, making the broader market vulnerable to reversals in these key components. When market breadth deteriorates during late-stage bubbles, it often signals that institutional distribution is occurring beneath surface strength.

Sentiment surveys reveal extremes in bullish sentiment that historically precede major market reversals. The American Association of Individual Investors (AAII) sentiment survey shows bullish readings at levels typically associated with market peaks, while professional investor surveys indicate similar extremes in optimism. Contrarian analysis suggests that when both retail and professional investors reach consensus on continued market gains, the probability of reversal increases significantly.

Economic Fundamentals vs. Market Valuations

Growing Disconnect from Underlying Economy

The divergence between stock market performance and underlying economic fundamentals has reached levels not seen since the dot-com bubble, with corporate earnings growth failing to keep pace with stock price appreciation across most sectors. While S&P 500 companies have delivered solid earnings growth in recent quarters, the magnitude of stock price increases far exceeds earnings improvements, resulting in expanding valuation multiples across virtually all market sectors. This pattern typically characterizes the final stages of bull markets, when investor enthusiasm drives prices beyond levels justified by business fundamentals.

Key economic indicators suggest underlying weakness that contrasts sharply with market optimism. The labor market has shown signs of deterioration, with job growth averaging below 100,000 per month over recent periods and significant downward revisions to previously reported employment gains. Initial jobless claims have risen above 260,000, a level that historically correlates with negative payroll growth, yet markets have largely ignored these warning signals. This disconnect between labor market reality and market performance mirrors patterns observed during previous bubble periods.

Corporate profit margins remain near historic highs, but face pressure from rising labor costs, potential tariff impacts, and normalizing competitive conditions as the economy adjusts to post-pandemic dynamics. Analysts’ earnings expectations for 2026 and beyond embed optimistic assumptions about margin sustainability and revenue growth that may prove difficult to achieve in a more normalized economic environment. The gap between current market pricing and realistic earnings projections suggests significant vulnerability to disappointment.

Federal Reserve Policy and Market Dependency

The relationship between Federal Reserve policy and market valuations has created a dangerous dependency that amplifies bubble risks. While the Fed has begun cutting interest rates from peak levels, the current policy stance remains restrictive compared to the emergency accommodation that supported previous market recoveries. Market participants appear to have embedded expectations for continued policy support that may not materialize if economic conditions deteriorate or inflation concerns resurface.

The effectiveness of monetary policy transmission has diminished as interest rates approach lower bounds, potentially limiting the Federal Reserve’s ability to support markets during future stress periods. Previous bubble corrections were ultimately resolved through aggressive monetary easing, but the current policy environment may not permit the same degree of intervention without risking renewed inflation or financial instability. This constraint suggests that market corrections beginning from current valuation levels may prove more severe and persistent than recent historical experience.

Quantitative tightening continues to reduce Federal Reserve balance sheet assets, gradually withdrawing liquidity from financial markets despite rate cuts. This technical backdrop creates headwinds for risk asset valuations that contrast with the supportive conditions that prevailed during previous market advances. The combination of reduced central bank liquidity and extreme valuations creates conditions where normal market stress could trigger larger corrections than would occur under more supportive policy conditions.

Investment Implications and Risk Management

Portfolio Positioning in Dangerous Territory

Institutional investors face unprecedented challenges in positioning portfolios when multiple valuation metrics signal extreme overvaluation but market momentum remains strong. Traditional value-oriented strategies have underperformed dramatically during the AI-driven melt-up, forcing many portfolio managers to choose between maintaining disciplined approaches or chasing momentum despite recognizing bubble conditions. This forced choice between career risk and fiduciary duty typically characterizes late-stage bubble environments.

Risk management becomes particularly challenging when fundamental analysis suggests caution but market behavior rewards continued risk-taking. Academic research demonstrates that bubble conditions can persist longer than most participants expect, making timing-based strategies extremely difficult to implement successfully. However, the same research shows that the eventual corrections from extreme valuation levels typically exceed the gains from attempting to ride bubble peaks. Strategic asset allocation approaches that maintain some defensive positioning may prove superior to tactical timing attempts.

Diversification benefits deteriorate significantly during late-stage bubble conditions, as correlations between asset classes and individual securities increase dramatically during correction phases. Traditional portfolio construction approaches based on historical correlation relationships may provide less downside protection than models suggest when markets correct from extreme valuation levels. International diversification and alternative asset classes may offer some protection, though global financial market integration limits the effectiveness of geographic diversification during systemic corrections.

Sector and Style Considerations

Growth vs. value dynamics have reached extremes not seen since the dot-com bubble, with growth stocks trading at significant premiums to value stocks across most market capitalization ranges. Historical precedent suggests that these style differentials often reverse dramatically during major market corrections, as growth stocks typically experience larger declines due to higher starting valuations and momentum-driven ownership. Value-oriented strategies may offer relative protection during correction phases, though absolute returns will likely be negative across all equity styles if corrections match historical precedents from similar valuation levels.

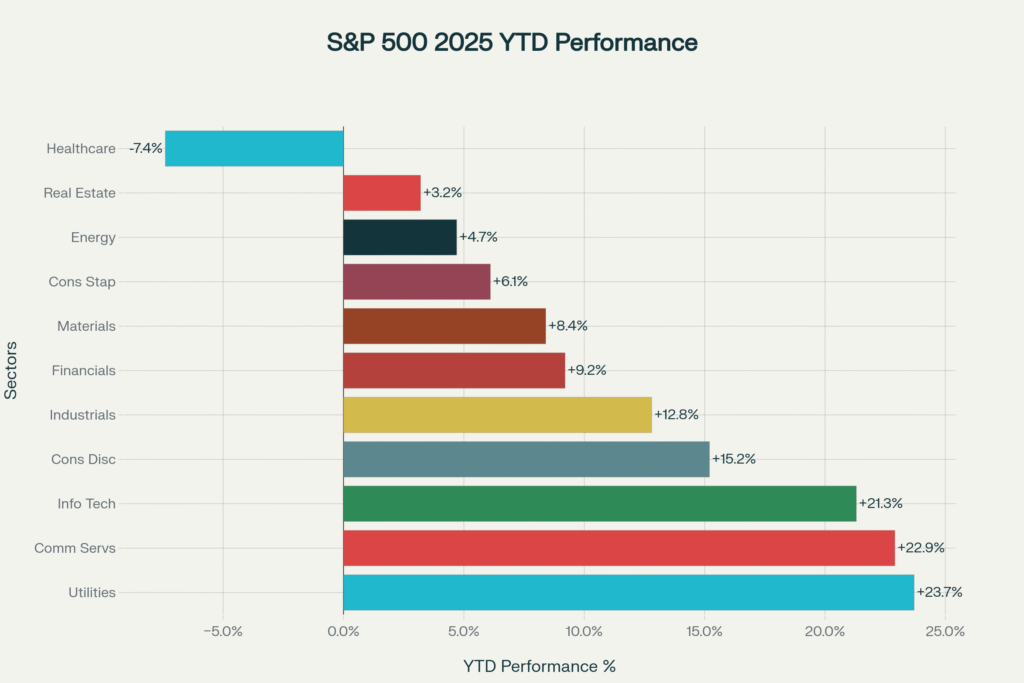

Sector rotation patterns suggest increasing vulnerability in technology and growth-oriented sectors that have driven market performance. Utilities, consumer staples, and other defensive sectors have begun outperforming despite their historically lower growth profiles, potentially signaling institutional recognition of increased market risks. However, defensive sectors also trade at elevated valuations by historical standards, limiting their effectiveness as safe havens during broad market corrections.

Small and mid-cap stocks present a particularly complex risk-return trade-off in the current environment. While these sectors have underperformed large-cap growth stocks during the AI bubble, they also trade at historically extreme valuations with median price-to-earnings ratios exceeding levels seen even during previous bubble periods. Small-cap valuations in the 40-45x range suggest that these sectors may be as vulnerable as large-caps during broad market corrections, despite their relative underperformance during the bubble phase.

Alternative Investment Considerations

Traditional safe-haven assets face challenges in the current environment due to interest rate dynamics and inflation concerns. Government bonds provide some diversification benefits but offer limited real returns after inflation and remain vulnerable to interest rate changes that could accompany economic policy shifts. Corporate bonds face credit risk as earnings disappoint and refinancing challenges emerge if economic conditions deteriorate from current levels.

Commodity investments may offer some portfolio protection during correction phases, particularly if correction is accompanied by currency devaluation or inflation concerns. Gold and other precious metals have historically provided portfolio insurance during extreme market stress, though their effectiveness depends on the specific triggers and policy responses to market corrections. Real estate investment trusts (REITs) face challenges from both valuation concerns and interest rate sensitivity, limiting their effectiveness as portfolio diversifiers.

International markets trading at lower valuations may provide some diversification benefits, though global market integration limits downside protection during systemic corrections. Emerging market equities trade at more reasonable valuations but face their own risks from potential global economic slowdown and capital flight to perceived safe havens. The key challenge is that virtually all risk assets have become expensive by historical standards, making true diversification extremely difficult to achieve.

Conclusion: Navigating the Most Dangerous Market in History

The convergence of multiple independent valuation metrics at historic extremes creates what can only be described as the most dangerous market environment in modern history. With the Shiller CAPE at 39.5, the Buffett Indicator at 217%, and market concentration reaching unprecedented levels, investors face conditions that have historically preceded devastating market corrections of 25-83%. The current environment differs from previous bubbles not in its fundamental dynamics—speculative excess driven by transformative technology narratives—but in its magnitude and the degree to which traditional risk management approaches have been overwhelmed by momentum and forced participation.

The melt-up phase currently underway represents the most treacherous period for investors, as rational valuation analysis is overwhelmed by fear of missing out and institutional capitulation to momentum strategies. Historical precedent suggests that this phase can continue longer than most expect, but the ultimate resolution invariably involves corrections that exceed the gains from attempting to ride bubble peaks. For most investors, the prudent approach involves reducing risk exposure, maintaining defensive positions, and preparing for the wealth destruction that typically accompanies the end of bubble periods.

The artificial intelligence revolution will undoubtedly prove transformative over decades, much as the internet and mobile computing ultimately justified early optimism despite intervening crashes. However, current market pricing appears to discount decades of perfect execution and exponential growth that mathematics and competition make unlikely to achieve. Investors who maintain discipline during this final bubble phase may find themselves positioned to capitalize on the unprecedented opportunities that typically emerge after extreme overvaluation corrects to undervaluation.

The path forward requires acknowledgment that normal market rules may not apply during parabolic phases, but historical precedent remains the best guide for ultimate outcomes. While timing the exact peak remains impossible, the accumulation of risk factors suggests that prudent investors should prioritize capital preservation over potential gains from riding the final stages of what appears to be the most dangerous market bubble in modern history. The mathematics of mean reversion suggest that the current extreme will ultimately correct, and the severity of that correction may define investment returns for the next decade.

Ready to navigate the most dangerous market environment in history? Our specialized investment advisory services help institutional investors and high-net-worth individuals develop robust risk management strategies for extreme market conditions. From defensive positioning to opportunistic value identification, we provide comprehensive portfolio guidance for protecting and growing wealth during bubble periods and their aftermath. Contact us today to explore how sophisticated risk management approaches can help preserve capital during what may prove to be the most severe market correction in modern history.

Leave a Reply